Plan for the unexpected

Stress-test your financial plan for any major curve-balls life may throw your way.

Stress-test your financial plan for any major curve-balls life may throw your way.

On both sides of the border today are items on the perils of unexpected events setting back long-term financial plans. CNN Money is reporting here that retirement savers are losing US$117,000 to unexpected events. Meanwhile, the BMO Wealth Institute has released a 10-page report entitled The biggest life events that can derail your financial plan.

None of this should come as a surprise to investors or anyone making long-term financial plans. As the late John Lennon sang on his final album, Double Fantasy, “Life is what happens to you while you’re busy making other plans.” (By the way, he may not have been the first to say this. See here for details.)

CNN reported on an Ameriprise Financial survey of Americans aged 50 to 70 with at least US$100,000. Nine in 10 of them had already experienced at least one economic or life event that hurt their retirement savings, while almost 40% had been hit by at least five unanticipated events that caused their average loss to hit US$144,000. The takeway, Ameriprise said, was to “expect the unexpected.”

Despite all the fancy retirement calculators available to modern investors, these tools provide at best rough guesses of what may or may not happen in the future. Who 20 years ago could have anticipated the minuscule interest rates that now afflict fixed-income investors? Stock market declines come around with unwelcome frequency and as we saw in the 2008 financial crisis, home prices are equally subject to price volatility. Putting aside money for children’s education or taking care of ailing elderly parents can also take a toll on savings.

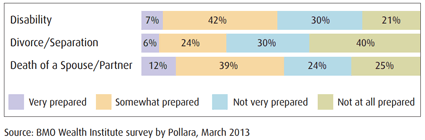

BMO makes the valid point that merely having some sort of financial plan isn’t enough: you need to stress-test such plans to make sure they can withstand major declines in financial markets, as well as major life events like job loss, illness or disability, death of a spouse and other events.

Far from Lennon’s double fantasy, such disruptions can inflict what BMO terms a “double shock” of both loss of income as well as unplanned extra demands on spending. Little wonder BMO finds Canadians’ biggest fear is the stress of not having enough money to retire.

If you’ve read this blog before, you’ll know what’s coming next. By all means, save and invest wisely, live below your means and do all you can to establish financial independence. This is not the same as retirement. If you can establish a modicum of findependence by your 30s or 40s (paying off all debts plus building a nest egg), you should do so: the sooner employment income is an income supplement rather than the sole means of financial support, the better.

If you’re healthy, have a good job or business and still expect decades more of life, the best insurance against unexpected financial setbacks is my three-word mantra of “just keep working.” Overshooting on retirement savings is a much more benign outcome than the opposite situation of under-saving followed by an unexpected job loss, business setbacks or marital splits. If you dislike your current career so much that you’re obsessed about “retiring” solely to get away from it, perhaps you should consider going back to school or retraining and find a career that’s more compatible with your nature. If you can’t see yourself doing what you’re doing now well into your 60s, that’s a clue you may be on the wrong track. (See also this Marketwatch column on the 8 habits of highly effective retirees. The point is you need to retire TO something, not FROM something!)

Sure, there are ways to increase the odds of surviving financial setbacks. BMO talks about disability insurance, long-term care insurance, maxing out Tax Free Savings Accounts (TFSAs) as a source of ready emergency funds, and various other actions. It spends some time discussing the “financial impact of widowhood,” pointing out that a couple with no life insurance would face the double shock of loss of income of a deceased spouse, even as the bills and expenses continue to mount up.

But you shouldn’t view the sudden death of a spouse as a “black-swan” event coming out of the blue. We all know we are mortal, as are our partners. In Canada, the average age of widowhood for women is a relatively young 56, according to BMO. And of course, even if both spouses live to a ripe old age, there’s the ever present spectre of divorce. BMO talks about the phenomenon of “grey divorce,” pointing out the only age group seeing a rise in divorce in this country are couples over age 50. If you were counting on two sets of RRSPs or RRIFs, two employer pensions and two sets of CPP and OAS payments, clearly cutting everything in half would amount to a major haircut to your financial plan. A good “stress test” would be to project your resources solely on your personal assets and pensions.

Seen thus, you could argue every Canadian should build their financial plans solely around their own resources, viewing any spousal contributions as a welcome bonus should illness, premature death or divorce not come to pass. I do this myself, despite the fact I’m in a solid marriage and hope to continue in it for decades to come.

If you’ve not discussed these things with a financial planner, now is as good a time as any, especially in light of the still-surging stock market.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Doing home renovations? Find out if there are any tax incentives that Canadians are able to claim.

U.S. inflation comes in hot, Delta says revenge travel is alive and well, doubling your CPP benefits, and AI...

You can amend previous tax returns to include new information, such as investment management fees for a non-registered account....

History repeats (or rhymes) itself in latest market upswing, FHSA celebrates its first birthday, investors getting rich from stocks,...

Money in a LIRA or LIF is intended to last a lifetime, making it difficult to access more than...

Financial planner and money coach Michelle Robertson left corporate life to teach women about money. Here’s what she learned...

When you die, capital gains tax might apply to some of your assets. Can life insurance help shelter your...

Do Canadians have to file a trust tax return this year? What is a bare trust? What are the...

Trump sells unprofitable company for billions, the U.S. is an oil king, GameStop struggles continue, and tech rules the...