How your credit score works

What's measured, how to read it and what it will cost you.

What's measured, how to read it and what it will cost you.

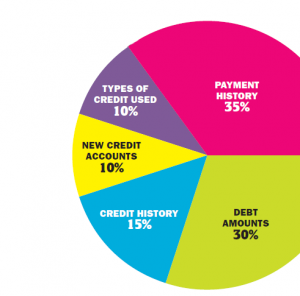

The FICO score, the basis for most credit scores, consists of five major categories based on data in your credit report. The percentages in the chart reflect how important each of the categories is in determining how your FICO score is calculated. The biggest factors are how much debt you have, whether you’ve paid your bills on time and how long your credit history is. You may also be penalized if you don’t have a good mix of types of credit and if you’ve opened too many new accounts recently.

The FICO score, the basis for most credit scores, consists of five major categories based on data in your credit report. The percentages in the chart reflect how important each of the categories is in determining how your FICO score is calculated. The biggest factors are how much debt you have, whether you’ve paid your bills on time and how long your credit history is. You may also be penalized if you don’t have a good mix of types of credit and if you’ve opened too many new accounts recently.

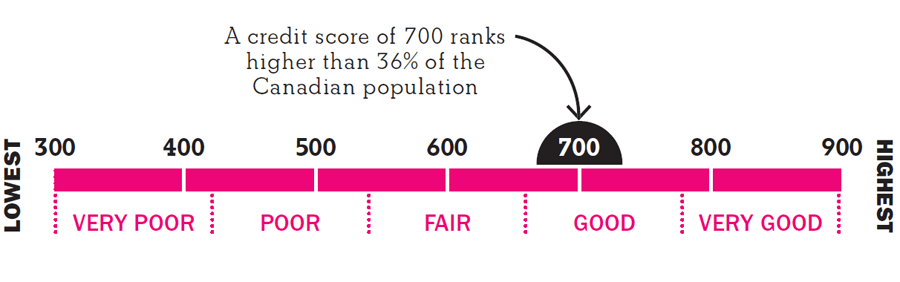

Your credit score rates creditworthiness out of a possible 900 points, and compares your credit standing to that of other Canadians. Lenders generally consider you a good credit risk if your score falls between 660 and 724. Anything below 560 is poor.

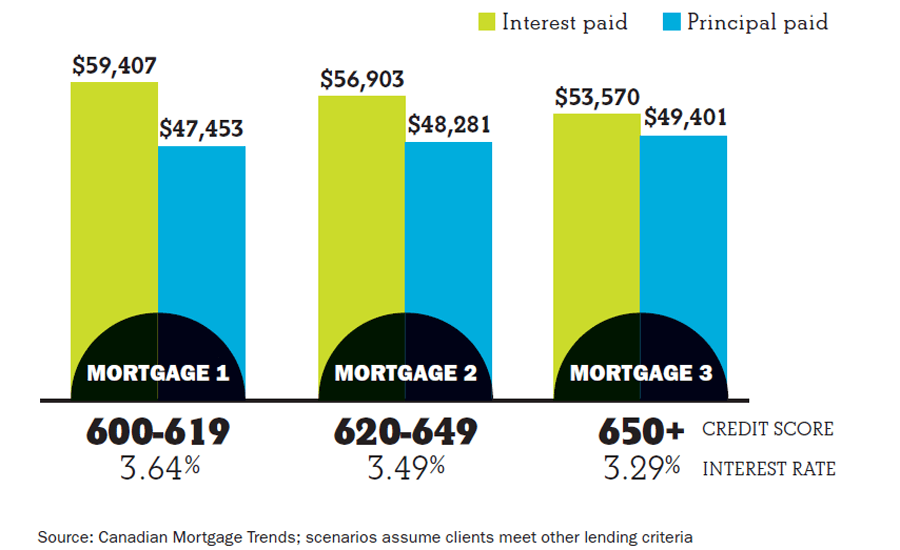

Homebuyers’ budgets will stretch much further if they have an optimal credit score. Consider these three different lending scenarios for a five-year fixed mortgage, based on the purchase of a $370,000 home with a 5% down payment. The lending rate increases as the credit score decreases, costing the buyer thousands of dollars more in interest and reducing the amount paid to principal. In this scenario, the homebuyer with the lower credit score ends up paying more than $6,000 extra in interest when compared to a buyer with good credit.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Learn how the federal government’s 2024 budget can affect you and your money.

Gen Z isn’t immune to phishing scams. Find out the most common schemes targeting young Canadians and how to...

Doing home renovations? Find out if there are any tax incentives that Canadians are able to claim.

U.S. inflation comes in hot, Delta says revenge travel is alive and well, doubling your CPP benefits, and AI...

History repeats (or rhymes) itself in latest market upswing, FHSA celebrates its first birthday, investors getting rich from stocks,...

Money in a LIRA or LIF is intended to last a lifetime, making it difficult to access more than...

As a student, it’s good to build a credit history while earning rewards for groceries, flights, movies and more....

Canada may be likely to avoid a recession, but we won’t start recovering until the second half of 2024,...

What a car loan can do to your credit and borrowing capacity, and how interest and add-ons really do...