Investing for the future without a pension plan

Rose's conservatism is holding her back.

Rose's conservatism is holding her back.

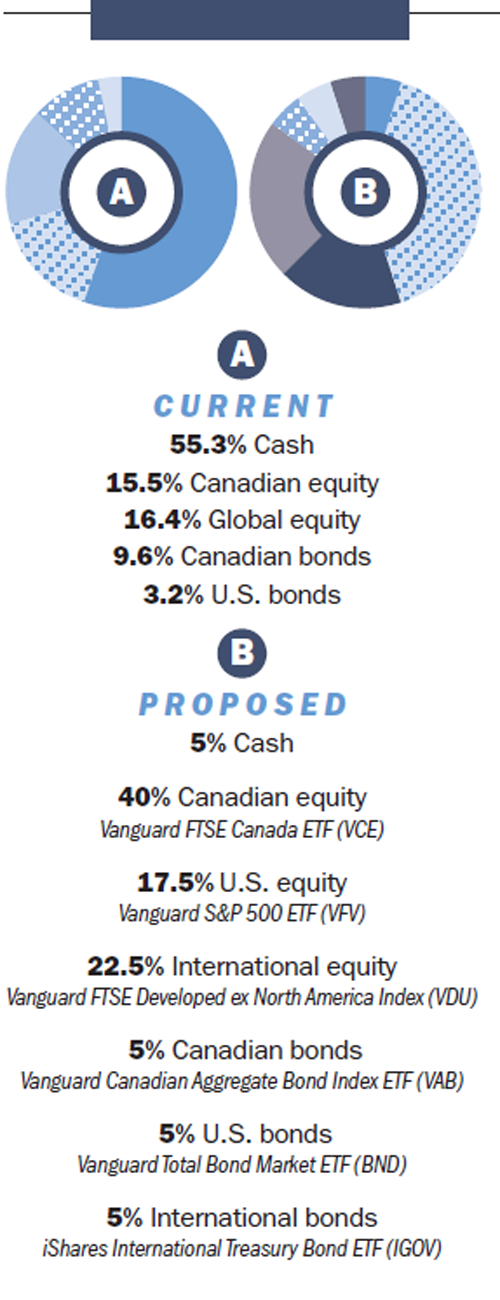

Like many people, Rose Yan, an executive assistant in Vancouver, doesn’t have a workplace pension plan. This means she’ll be largely responsible for funding her retirement. Impressively Rose is meeting that challenge head-on: she’s an excellent saver who has already amassed $112,000 in RRSP contributions. The only thing holding her back from meeting future financial goals is well-defined asset allocation and appropriate risk management. Despite her relative youth, her portfolio is conservative, with 68% in cash and bonds and only 32% in equities. That won’t provide sufficient growth.

The Solution

The SolutionTyler Mordy, president and co-CIO for Hahn Investment Stewards, conducted a risk tolerance questionnaire with Rose. Despite her portfolio’s heavy weighting in fixed-income products, he found her long-term willingness and ability to take risk is quite high. “The best approach is to position her registered account for growth,” says Mordy. “For our clients, that means a strategic allocation of 80% stocks and 20% bonds and cash.” To ensure sufficient long-term growth, Mordy would like to see Rose diversify her risk exposure in the equity portion of her portfolio. This would include emerging markets, although Mordy’s firm would allow for some tactical latitude that would put much more weight on Canadian stocks. Key too will be ensuring that her fees are reasonable. “In most cases this is most easily accomplished through ETFs,” says Mordy.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email