Investment returns: A great decade, after all

Investors who stayed in the markets have done remarkably well over the past 10 years—something we couldn’t have said as little as five years ago

Investors who stayed in the markets have done remarkably well over the past 10 years—something we couldn’t have said as little as five years ago

Disillusioned. Frustrated. Irate. Those few words likely describe how many investors felt in 2009 when they looked at the long-term performance of their investments. At that time a typical balanced portfolio of $50,000 would have grown to just $64,100—a 2.5% average annual return—after 10 years of being fully invested. Those were the dismal results we found the last time we crunched these numbers. We aptly called it the “lost decade,” since that return more or less matched the rate of inflation over that period.

To be fair, the decade leading up to 2009 was an unusually bad period for markets, as it included both the dot-com crash of 2000–02 and the financial crisis of 2008–09, which nearly spun the global economy into a depression. Either of those events would have been enough to shake investor confidence. Being hit by both of them was just cruel.

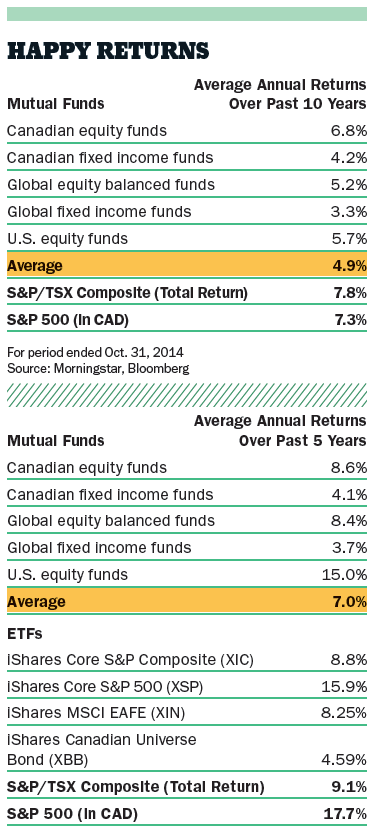

The last decade has been much kinder. While the scars of the financial crisis remain, its overall impact is muted. A balanced portfolio that started at $50,000 in 2006 (20% Canadian equities, 20% U.S. equities, 20% international equities and 40% fixed income) would be worth a little more than $83,000 today, based on the return figures provided in the table to your right. The lion’s share of those gains, though, can be traced to the past five years as stocks recovered dramatically after the financial crisis, with special thanks to a particularly robust U.S. market. Of course, this assumes you held a balanced portfolio, rebalancing regularly. If your portfolio has a different makeup than the one described above then your returns could be quite different, which is why we also break down the portfolio returns by fund type.

If you are susceptible to home bias in your portfolio—that is, the majority of your stocks are Canadian—this next point should give you pause. Over the past five years the average U.S. equity fund returned 15%, juiced by an equity rally that continues today and a surging U.S. dollar. Those returns were so strong they nearly doubled the performance of Canadian equities over that period. (Global equity funds were on par with Canadian funds over that time span.)

Although a typical balanced portfolio did well over the past five and 10 years, investors could have done even better for themselves had they eschewed expensive mutual funds altogether and built a portfolio with lower-cost exchange-traded funds. The last time we built this report ETFs were relatively new and still gaining in popularity. This prevented us from adequately comparing the performance of ETFs versus funds back then. That’s too bad, because it makes a difference.

Looking at just the past five years, a diversified portfolio comprised of the iShares Core S&P/TSX Capped Composite Index ETF (XIC), the iShares Core S&P 500 Index ETF (XSP), the iShares MSCI EAFE Index ETF (XIN) to represent global equities, and the iShares Canadian Universe Bond Index ETF (XBB) would have earned investors an average annual return of 9.34% versus 8.34% for comparable mutual funds. The 1% difference is telling: it’s roughly the difference in fees between mutual funds and ETFs. On a $50,000 balanced portfolio that works out to a difference of about $4,000 over five years.

What’s the takeaway from all of this? Overall, as long as you had a diversified portfolio over the past five or 10 years, you’re better off. Unless you made some big bets on individual stocks it was nearly impossible to have lost money in the markets during that period. This is welcome news, particularly for the baby boomers as they start to retire en masse and draw down their portfolios. They might still be reeling after the lost decade, but clearly they’ve gained ground. Still, this is no time to get cocky. After a prolonged rally in the equity markets—not to mention a surprisingly strong run for bonds—investors can breathe easy, so long as they don’t forget the recent lessons. As the results in 2009 told us, there’s simply no telling when your portfolio will be blindsided again.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email