Stocks: The hard sell

Investors love to buy stocks, but selling is much harder. All too often pride, anxiety and neglect keep us hanging onto our losing stocks until it's too late

Investors love to buy stocks, but selling is much harder. All too often pride, anxiety and neglect keep us hanging onto our losing stocks until it's too late

![]() Patricia Price grabs a coffee, powers up her computer, turns on BNN and settles in for another day scouring the investment news on the web for the next stock to buy. When she answers a phone call from MoneySense, it doesn’t take long before she turns the conversation to the mining company Teck, and China’s appetite for resources. “Over the long term copper and coal should do well,” she says. Price delivers her outlook with the confidence of a trader on Bay Street, but in fact she’s a 68-year-old, semi-retired Maritimer in Boiestown, N.B., a speck of a place some 50 minutes north of Fredericton.

Patricia Price grabs a coffee, powers up her computer, turns on BNN and settles in for another day scouring the investment news on the web for the next stock to buy. When she answers a phone call from MoneySense, it doesn’t take long before she turns the conversation to the mining company Teck, and China’s appetite for resources. “Over the long term copper and coal should do well,” she says. Price delivers her outlook with the confidence of a trader on Bay Street, but in fact she’s a 68-year-old, semi-retired Maritimer in Boiestown, N.B., a speck of a place some 50 minutes north of Fredericton.

Today Price is waffling on her next move for Teck after watching her investment tank. She got in on the diversified miner at $58. Like a wise investor, she lowered her average buying cost by adding to her position when shares dipped to $48, and again when they ticked below $38. She lost patience when the shares bottomed out at $26. Time to move on, but her confidence boils away as talk turns to selling. “I want to take my loss on Teck and put it somewhere I feel is much safer, but because it’s starting to creep up again I hesitate to do that.” You can hear the anxiety in her voice.

It’s like a bad romance. Just when you think you’re ready to break up and move on, you get reeled back in. Price isn’t the only one who feels this way. “You look at a company and it goes nowhere; then it flirts with you by going up a bit and down a bit,” says William Corbett, a retired criminal lawyer in Ottawa who manages his own portfolio. “Selling is an emotional thing.”

Emotions muddy the decision-making process, not just for amateurs like Price and Corbett, but for professionals, too. “Business school taught me how to buy, but selling is intuitive,” says Irwin Michael of ABC Funds. “You have to learn that part on your own.”

Sir John Templeton once said the only time to sell is when you need the money. In practice it’s more complicated. The pros will tell you there aren’t many companies worthy of such devotion—especially in a small concentrated market like Canada.

Investments change over time—even the good ones. Take Eastman Kodak. The film manufacturer was a blue-chip stock for more than 70 years and rewarded long-term investors handsomely, especially those who bought it before the Second World War. And then it didn’t. The proliferation of digital cameras made Kodak irrelevant and it succumbed to bankruptcy in 2012, eight years after losing its place in the Dow.

Investments aren’t the only things that change over time; your needs do, too. You may need to sell for an emergency, to transition your portfolio to focus more on fixed income or even for routine rebalancing. It all boils down to this: how do you identify the right time? Here are how some of the best investment minds in the country decide when it’s time to sell a stock.

“Anyone with money can buy stocks, but only smart people can sell them,” says Ted Weisberg, president of Seaport Securities in New York. Sage advice from a man who’s spent more than 40 years as a broker on the floor of the NYSE and runs a successful money management firm. Smart investors need to find a way to separate emotions from their investment decisions. “The sell decision should be wrapped around your ultimate goals,” he says.

To do that you need to know why you bought a stock in the first place: whether it was for growth, as a hedge against inflation or for income. If you don’t have an investment strategy you should ask yourself whether investing in individual stocks makes sense for you. Stock-picking takes time and discipline, and is not for everyone. “Without having a philosophy, you don’t really know the right time to buy and sell,” says Jason Heath, a fee-only planner with Objective Financial Partners in Toronto. “When you act with your heart you are more likely to foul up.” Pride keeps investors from selling losers; greed makes investors hold on to stocks longer than they should.

You need to have an investment thesis, but once that thesis is broken, it’s time to sell, says Jack Mahler, managing director and head of equities at OMERS, one of the largest pension plans in the country. At OMERS that thesis is built on its view of the economics of the business, price discrepancies and the risk/reward. Just don’t let your investment thesis creep, he says. Stick to your guns; otherwise you’re simply making excuses to hold onto a stock that will underperform.

Ask yourself one simple question, says Heath: would you buy it now? Don’t think about the price you paid; think about whether you would put more money into the company at its current price. Most people get caught up in how well a stock has done or to try to avoid selling at a loss, while ignoring the elephant in the room: whether the company is still a good investment.

Investors make mistakes, and it takes courage to admit that. “You have to know where the exits are,” Weisberg says. That’s true for both winners and losers in your portfolio. To make this decision you need to have an endgame when you invest; without one you can’t tell if your investment thesis is panning out or if it’s time to cut your losses.

While short-term shocks scare investors into selling prematurely, long-term investors need to recognize that holding an investment in perpetuity doesn’t always make sense. Anyone who bought and held Nortel Networks learned this lesson the hard way. But you don’t need a spectacular flameout like that to hurt your portfolio.

Patricia Price knows all about the ups and downs of investing. Especially the downs. The second stock she ever bought was China Automotive Systems, which promptly fell from $14 to $8 before she finally bailed on it. Poseidon Concepts is a fresher painful memory. Shares of the oil and gas service company fell off a cliff when it lowered its earnings guidance in November 2012. “A week after I bought it, it dropped. I just about cried,” she says.

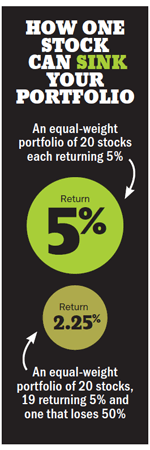

Losses like those can inflict serious damage to your portfolio. Peter Gibson, one of the country’s top equity market forecasters and former chief portfolio strategist at CIBC, has a name for this kind of security: torpedo stock. As the name implies, torpedo stocks can sink your portfolio into the red or, at the very least, cut your returns to less than you’d get from T-bills or bonds. A torpedo stock is any stock expected to fall by 50% or underperform the market by 50%. In the ’80s and ’90s no one really noticed torpedo stocks because most stocks then were rallying 20% or 30%, he says. It’s another matter entirely with average returns as low as they are right now.

Here’s an example. Say you have an equally weighted portfolio of 20 stocks and 19 of them earned an average of 5% and one outlier dropped by 50%. Suddenly your portfolio returned only 2.25%. While there aren’t many companies out there that are going to drop by 50% in a year, it only takes one to sink your portfolio.

Gibson says there’s never been a more important time to look for torpedo stocks, especially with the Dow Jones Industrial Average hitting all-time highs. But how do you spot them? The main thing Gibson looks to is changes in return on equity (ROE), which measures how much profit a company generates with the money shareholders have invested. He then looks at how the current growth compares to the average growth (over four quarters to account for seasonality) and measures the standard deviation. A company with a negative ROE change of 0.3 standard deviations is a sell, and a company with a shrinking ROE of 0.5 standard deviations is a torpedo stock, he says.

Growth, value and income investors all have their own viewpoints on when to buy a stock. Value investors tend to favour lower than average price-to-earnings or price-to-book ratios and high dividend yields. Growth investors hunt for companies with earnings that are expected to grow at a faster rate than their industry or overall market. And dividend investors look for stable businesses that have high yields and sustainable payout ratios.

Too bad they don’t have such strict rules for selling. “There’s no magic number,” says Bill Webb, chief investment officer at Gluskin Sheff and Associates in Toronto. “You have to come up with what you think is the fair intrinsic value for the business.” Look at all the variables you used when you bought the stock—discounted cash flow, price-to-earnings, price-to-cash-flow, net asset value, price-to-book—and use that information to decide what the upside is if the stock rises and what you stand to lose if it drops.

For better or worse, companies are going to surprise you from time to time, so it’s important to stick to the reasons why you bought the company in the first place. “You can get to your one- or two-year target prices more quickly than you expect sometimes. It’s important not to overstay your welcome,” says Webb. “If there is a 4% upside and a 20% downside, that’s not a good risk-reward ratio.” You might be better off looking for another place to use that cash.

Heath is inclined to look at the price-to-earnings multiple and compare it to the rest of the market and the sector. Canadian banks, for example, typically trade around 10 times earnings. When they inch up above 12 times it might be worth considering taking some profits off the table. That’s especially true if those multiples get way out of whack. “It helps to put things into perspective,” says Heath. “When you look at the bubbles in the past that have been built on irrational exuberance, it’s tended to be when price-to-earnings were extreme.”

Of course, fundamentals don’t always tell the full story. “I will sell a stock if you get to a situation where the fundamentals are very positive, but the stock stops responding to positive news,” says Webb. “That usually tells you that the stock is close to fully priced.”

Technical analysis—looking for patterns in stock data to predict future prices—is another popular tool among do-it-yourself traders, but pros caution against relying exclusively on it to make investment decisions. “We’re not aware of any technical indicators that have any validity,” says Mahler. Recent research on common technical indicators suggest they did exactly the opposite of what you might expect.

Most days when David Keil, 36, isn’t investing you can find him sailing, kiteboarding or freediving in the emerald green waters near his home in Turks and Caicos. A few years ago, while studying engineering at the University of Waterloo, you might have found him with friends at the restaurant East Side Mario’s. “That was the hangout,” he says. Given all the time he spent at the restaurant, he felt he had a good read on the company owned by Prime Restaurants, then a publicly traded income trust. Looking back, Keil says his nostalgia for his university life clouded his judgment. Sales were dropping, there was palpable discontent among investors, and the company had no plan to convert from an income trust. Still, he kept cheering management on. All the while, for four straight quarters the CEO would say “we have turned the corner, and we are boldly going forward” in this flat monotone voice. “He was just phoning it in.” Keil sold for about $5 a share, well below the stock’s historical average, but figures he broke even if you include dividends.

Disillusionment with management or a sudden shift in strategy should prompt you to question your investment, says Webb. If in your opinion the change doesn’t make sense, then sell. You need to trust management, which does so many things on a day-to-day basis that investors never see. If you feel management is being evasive it could be enough of a reason to move on. Rising debt levels and the issuance of stock are other points to watch for, as both dilute your investment in the company.

While every investor makes mistakes, there are times where you can do all the right things and still see an investment go south. Corbett recently experienced this with Excelon, a major U.S. utility. “The price-to-earnings was excellent, price-to-book was good, the dividend was around 5%. It’s a utility for Pete’s sake, how can you lose on a utility?” he exclaims. “Well, you can if Sandy knocks them out across the Eastern Seaboard for six months.”

Unexpected events like these shouldn’t dissuade you from holding onto an investment. “Most people like to ride with a winning team and tend to sell their losers because they can only take so much pain,” says Irwin Michael of ABC Funds. But a loss due to something outside the company’s control shouldn’t shake your confidence, especially if your investment thesis still holds.

Rules can help take emotion out of trading. One rule of thumb that several money managers recommend is to sell your investment if it unexpectedly drops 10% for no obvious reason, especially if the rest of the market doesn’t match that drop. Critics say this promotes panic selling and undermines the reasons for buying a stock in the first place. They argue that if a stock drops suddenly you should take the opportunity to do some dollar cost averaging. Applying this rule to small or illiquid stocks is problematic, because the share price is more prone to larger swings as investors suddenly have to sell.

Proponents counter that by the time you’ve figured out why a stock is falling, you may have lost another 10%—or more—which can be hard to stomach. By putting a bottom on losses, you limit downside risk. You can set this up automatically by putting a stop loss in place to sell once the stock falls below a certain level. Investors can also use options to limit the downside on a stock. While options provide a form of insurance for your portfolio, it comes at a cost and can limit your upside.

Maintaining strict rules around how you manage your portfolio will keep you out of trouble and help prevent panic selling that can do real harm to the portfolio. Do-it-yourself investors are particularly prone to selling at the wrong times, says Heath. Many will have sold their positions in Europe because it is in recession, but often in cases like this they should be doing the opposite.

A well-balanced portfolio will help reduce the volatility that can make investors jumpy. Limiting holdings of any single stock to perhaps 5% of your portfolio is crucial to reducing risk. If an investment in your portfolio exceeds that threshold, sell enough to bring it back under your target threshold, says Heath.

Sticking to such rigid rules can be tough, especially if you feel there may be some upside left in the stock. But the pros say you have to get over it. “I resign myself to always leaving a bit of money on the table,” says Michael. He gives two important reasons for this: you can’t be right all the time and after a stock has doubled or tripled the guy you’re selling to has to feel he can make some money—especially when you’re selling thinly-traded stocks. “You can’t be too greedy.”

The recent takeover of Nexen by China’s CNOOC is an apt illustration. Its shares soared more than 50% after the offer, to within a dollar of the proposed sale price. Holding out for the merger to close would only have netted you an additional 3.8% while Ottawa mulled over the deal. The risk was what would have happened if the decision went the other way. Had that happened the stock likely would have dropped back to its pre-takeover levels, resulting in a loss of 30%.

Given the time it has taken to close this deal and the political posturing around it, it’s hardly worth the risk of giving up the 50% gain for an extra few percentage points. Unless you were expecting a new offer to come in and drive the price higher, in cases like this it’s probably a good time to sell and move on and let someone else assume the risk.

As much as investors like to pick their spots, you can’t always control when you sell. Any number of factors can affect your timing: you could need the money for other purposes or maybe you’re shifting your investment focus away from equities.

If you’re selling down the equity portion of your portfolio, Heath suggests trimming all positions simultaneously to avoid selling one company at the wrong time. “It’s like dollar cost averaging in reverse,” he says. Keep in mind, however, that this approach can increase your trading commissions.

Where investors can really get into trouble is when they start making changes too quickly. That’s where having a long time horizon can help, says Mahler. “A shorter time horizon is where the individual does the most harm and they incur all the costs that go with it,” he says. You have to give your investment thesis time to play out.

Beyond fundamentals and changes to your personal situation, another factor that could guide your sell decision is taxes. If investors are looking at a large number of capital gains they may want to do some tax-loss selling in non-registered accounts to offset them, says Heath. Harvesting capital losses—even on investments you like—in order to offset capital gains can be a wise strategy. If you still like the companies you can always buy them back after 30 days to avoid being deemed a superficial loss. But don’t hold on to the stock just to avoid taxes, adds Michael. “A lot of retail investors won’t sell after a big gain because they are afraid to pay taxes,” he says. “In my mind if you’re paying capital gains taxes you’re making money.” Holding on to a stock too long just invites unnecessary risk.

Whether you’re an active trader or a long-term buy-and-hold investor, selling should be a tool to keep at your disposal. All investors need to check up on their portfolios from time to time, but at the end of the day, resist the urge to do too much tinkering. “The more decisions you make, the more your portfolio trends towards average and the higher number of errors creep into your decision making,” says Hugo Lavallée, manager of Fidelity’s Canadian Opportunities Fund. “No one is asking you to be perfect because you can’t be when you’re investing,” adds Michael. “The only people who sell at the top or buy at the bottom are liars.”

For now, Corbett, the retired lawyer, is holding off selling his investments. But in the months to come, he has decided he will sell some top performers, starting with Telus, which represents 10% of his overall portfolio. “Knowing when to sell is difficult, but I’m more comfortable with it now,” he says. His sell decisions have been driven by two things: routine rebalancing and the need for money.

Corbett has learned the critical balance between having the patience to see his strategy through and knowing when to move on. It’s the sweet spot upon which pros like Weisberg of Seaport Securities have built successful investing careers. “If you’re right a few more times than you’re wrong,” says Weisberg, “you’re going to make a lot of money.”

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Food and beverage company expects organic growth of 4% in 2024

General Motors reports strong first-quarter profits as prices help offset small U.S. sales dip.

New analysis from the National Institute on Ageing makes a strong case for delaying Canada Pension Plan payments to...

A pattern in the markets works—until it doesn’t. Investors will be better off focusing on the fundamentals.

Bitcoin’s next “halving” is right around the corner. Here’s what you need to know.

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Earth Day is on April 22. Here’s how to invest sustainably, and other ways to help the planet.

Understanding industry jargon can make you a better real estate investor.

Capital gains tax inclusion rate will increase (for some), Netflix chills, U.S. bank earnings solid, and will the loonie...

Tech industry warns that the budget's capital gains proposals could cause “irreparable harm.”