Widowhood: Reassessing finances and life goals

With the recent passing of her husband, Marina Wilkinson is in the process of reassessing her finances and life goals. What should she prioritize?

With the recent passing of her husband, Marina Wilkinson is in the process of reassessing her finances and life goals. What should she prioritize?

Marina Wilkinson is sitting alone at the kitchen table of her two-storey, four-bedroom home in Beaverlodge, Alta., sipping a cup of tea and trying to organize the rest of her life. The task is overwhelming. It’s been two months since her husband Roderick died, following a 25-year struggle with an immunological disease. Marina is still feeling the emotional pain of losing her partner, but adding to her anxiety is another type of burden. “I’m totally at sea with all the finances,” says the 59-year-old widow and mother of two adult children. “This isn’t through lack of experience because I handled all our money matters during our 39 years of marriage. It’s about how to put a plan in place, as well as making good personal decisions, so I can move on. Now my husband has passed away, I need a new blueprint for my life. It’s daunting.”

There are countless important decisions that need to be made. “I work full-time and it was always my intention to work as long as Roderick was alive—at least until age 65,” says Marina, who earns $45,000 annually as a secretary at a dental clinic. (We’ve changed names to protect privacy.) “But I’ll soon receive the survivor benefit from Roderick’s government pension and don’t know how that will affect my tax picture. I certainly don’t want to continue working if I’m just going to end up giving away all the money to the taxman.”

Other key decisions for Marina include how to invest the proceeds of a $245,000 life insurance policy, and whether she should sell her spacious Beaverlodge home to move to a duplex on Vancouver Island, which she inherited with sister Joy in 2010. The duplex had been rented out, but Joy is moving into the upstairs unit, leaving the lower one available for Marina. Ideally, Marina would like to leave work and retire in June of 2015. At that time, she could move to Vancouver Island to live with her sister, an appealing prospect. “I’m all alone now. I need to be realistic,” says Marina, originally from Victoria. “It’s cold in Alberta in the winter—40 below zero some days. I’d enjoy living in a milder climate and being closer to friends.”

Holding her back are several difficult choices she needs to make if she decides to go ahead with the plan to sell her Beaverlodge home. “It will need to be renovated first, but I can always take in a boarder or two to help with the expenses until I leave my job,” says Marina. “Or, should I do some minor renovations and sell it sooner? It’s hard to decide.”

Finally, she’s contemplating if she should just “rent out a couple of rooms in this big house,” and stay in Beaverlodge.

Without question, Marina’s current home carries deep emotional ties. “My husband and I built our house in Alberta in 1995, after living in a mobile home for 16 years. “We had been told that with Roderick’s illness, we would never qualify for a mortgage,” she says, information she later found out was incorrect.

It was in the 1970s that Marina first met Roderick through mutual friends at a family barbecue. “It was love at first sight,” she says of her geologist husband. By 1975 they were married and Marina left behind her university studies to work full-time as a receptionist. In 1979 they settled in Beaverlodge and immediately had two children, with Marina staying at home to care for them. Then disaster struck. Roderick was diagnosed with the immunological disease in 1984 and the next few years revolved around taking him to appointments and generally running the household.

In 1988, things slowly returned to normal and Roderick’s disease was under control, so Marina returned to work. Over the years, Roderick continued on with his provincial government geologist’s job. For the last 13 years of his life his long-term disability paid him 70% of his initial salary of $42,000. His employer, however, continued to contribute to his pension.

Today, Marina is entitled to a survivor benefit of $32,875 per year (which includes both Roderick’s CPP and employer pension), but is unsure whether she should take it all at once or stick with one of several monthly payment choices. “I don’t fully understand all my pension options,” says Marina. “Some friends have suggested I take the $550,000 lump-sum payment so I can leave an estate to my kids. I don’t want to give so much away that I’ll have to pinch pennies in old age. But is taking the lump sum a better risk than leaving it in an underfunded pension plan?” she asks. “And when should I take my own CPP pension? If I have enough money to live on should I delay taking it for as long as possible?”

As of January, Marina’s annual income adds up to $80,677, which includes her salary as well as the spousal benefit from her husband’s employer pension and his CPP, plus rental income from the Victoria duplex. But if she quits her job, her income will decrease to about $35,000. “Can my investments and my own CPP and OAS provide me with $50,000 net annually for life?” wonders Marina. “I just don’t know.”

Working in her favour is the fact Marina has always been good at managing her money. Her parents were children of the Depression so they were very cautious financially. “They could make something out of nothing and often did,” says Marina. Later, her father (a carpenter) took an interest in investing and Marina took notice of his passion for it. “My dad loved RRSPs and was an early investor in them. He thought they were a ‘heck of a good deal,’” she says.

So over the years as Marina and Roderick paid off the mortgage on their home, they also contributed to RRSPs, which she invested in stocks and GIC rates. Then, in 2011, fearing the market was getting pricey, she sold 70% of the equities in their accounts. She’s now trying to decide on a future investment strategy, both for the RRSP as well as the life insurance money she will soon receive. “I’m educating myself on the couch potato strategy and have always invested on my own,” says Marina. “I want my portfolio to take me through the ups and down of the market. I’ve never found a financial planner I trusted but I may soon have to.”

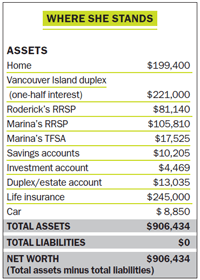

As it stands, Marina’s investment portfolio includes her Alberta home (worth $199,400), half of the duplex on Vancouver Island (her share is valued at $221,000), $186,950 in RRSPs, the $245,000 life insurance payout, $17,525 in TFSAs and $27,709 in other accounts. That makes $906,434 in total assets (including the value of her car), with no outstanding debt.

Another priority is to reduce some of her expenses—Marina pays $1,598 annually in term life insurance that may no longer be necessary. Over the years, she also completed several university courses, but is still a few credits short of a degree. “Someday, I’d love to finish—maybe when I retire,” she says. But more than anything, Marina wants a future filled with adventure and travel as well as more time visiting her two children and two grandchildren. She’d like to take a cruise to London, then travel through Europe by train.

One thing is certain—Marina can hardly wait to start her new life. “Up until six weeks ago, I threw myself into my work to try and dull the pain of watching my husband struggle. And then it was all over. One minute he was there and the next minute he was gone. It was so peaceful and so shattering,” she says. “My dreams have been on hold for so long. I don’t want to miss this chance. I am truly open to all options. I just need a good financial plan to start living my life to the fullest.”

For the first time in a long while, Marina Wilkinson will have time to focus on getting a financial road map that will make her own life goals the top priority. “Marina needs to get past the emotional part of establishing that she is financially independent and start focusing on what her goals are, because she has more than enough money to live a long and healthy life,” says Tom Feigs, a financial planner with Money Coaches Canada in Calgary. Heather Franklin, a fee-for-service planner in Toronto, agrees, adding, “the key will be to separate her decisions into smaller digestible bits and not to feel pressured to decide everything all at once. That will be a big challenge for her.” Here’s what Marina should do.

Choose the right pension option. When evaluating employer pension options, clients often see the hundreds of thousands in cash value for the first time. “Their first reaction is always, ‘Sure would be nice to drop this $550,000 in my back pocket,’” says Feigs. “But almost always, it’s the absolute wrong decision.” Why? Because according to Feigs, a guaranteed single-life pension like the one Marina is entitled to provides peace of mind and security for life. “Marina’s pension also has an annual cost-of-living adjustment of 60% of the Consumer Price Index—an important feature,” says Feigs. His advice? “Choose the guaranteed single-life option. If you wish, you could add the five-year minimum payout guarantee at a cost of $7 a month.”

Heather Franklin agrees, pointing out that there are pros and cons to both options. “Marina could do just as well by taking the $550,000 lump-sum payment and, with the help of a good fee-for-service planner, investing it in a well-diversified portfolio of dividend-paying stocks: 70% in Canadian stocks, 20% in U.S. growth stocks and 10% in a bond ETF.”

Franklin likes the flexibility it would give Marina to draw the money down on her own terms and she’d get good income plus growth. Such a portfolio would return about $19,000 a year, a little less than the single-life pension option but alternatively, her stocks would give her years worth of growth as well as the annual dividend income which should increase over the years. The key? “Marina has to absolutely be comfortable managing her own money,” says Franklin. “If she has any doubts whatsoever, she should take the monthly single-life pension option.”

Fine-tune her finances. Both Franklin and Feigs recommend that Marina should stop making RRSP contributions and top up her TFSA instead. She should also stop paying the $1,598 annually for life insurance. “She doesn’t need that anymore,” says Feigs.

Sell the house. Both experts think Marina can sell her home at any time. “Just don’t spend too much on renovations,” says Franklin. “Do the basics and then sell it.” Feigs agrees, noting that moving to the West Coast duplex is the right choice for Marina. “She should get her duplex apartment renovated this year and move in when it’s ready,” says Feigs. “The smaller duplex apartment will keep her expenses low, be in a temperate climate that she loves and put her near family and friends. That will be wonderful for the quality of her retirement life.”

Get an investment plan. Right now, Marina has almost $500,000 sitting in cash in RRSPs, TFSAs and other investments. Selling her home will add another $150,000. “She needs to invest all this money in a dividend-paying stock portfolio, similar to the way I suggested for her lump-sum payment for the employer pension,” says Franklin. Feigs agrees the RRSP money and life insurance payment should be invested conservatively, possibly in a couch potato portfolio returning about 4% net annually. “She should work with a fee-for-service financial planner to clarify her financial road map, all the while keeping her fees low. Her husband’s pension, CPP and her own CPP and OAS will provide her with close to $50,000 annually. She can dip into her portfolio for a few thousand dollars extra every year if she feels she needs it.” Marina should go to www.moneysense.ca/planners to find a planner in her area.

Start collecting CPP at age 60. At 60, Marina will be eligible to collect roughly $10,000 in annual CPP payments. At 65, she can collect about $6,500 in OAS annually. Marina should also update her will. And finally, “she may want to continue her studies and earn her university degree,” Feigs concludes. “It will keep her brain active and give her a sense of accomplishment. That’s a great thing to have in retirement.”

Julie Cazzin is an award-winning business journalist and personal finance writer based in Toronto. To be considered for Family Profile, tell Julie about your situation at [email protected]

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Tech industry warns that the budget's capital gains proposals could cause “irreparable harm.”

Learn how the federal government’s 2024 budget can affect you and your money.

Gen Z isn’t immune to phishing scams. Find out the most common schemes targeting young Canadians and how to...

Cards that waive or refund the fee for foreign currency charges are few and far between—but if you’re a...

The data behind the top places to buy real estate in Canada.