Organize your finances

Print out “Worksheet 2-Gather your documents.” (You printed this out in January but if not, or you print it again)

It’s a checklist to help you pull together what you’ll need before you start, including bank statements, credit card statements, and life insurance polices.

Once you have all your documents in front of you, you’re ready to fill out “Worksheet 3-Your net worth statement.” (You printed this out in January, but if not, you can find that here: Worksheet-3B-Summary-net-worth-statement

First list the values of all of your assets, including your home, your cars, your cash and investments. Then list your liabilities, including credit card debts, your mortgage and any other outstanding loans. Tally both your assets and your liabilities and transfer those amounts to the following section, your simplified net worth statement.

Finally, subtract your liabilities from your assets to discover your true net worth. This shorter net worth statement gives a clear snapshot of exactly where you stand today.

×

Should you buy a condo?

When it comes to lifestyle, condos offer both young and old a more carefree approach to living expenses and maintenance. Check out our guide to buying a condo here.

×

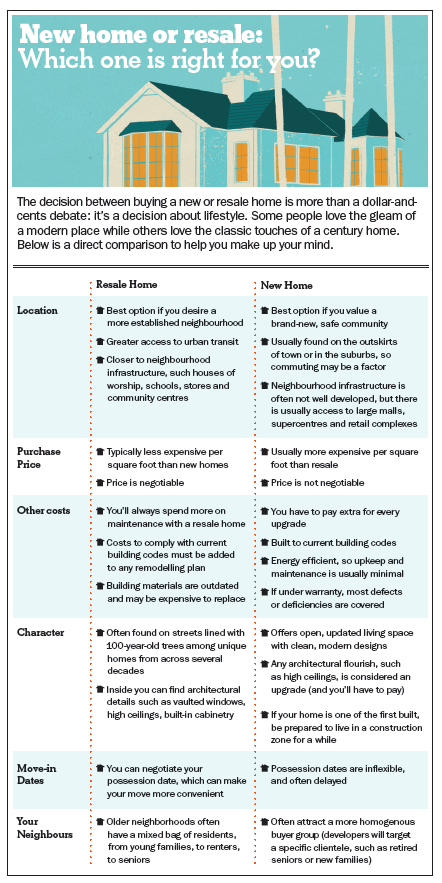

New home or resale?

We’d all love to buy a new home but often downtown neighbourhoods have a full stock of mostly older and resale homes. Find out which one is best for you and your family here.

×

Watch out for these tricks

When you’re looking to buy a house and are in the market for the best mortgage rates possible, you may decide to use a mortgage broker. But be careful. Most brokers only negotiate with a few lenders on your behalf. And to find out what else you should know before signing on the bottom line of any any mortgage, check out these 5 things the mortgage broker isn’t telling you.

×

Be careful when looking for a mortgage

When you’re looking to buy a house and are in the market for the best mortgage rates possible, you may decide to use a mortgage broker. But be careful. Most brokers only negotiate with a few lenders on your behalf. And to find out what else you should know before signing on the bottom line of any any mortgage, check out these 5 things the mortgage broker isn’t telling you.

×

Money fit reader tip

Search for tax breaks and credits. For several years before we bought our first home—a four-bedroom, two-storey house that we plan to raise our growing family in—we saved money using the first-time Home Buyer’s Plan. We withdrew the maximum $50,000 between the two of us tax free and that was enough for a 20% down payment. We also split our mortgage in two (a 5-year and a 10-year), which gives us some protection if interest rates rise. There’s no extra fee for doing this and we can add lump sum payments.”

– Jessica and Christopher Pitt 28 & 38, Calgary

×

Your Action Plan

Start off by ensuring that you’ve organized all your important documents into a fold-out file system. Include bank statements, your will, powers of attorney, mortgage statements, tax returns, life insurance policies, powers of attorney, etc. Having all of these important documents within easy reach is a huge time saver. Then make sure that family members and friends know exactly where to find those documents in case of emergency. Second, if you’re a homeowner, or simply looking for a home right now, be sure to read the MoneySense “Guide to buying and selling a home.” Even if you’re not in the market right now to buy a property, understanding all the basics will come in handy when you do decide to either buy, sell, upsize or downsize your home. Better yet, you can be a fountain of information for friends and family when it comes time for them to buy a home. Of course, if you like the house you’re living in now, and are considering doing some renovations, make sure to do up a separate budget for those. Ensure you have enough money on hand—or have access to a low-interest rate equity line of credit—before you start tearing down walls. Then make sure you moniter your budget weekly so you don’t overspend. And finally, fill in your net worth statement so you know where you stand.

×

{kind=link}