How not to sweat rising interest rates

Mutual fund and ETF makers have created floating-rate bond funds that aim to cut the risk of rising interest rates.

Mutual fund and ETF makers have created floating-rate bond funds that aim to cut the risk of rising interest rates.

Herd mentality is a strong instinct. Why carve out a new path when it’s easier to follow someone else’s? The consensus is interest rates are headed higher this year and bond prices lower. Bond investors might rightly sell to avoid loss and buy back at a later date.

It’s hard to get the timing right. After the financial crisis, five-year Canada bond yields fell to 1.69% (December 2008, source: Bank of Canada). No surprise there, since the world was in a shambles and interest rates were lowered to save it. Rates recovered but over 2012 and sporadically through most of 2013, yields never surpassed that crisis level. Hands up if you called that one! While the forecast for 2014 is interest rates will move higher, when and how quickly is tough to call.

Interest rates have come off those lows, still below historic averages but an improvement. Indeed, when stocks ended their run in January there was some bond buying. Equity investors looking to lock in gains sold, moving cash to bonds at relatively attractive rates. Short-term and short-duration bonds were typically used to preserve capital. But they also looked to floating-rate bonds.

Floating-rate bonds or notes are unlike plain-vanilla debt instruments paying fixed coupons (the annual or semi-annual interest payments.) The coupon is variable and resets periodically; daily, weekly, monthly, quarterly or annually depending on issuer. Coupon rate is set relative to specified benchmarks like the U.S. federal funds rate, LIBOR (London Interbank Offer Rate: the rate that banks borrow from each other in London) or CDOR (Canadian Dealer Offered Rate). Issuers may reset coupons at CDOR plus 0.5% every six months.

Issuers of floaters include corporations, municipalities and governments. Given concerns about credit quality and the need to preserve capital we’re seeing unusual demand for government securities; a recent issue of U.S. government floating-rate debt attracted almost six times the offered amount.

The market is large and growing, with an estimated $300 billion in outstanding issues. Banks and financial institutions dominate corporate offerings, partly because of demand for variable-rate borrowing. With variable mortgages, banks match debt obligations to variable revenue streams. Canada is active, as are U.S.-backed agencies Fannie Mae and Freddie Mac. The U.K. and Italy have long issued floating-rate debt.

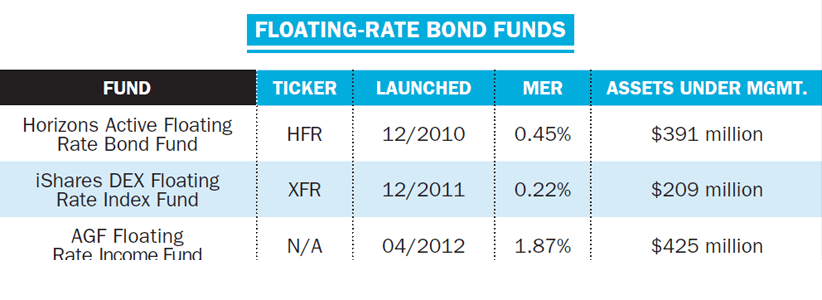

Investors can buy individual floaters through brokers but I prefer mutual funds or exchange-traded funds. Horizons won best Fixed Income ETF at the 2013 Morningstar Canadian Investment Awards. Its Active Floating Rate Bond Fund offers a portfolio of Canadian debt securities, with swap agreements to hedge rate risk. Duration is under two years. It uses active portfolio management by bond giant Fiera Capital.

iShares’ DEX Floating Rate Note Index Fund replicates an associated index three quarters in government bonds. It tracks issues as long as five years but average maturity is half that. A more passive investing style lowers costs and is best suited to investors worried about credit risk.

AGF’s Floating Rate Income Fund offers global diversification in a portfolio of U.S. senior secured bank loans. Subadvisor Eaton Vance Management, a pioneer in floaters, says floating-rate loans behave differently from, and have a low correlation to, traditional bonds. Thanks to variable coupons, yields are less volatile. Loans are reset every 30 to 90 days, so duration is near zero. Last, floating-rate loans are often most senior in corporate capital structures: important because floating-rate loans are often extended to companies with below investment-grade credit ratings. That makes these products competitive with its yields. Adding floaters to portfolios accomplishes several things. It maintains a presence for fixed income in a portfolio—a parking spot—while offering low correlation to traditional fixed-income assets. It defends against rising interest rates and their possible detrimental effect on the fixed-income component of a portfolio. And it provides a competitive income stream that can adjust to rising interest rates.

The lemmings in the crowd may be headed for an interest rate cliff. Smart investors have started beating a path to floating-rate securities. The visionary investors, those guys with their hands still up….can put them down.

Pat Bolland is a veteran financial broadcaster currently with Sun News Network. His Twitter feed is @patbolland.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

The first home savings account was created to help you save more money for a home purchase. Here’s how...

Presented By

National Bank of Canada

Find out what non-registered accounts are, how they compare to registered accounts and which investments are best for non-registered...

MoneySense was born 25 years ago. This list of 25 financial innovations shows how much personal finance has changed...

Sponsored By

Embark Student Corp.

How can you choose the best ETFs for you? Watch this video before you use an ETF screener.

Find out which Canadian robo-advisor tops our 2024 list, and which robo is right for you and your investing...

Is it easy to buy and sell stocks and ETFs? Is it safe for Canadian investors? Find out the...

GICs were embraced by many Canadian investors last year, whether conservative or not. With rates expected to fall again...