A low-income dilemma

Will Joanna's family lose their benefits if she goes back to work?

Will Joanna's family lose their benefits if she goes back to work?

One sunny fall afternoon 12 years ago, Joanna Murphy was happily entertaining friends and family with an outdoor barbecue of steaks and ribs when she heard a huge bang from her garage. In a freak accident, the still her husband Ted was using to make vodka exploded, shooting debris everywhere. Ted, a machinist, was killed instantly. “At the time, I was three months pregnant with my youngest son,” says Joanna, 52, of Windsor, Ont. “I’ve been raising my three boys on my own for almost a decade now, but I still miss Ted. He was the love of my life.”

Joanna, a former nurse, is still thankful for one of the last financial conversations she and Ted ever had. (We’ve changed names to protect privacy.) “We had two young boys at the time and another on the way, so I brought up the idea of getting life insurance,” says Joanna. “Ted agreed, though he didn’t believe in it. But that money allowed me to pay off our modest mortgage, put the rest in the bank and stay home to raise my kids. I had some assets from a previous marriage but the $190,000 in life insurance I received was a life-saver. You never think you’ll need it, until one day you do.”

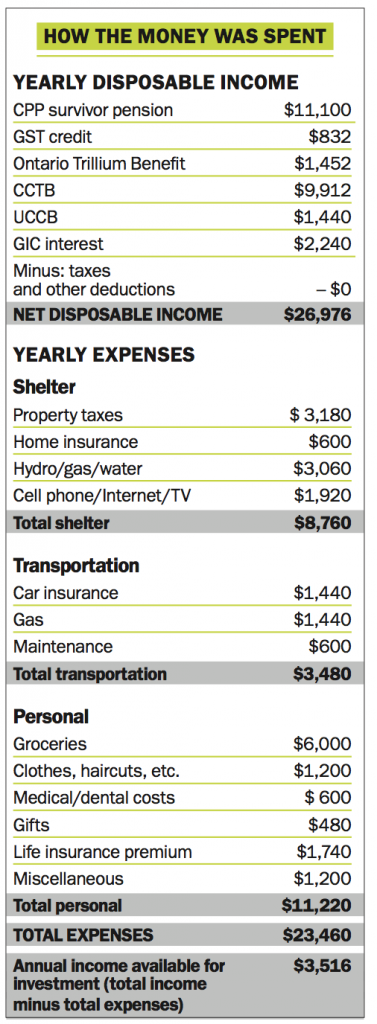

Since she hasn’t worked in over a decade, Joanna lives on an annual income of about $27,000, which consists of CPP survivor benefits, the Canada Universal Child Care Benefit (UCCB), the Canada Child Tax Benefit (CCTB) as well as $2,240 in interest from GIC rates. Her eldest son, 21-year-old Alex, no longer lives at home, but her sons Peter, 12, and Paul, 9, still do. As a result, Joanna’s primary focus is to ensure she gets the most from every penny in her slender budget.

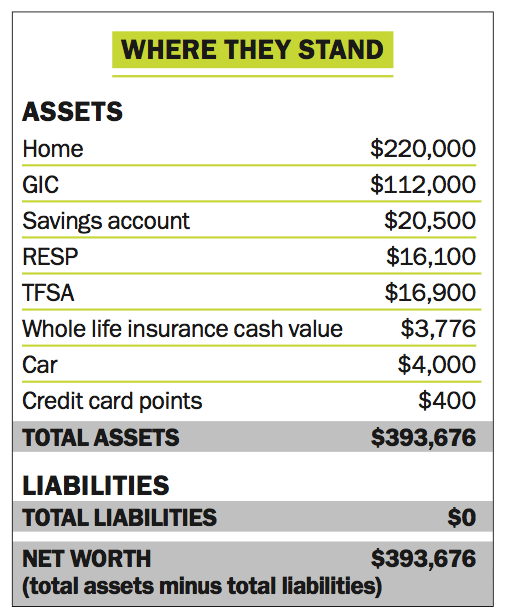

Given her tiny income, the assets Joanna has built up for her family are impressive. Her mortgage is paid off and her home is worth $220,000 under current market conditions. She has $112,000 in GICs, $20,500 in a savings account, $16,100 in an RESP and $16,900 in a TFSA. She also has a whole life insurance policy worth $103,000, with a cash value of $3,776, as well as a $100,000 term policy that expires in two years. “Since Ted died, I’ve tried to make good financial decisions but now I need some direction for what to do with my life and my money over the next decade and heading into retirement.”

At this point in life, Joanna says she has four major goals: to decide whether it makes financial sense to return to work, to strategically utilize RESPs for her two youngest sons, to get better investment returns for her money, and to understand how CPP will be calculated for her personal situation when she turns 60 or 65.

Despite all these questions, Joanna doesn’t anticipate any major life changes, apart from maybe getting a part-time job. “I’d like to stay in my home for nine more years, until my youngest, Paul, completes high school,” she says. At that point she plans to rent a modest apartment. “Based on my projected expenses, I think I can achieve this. But if I can make some extra money without putting our benefits at risk, I’d love to do it.” Now that her kids are old enough to stay home, it feels like the timing’s right, but since most of her nursing skills are outdated, Joanna knows that any job she takes would likely be outside of her field and pay minimum wage. “Would that even be worth it?” she wonders. “If you pass certain thresholds in household income you can lose Trillium health and drug benefits as well as some kids’ education credits. I don’t want to jeopardize that.”

Those education benefits are important to Joanna. Both Peter and Paul are gifted at math and they’d both like to be engineers when they grow up. Up until now, Joanna has put money in RESPs and, because of her low income, collected the 40% top-up in grant money. That breaks down into a 20% top-up from the basic Canada Education Savings Grant (CESG), which is offered on all RESP contributions, as well as an additional 20% CESG that’s given to low-income families. Joanna also receives a $100 Canada Learning Bond, and will continue to receive this extra RESP money as long as she qualifies for the National child benefit (and until each boy turns 15). “I expect the boys to pay for some of their education costs but they’ll want to graduate with little or no debt.”

Still, Joanna has a lot of questions. For instance, how will her family’s current income be impacted by her part-time earnings. Or, more specifically, how will changes being implemented by the Liberal government to the Child Tax Benefit, coupled with the changing thresholds for marginal income tax rates impact her benefit payments? “Households with incomes below $30,000 will receive maximum child tax benefits,” says Joanna. “Will working part-time mean I will receive less?”

Joanna also has questions about the proposed Ontario Liberals’ free post-secondary tuition program for low-income families. “My boys may benefit from possible free tuition, but will the money invested in RESPs disqualify them? I don’t want to invest any more if that’s the case,” she says.

There’s also the matter of her own savings plan. Right now, she only earns 2% on the bulk of her savings, which are invested in GICs. “I hate risk, but GICs give such low returns. I could definitely use investment advice.”

She worries, too, about the risks of not renewing her term life insurance when it expires in two years. Right now she’s torn between renewing her current term life policy, investing more in her whole life policy, or applying for new coverage. She confesses, the only reason she hasn’t done anything is because she’s afraid of higher premiums. “My health isn’t too great.”

Making matters more confusing, Joanna has no clue how her CPP will be calculated once she hits retirement age. Ted was Joanna’s second husband. After graduating from nursing college in the 80s, she married her high school sweetheart, Doug, who is Alex’s father. They divorced some years later, but remain friends. “Would my monthly payments be calculated from my own contributions as well as from my late husband’s and my ex-husband’s?” she asks. “When Doug and I divorced the agreement specified that I’d get a portion of his CPP but I imagine that’s null and void now, or is it?”

For Joanna, understanding the details is important. Her father was a carpenter who paid for everything up front. “He built our house in stages so he could pay cash. With seven brothers and sisters, hand-me-downs were part of our daily lives but we never lacked for anything.” She’s raised her boys the same way. Despite her family’s small income, she feels her boys have never missed out. Both Peter and Paul are involved with volunteer groups that arrange outings, such as games of laser tag, nature walks and neighbourhood suppers. Another advantage is that both boys have learned to be money wise. “Paul got a $10 gift certificate to McDonald’s for his birthday and he decided to buy just the fries on each visit,” says Joanna, “just to stretch the fun.” Plus, Joanna and her boys take the odd trip to Niagara Falls or Thunder Bay, Ont., to visit their uncle. “The boys lead a very full life.”

It’s a testament to Joanna’s shrewd planning that she manages to stretch her small budget as far as she does. But now she wonders what she should be doing to prepare for the future. What she wants are happy adult boys and a comfortable retirement. “I don’t think it’s too much to ask.”

Joanna’s good budgeting and saving skills are to be admired. “With a bit more understanding of how government benefits and grants work, she and her boys can continue having a comfortable life,” says Vickie Campbell, a certified financial planner with Ryan Lamontagne in Ottawa. To keep on track Joanna should do the following.

Return to work. Joanna’s been fretting over this, and the advice from the experts is to just do it. Her current income comes primarily from her CPP survivor’s pension and Canadian Child Tax Benefits. “If she goes back to work, the CCTB would start to be clawed back once she’s earning more than $30,000 in income,” says Campbell. “But by going back to work she would qualify for the Working Income Tax Benefit (a refundable tax credit), as long as she earns $3,000 or more each year. Even though Joanna would lose some benefits, she’d still be further ahead by getting a job,” says Campbell, who adds: “She can safely earn $15,000 annually and still come out ahead.”

Understand how benefits work. Because Joanna currently relies on child benefits as part of her income, she’ll need to plan ahead for the years when Peter and Paul no longer qualify for the CCTB. At present, these benefits bring in $10,800 in income each year (about $1,000 more in 2016 than they did under the old benefit program). She also receives an additional $2,671 from the new Ontario Child Tax Benefit. But by age 60 she’ll lose more than a third of the family income, when both boys turn 18 and these benefits stop, says Campbell. Joanna could count on an extra $5,600 each year from the CPP children’s orphan benefit, says Campbell, as long as both boys are enrolled in a post-secondary school. She should keep in mind, though, that this monthly rate (which is currently $234.87, but is adjusted annually) will only be available until each boy turns 25. If she decides not to work during this time, she’ll have to rely on her savings and CPP to get her through. The good news, says certified financial planner Jason Heath, is Joanna will be entitled to CPP credits from her first husband as well as a survivor benefit from her second husband. “Her own CPP credits, combined with the credits from her two former husbands, may increase her entitlement up to the equivalent of one full CPP retirement pension, which is just over $13,140 per year,”says Heath. She should visit Service Canada to get clarification on this as soon as she turns 60.

Stay insured. Joanna’s insistence on insurance has saved her in the past, and she should keep it up, says Campbell. However, some health issues a few years ago—issues Joanna doesn’t like to discuss—may make it harder for her to qualify for any type of life insurance in the future without having to pay a big premium. “Her term policy may allow her to renew without medical evidence but her rate will probably still be much more than it is now,” says Campbell. “Still, in the event of her death, she should take solace in the fact that her boys will have her assets, as well as her whole life policy, which may be enough.”

Keep building RESPs. While Joanna is banking on the boys getting scholarships, Campbell suggests she continue investing in RESPs. Regardless of how much she earns, Joanna will receive the 20% CESG top-up. But to qualify for the 20% top-up, she’ll need to keep her yearly income below $45,282. Do this and Joanna’s boys will also qualify for free Ontario tuition (as long as her annual income is below $50,000). “Use the RESP money for books and additional living expenses,” says Campbell.

Get an investment plan. While stocks aren’t for everyone, Heath stresses that low returns on GICs coupled with rising prices means “Joanna is barely keeping up with inflation.” Campbell adds that if Joanna wants to invest in equities she should review her risk level with an advisor and only allocate a small portion of her savings—about 20%—to a balanced portfolio. “She’s conservative and too dependent on her capital to be riskier.”

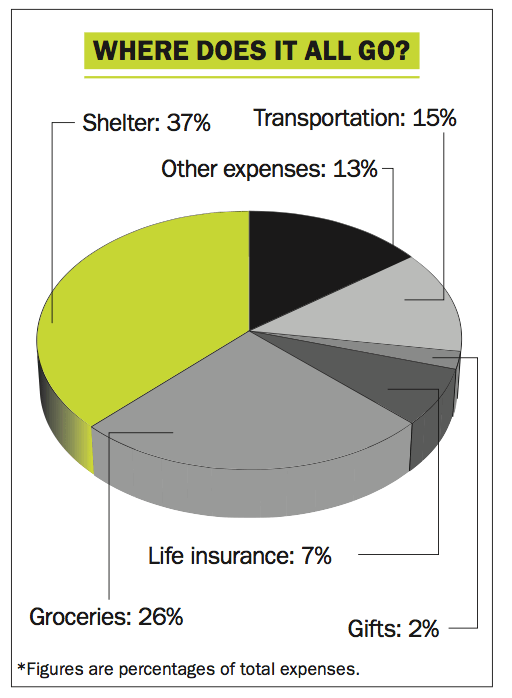

Keep the house. The cost of living in her mortgage-free home is just $3,180 in property taxes and $3,060 in utilities. Compared with the cost of renting an apartment, she’s much further ahead, says Campbell. “She may want to consider selling her home at a later date when she no longer wants to deal with the upkeep but holding onto it for a few years longer will bring her some added security in her retirement years.”

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Tech industry warns that the budget's capital gains proposals could cause “irreparable harm.”

Learn how the federal government’s 2024 budget can affect you and your money.

Gen Z isn’t immune to phishing scams. Find out the most common schemes targeting young Canadians and how to...

Cards that waive or refund the fee for foreign currency charges are few and far between—but if you’re a...

The data behind the top places to buy real estate in Canada.