How annuities work in Canada

Presented By

National Bank of Canada

While almost seven in ten current Canadian retirees say that in retrospect they should have saved for retirement for at least 25 years, a poll finds 15% of those still working will spend less than five years saving for retirement and 6% don’t plan to save at all.

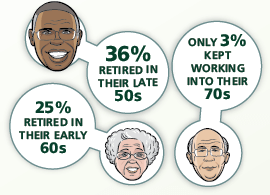

Talk about a disconnect! Not surprisingly given these dismal efforts, the TD Retirement Realities Poll finds many still working plan to do so longer than current retirees did during their careers. The poll, released today, finds 64% of working Canadians expect to retire in their 60s. However, more of them (36%) expect to do so after the traditional retirement age of 65, versus just 28% who are shooting for their early 60s. And a surprising number — 16% — expect to keep slogging it out well into their 70s. Only 3% of current retirees kept it up into their 70s, with 36% leaving full-time work by their late 50s and 25% by their early 60s.

The poll of 2,407 conducted by Environics Research focused on Canadians 25 years old or more, split between 1,251 workers and 929 retirees. More than 60% of the former said they won’t save for retirement for as long as the latter group recommends. When today’s retirees were asked how long they thought they should have saved for retirement, a whopping 69% said at least 25 years.

25 years should be the absolute minimum saving timeframe

Studies I’ve seen in the past typically use 25 years as an absolute minimum, and given the trend to greater longevity, it’s arguable that 30, 35 or even 40 years is more realistic. One thing for sure, a mere five years isn’t going to do it. If you’re in that camp, you’re making a big bet on living solely on government benefits in old age. In that case, check out Julie Cazzin’s Retire in Luxury on Next to Nothing feature in the November issue of MoneySense for a list of places in the world where you can live solely on CPP and some combination of OAS and GIS.

But if you do plan to save only for a short time, you may as well focus on the TFSA. See my earlier blog for more on that.

Click here for the full infographic on TD’s full findings.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Learn how the federal government’s 2024 budget can affect you and your money.

Gen Z isn’t immune to phishing scams. Find out the most common schemes targeting young Canadians and how to...

Doing home renovations? Find out if there are any tax incentives that Canadians are able to claim.

U.S. inflation comes in hot, Delta says revenge travel is alive and well, doubling your CPP benefits, and AI...

You can amend previous tax returns to include new information, such as investment management fees for a non-registered account....

History repeats (or rhymes) itself in latest market upswing, FHSA celebrates its first birthday, investors getting rich from stocks,...

Money in a LIRA or LIF is intended to last a lifetime, making it difficult to access more than...

Financial planner and money coach Michelle Robertson left corporate life to teach women about money. Here’s what she learned...