Building a low-fee portfolio that lasts

No more high-fee Canadian equity mutual funds. It’s time for a new portfolio that delivers more income and better returns with less risk

No more high-fee Canadian equity mutual funds. It’s time for a new portfolio that delivers more income and better returns with less risk

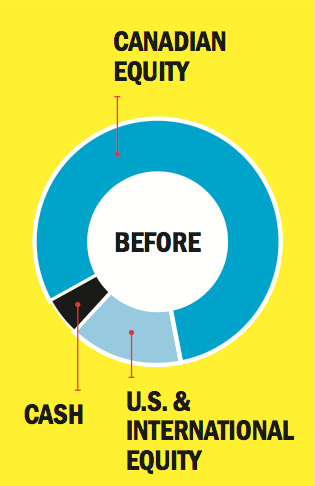

Cochrane, Alta. residents Edward, 60, and Penelope, 58, retired five years ago. Ed feels grateful to his former employer for his defined benefit pension plan, but he doesn’t feel that way about his adviser of 25 years. “We’re getting mediocre returns—we’re not even hitting the benchmarks,” he says. “We want a change.” Their portfolio includes $250,000 worth of Imperial Oil shares as well as registered and non-registered mutual funds. Their holdings are mostly in funds charging 2.2% in fees, with a whopping 80% weighted in Canadian equities. Their goal? “More income, more tax efficiency, and less fees.”

Cochrane, Alta. residents Edward, 60, and Penelope, 58, retired five years ago. Ed feels grateful to his former employer for his defined benefit pension plan, but he doesn’t feel that way about his adviser of 25 years. “We’re getting mediocre returns—we’re not even hitting the benchmarks,” he says. “We want a change.” Their portfolio includes $250,000 worth of Imperial Oil shares as well as registered and non-registered mutual funds. Their holdings are mostly in funds charging 2.2% in fees, with a whopping 80% weighted in Canadian equities. Their goal? “More income, more tax efficiency, and less fees.”

Calgary money coach Tom Feigs says the Arnesons first need to adjust their asset allocation. Right now, their after-tax guaranteed income for life from Ed’s company pensions is $58,000 annually (indexed to inflation) and will bump up to $78,000 when Ed turns 65. If they can get an average annual 4% return on their portfolio, the couple can easily supplement their lifestyle up to $95,000 in income per year to age 95. However, says Feigs, “they need to moderate their 95% exposure to equities soon to reduce volatility and risk, as well as lower the percentage they hold in Canadian equities to 30% from 80%.”

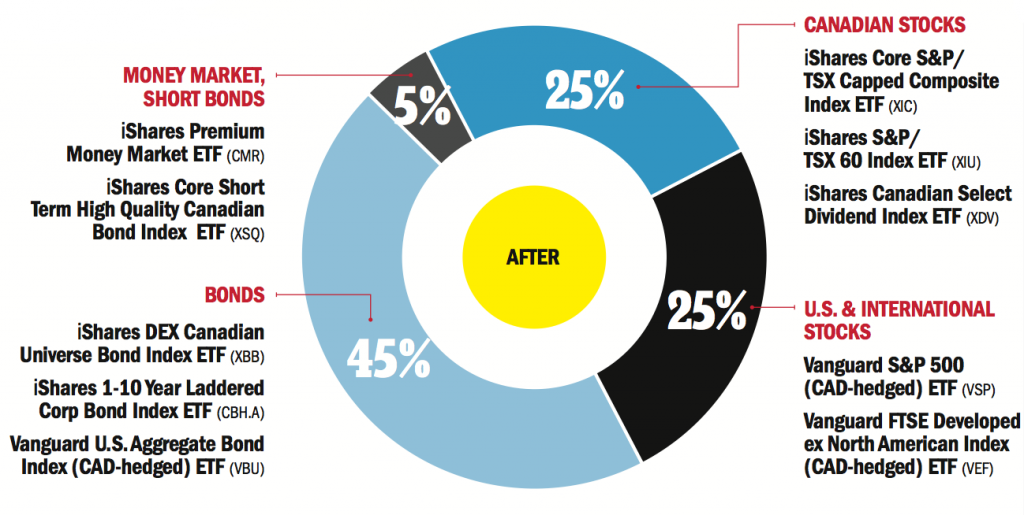

As well, Feigs thinks the fees the couple are paying are excessive. “Any savings in fees boosts returns year after year by thousands of dollars.” Feigs outlines two options. The first is to build a passive portfolio using exchange-traded funds (ETFs) charging just 0.5% or less annually (as shown above)—“but that will mean doing the investing themselves.” A better choice, he says, may be to open an account with a low-fee mutual fund investment firm such as Leith Wheeler or Mawer. These firms will build and maintain a portfolio made up of their own low-cost mutual funds for about 1.2% in fees. Either way, he says, the Arnesons should aim for a portfolio split of 50% equities and 50% fixed income. “This will reduce risk while maintaining a reasonable return.”

To keep taxes low, they should split Ed’s company pension and move funds to their TFSA accounts as the contribution room grows.

Do you want a portfolio makeover from MoneySense? If so, send an email describing your situation to [email protected]

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email