From stock-picker to indexing purist

Newlywed Emily Li wants her investments to work harder.

Newlywed Emily Li wants her investments to work harder.

Emily Li, 29, and her husband, 32, have just $30,000 left on their condo’s mortgage, and in three years or so they want to buy a bigger home. The couple also hopes to retire in their late 50s, and they’re well on their way. They have no consumer debt and their frugal ways have given them a big head start on retirement. Emily is a fan of MoneySense’s Couch Potato strategy and owns a few equity ETFs, but she still holds many individual stocks that would trigger capital gains tax if sold. Is the tax hit worth taking for the peace of mind and better diversification she’d gain from an indexed portfolio?

Emily Li, 29, and her husband, 32, have just $30,000 left on their condo’s mortgage, and in three years or so they want to buy a bigger home. The couple also hopes to retire in their late 50s, and they’re well on their way. They have no consumer debt and their frugal ways have given them a big head start on retirement. Emily is a fan of MoneySense’s Couch Potato strategy and owns a few equity ETFs, but she still holds many individual stocks that would trigger capital gains tax if sold. Is the tax hit worth taking for the peace of mind and better diversification she’d gain from an indexed portfolio?

PWL Capital portfolio manager Justin Bender is a no-nonsense pure indexer and no stranger to the pages of MoneySense. He takes no prisoners when it comes to clients who want to pick their own stocks. In his discussions with Emily, it became clear there were no good reasons for her to own individual stocks, and the one-time capital gains tax of $2,500 was an acceptable trade-off to assemble the kind of set-it-and-forget it Couch Potato portfolio Emily believed she needed. “I’ll trade off capital gains to reduce single-security risk every time,” Bender says.

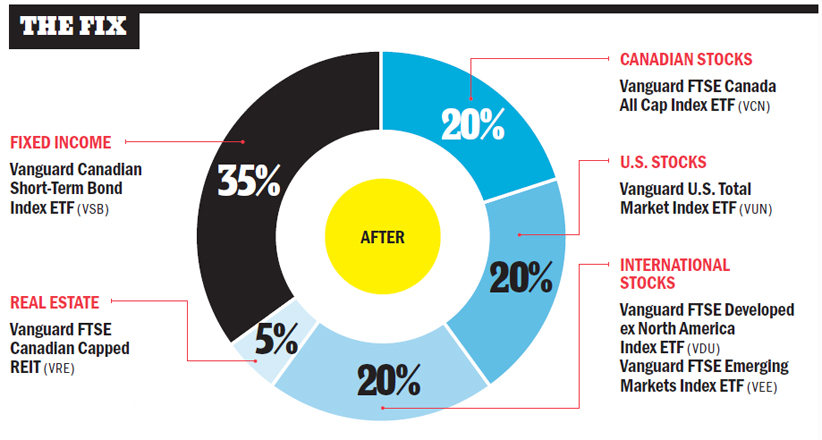

He also took the opportunity to move the portfolio away from an overly aggressive 100% equity allocation towards a more balanced portfolio that includes 40% in short-term bonds and a slice in Canadian real estate investment trusts (REITs). Emily’s new portfolio is now all Vanguard ETFs, and it has a weighted-average MER of just 0.22%.

Now instead of holding much of her wealth in a small number of companies, Li owns about 6,000 stocks from around the world: her equity holdings are split between broadly diversified Canadian, U.S. and international markets (developed and emerging). To avoid currency-conversion charges, the ETFs are all traded on the TSX.

In order to be as tax-efficient as possible across the couple’s accounts, Bender explained the bond holdings should be held in their TFSAs and her husband’s RRSP. The equities, meanwhile, are held in Emily’s taxable account.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email