Tame the debt monster

If we want to get out of our debt cycle we need to plan a way out of bad habits

If we want to get out of our debt cycle we need to plan a way out of bad habits

[brightcove video_id=”6023926371001″ account_id=”6015698167001″ player_id=”lYro6suIR”]

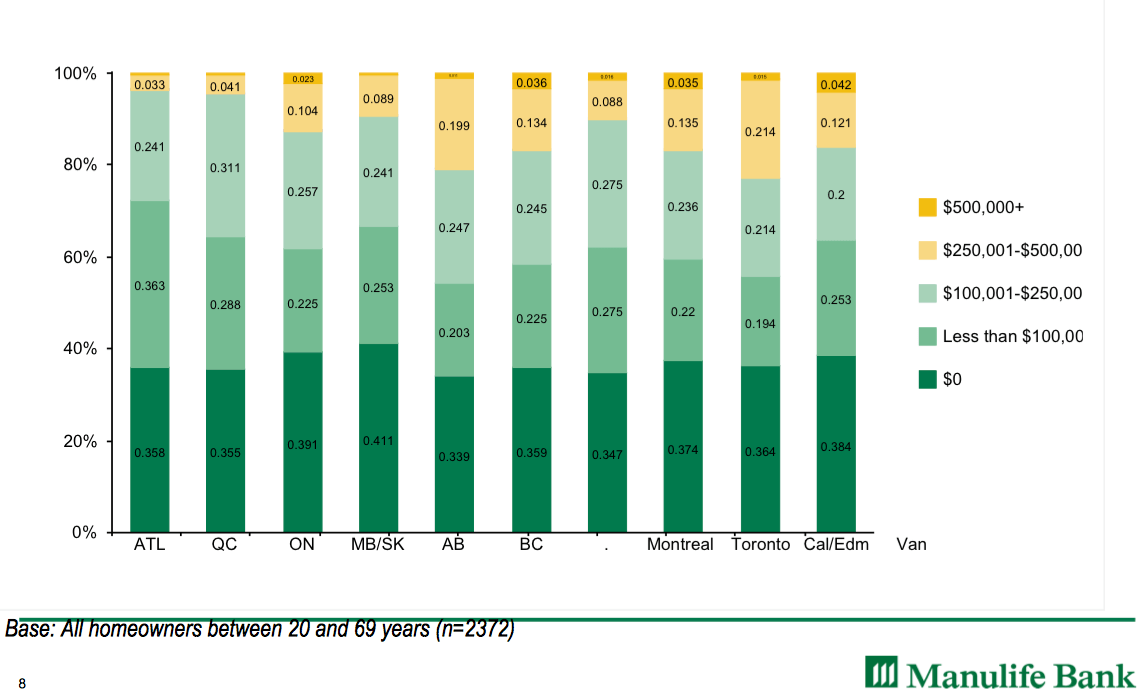

Would $1,000 in the bank cover all your bills for the next six months? Probably not. And yet, about a quarter of Canadian homeowners confess to only having $1,000, or less, set aside for an emergency.

These are the findings of the latest survey by Manulife Bank of Canada. Turns out, more than a third of mortgage holders in Canada would have difficulty making their regular mortgage payment within three months if the main income earner in their household lost their job. Yet, experts, including Manulife Bank, recommend that each household keeps enough in emergency savings to cover three to six months of expenses.

“A high-interest savings account is a good option. Or, if you’ve got a home equity line of credit, you could use your savings to reduce your debt and save interest – and still have access to that money if an emergency arises,” said Rick Lunny, president and CEO of Manulife Bank of Canada.

The concern is that Canadians are living beyond their means—a situation that’s grown over the last decade along with surging real estate prices. According to the Manulife survey, 40% of homeowners have difficulty managing common expenses associated with home ownership, let alone creating a financial buffer (commonly referred to as a “rainy-day fund” or “emergency savings”).

It appears that up until very recently, Canadians were heeding the advice of experts and cashing in their emergency funds. The idea was that if you lived in a financially stable household, it actually made more sense to use that cash elsewhere and open up a line of credit that you could use if there was a crisis. The theory was that the cash sitting in an emergency fund—typically in a high-interest savings account or a money-market fund—was earning less than what your debt cost you. Rather than keep the emergency fund, many Canadians used it to pay down their debt.

But with recent headlines of mortgage rate hikes and a potential increase in U.S. interest rates (which would prompt an increase in Canadian interest rates), the idea of having an emergency stash of cash is back in favour, particularly if you, like one in six Manulife survey respondents, who would encounter financial difficulty with any increase to their mortgage payment.

“A financial buffer is an important part of a financial plan,” said Lunny. “If you don’t have extra cash at the end of the month, it’s very difficult to build a rainy-day account. For those who find themselves in this situation a good place to start is working with an advisor to create a budget. Many people are surprised at how much of their money is going toward things that they don’t consider that important.”

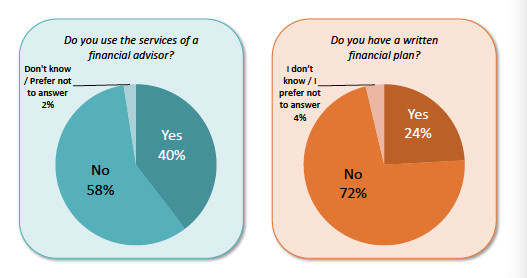

According to a new study sponsored by Mackenzie Investments, 72% of Canadians didn’t have a written financial plan.

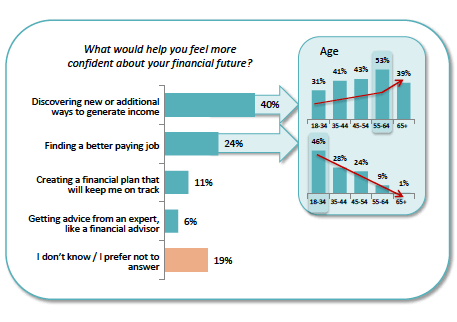

In the same survey, more than two-thirds said that the solution to feeling more secure in the future was to either discover new or additional ways to generate income or to find a better paying job. In other words: more money, less problems.

But professional money coaches know this isn’t actually the solution to debt problems. As Sheila Walkington, co-founder of Money Coaches Canada, has told us in the past, a key component of her job is to “help clients deal with the psychology of money. To help them shed their negative attitudes and bad habits and to motivate them to get a grip and stop self-sabotaging their financial goals.” Yet, in the recent Mackenzie survey, only 11% acknowledged that developing a financial plan would help and 6% believed that advice from a professional would help.

In the past, MoneySense has advocated strongly for the development of a financial plan. As award-winning journalist, Julie Cazzin, writes: “[a] personal finance plan is [a] road map, helping [you] navigate to [your] dreams. And the roads to those dreams were built on details.”

To establish your own financial plan, check out the 11 Steps to Financial Freedom, which includes worksheets and tips on how to create the right financial plan for you.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

New analysis from the National Institute on Ageing makes a strong case for delaying Canada Pension Plan payments to...

A pattern in the markets works—until it doesn’t. Investors will be better off focusing on the fundamentals.

Two siblings’ complex inheritance provides a case study in minimizing death taxes.

Managing lifestyle creep is challenging financially and psychologically, especially with inflation. Expert strategies keep day-to-day spending in check.

Bitcoin’s next “halving” is right around the corner. Here’s what you need to know.

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Capital gains tax inclusion rate will increase (for some), Netflix chills, U.S. bank earnings solid, and will the loonie...

Tech industry warns that the budget's capital gains proposals could cause “irreparable harm.”