Don’t be fooled by this interest rate mistake

A one percentage point move is not the same as a 1% move

A one percentage point move is not the same as a 1% move

I grew up enjoying Weird Al Yankovic’s unique twist on popular songs. His parodies struck a chord with me and “White & Nerdy” neatly sums up many of my teenage years.

More recently, Weird Al brought joy to the hearts of editors and English teachers alike when he released “Word Crimes.” The clever song mocked those of us with, shall we say, a less than ideal handle on the language. (I plead guilty as charged.)

The language of mathematics is also the subject of a great deal of abuse. One error that really sticks in my craw surfaces in the financial world where it can lead to a great deal of confusion. I recently spotted it when perusing the risk section of a Canadian bank’s annual report. (To avoid embarrassment, the culprit will remain nameless.)

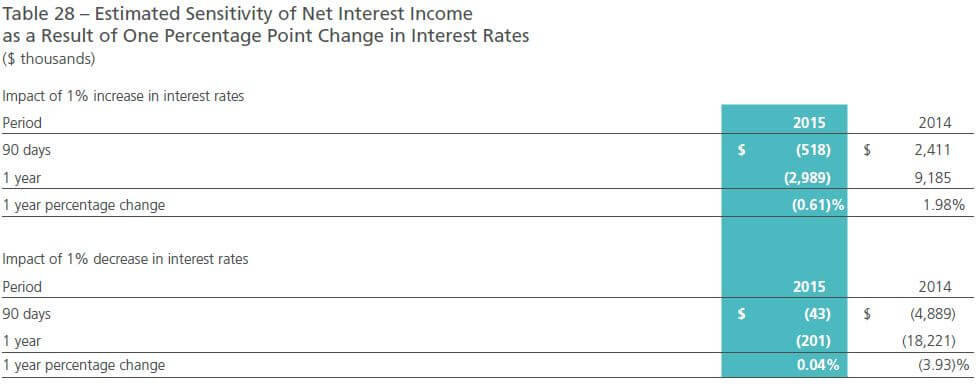

The offending table from the annual report is displayed below. Can you spot the problem?

The table shows what the bank’s risk managers think will happen to its net interest income in the event that interest rates climb, or fall, by one percentage point. The same move is also described as a 1% increase, or decrease, in interest rates. Problem is, in almost all cases, a one percentage point move is not the same as a 1% move.

Let’s say interest rates start at 2%. A one percentage point increase would push them up to 3%. Alternately, one can say that interest rates have increased by 50% when they climb from 2% to 3%.

When you boost a 2.00% rate by 1.00% you get 2.02% because 1.00% of 2.00% is 0.02%. (I’ll discuss significant figures another day.)

That said, there is a special case when a one percentage point increase is equivalent to a 1% increase. It occurs when interest rates start at 100%. In this case, both accurately describe an interest rate climb from 100% to 101%.

To be fair to the bank in question, it is reasonably clear that the table shows what they expect will happen under a one percentage point move rather than a 1% move. Nonetheless, it is something worth clearing up in next year’s report.

I hasten to add that basis points are also widely used when talking about interest rate changes. One basis point is equal to one hundredth of a percentage point. For instance, when a 4.00% interest rate climbs by 10 basis points it moves from 4.00% to 4.10%.

When describing differences in percentages (interest rates, growth rates, returns, etc.) you’ll do your readers a kindness by using percentage points or basis points.

Investors following the Dogs of the Dow strategy want to buy the 10 highest yielding stocks in the Dow Jones Industrial Average (DJIA), hold them for a year, and then move into the new list of top yielders.

The Dogs of the TSX works the same way but swaps the DJIA for the S&P/TSX 60, which contains 60 of the largest stocks in Canada.

My safer variant of the Dogs of the TSX tracks the 10 stocks in the index with the highest dividend yields provided they also pass a series of safety tests, such as having positive earnings. The idea is to weed out companies that might cut their dividends in the near term. Just be warned, it’s a task that’s easier said than done.

Here’s the updated Safer Dogs of the TSX, representing the top yielders as of July 18. The list is a good starting point for those who want to put some money to work this week. Just keep in mind, the idea is to hold the stocks for at least a year after purchase – barring some calamity.

| Name | Price | P/B | P/E | Earnings Yield | Dividend Yield |

|---|---|---|---|---|---|

| CIBC (CM) | $98.47 | 1.89 | 10.77 | 9.28% | 4.92% |

| National Bank (NA) | $45.03 | 1.62 | 13.05 | 7.66% | 4.89% |

| Power (POW) | $28.30 | 1.06 | 8.88 | 11.26% | 4.73% |

| Shaw (SJR.B) | $25.25 | 2.05 | 9.15 | 10.93% | 4.69% |

| Bank of Nova Scotia (BNS) | $65.45 | 1.61 | 11.69 | 8.56% | 4.40% |

| BCE (BCE) | $62.35 | 4.33 | 19.67 | 5.08% | 4.38% |

| TELUS (T) | $42.96 | 3.33 | 19.09 | 5.24% | 4.28% |

| Bank of Montreal (BMO) | $84.84 | 1.53 | 12.68 | 7.89% | 4.05% |

| Royal Bank (RY) | $80.01 | 1.96 | 12.01 | 8.32% | 4.05% |

| TD Bank (TD) | $56.57 | 1.67 | 12.86 | 7.78% | 3.89% |

Source: Bloomberg, July 18, 2016

Notes

Price: Closing price per share

P/B: Price to Book Value Ratio

P/E: Price to Earnings Ratio

Earnings Yield: Earnings divided by Price, expressed as a percentage

Dividend Yield: Expected-Annual-Dividend divided by Price, expressed as a percentage

As always, do your due diligence before buying any stock, including those featured here. Make sure its situation hasn’t changed in some important way, read the latest press releases and regulatory filings and take special care with stocks that trade infrequently. Remember, stocks can be risky. So, be careful out there. (Norm may own shares of some, or all, of the stocks mentioned here.)

Why Land and Homes Tend to Be Disappointing Investments

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Food and beverage company expects organic growth of 4% in 2024

General Motors reports strong first-quarter profits as prices help offset small U.S. sales dip.

New analysis from the National Institute on Ageing makes a strong case for delaying Canada Pension Plan payments to...

A pattern in the markets works—until it doesn’t. Investors will be better off focusing on the fundamentals.

Bitcoin’s next “halving” is right around the corner. Here’s what you need to know.

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Earth Day is on April 22. Here’s how to invest sustainably, and other ways to help the planet.

Understanding industry jargon can make you a better real estate investor.

Capital gains tax inclusion rate will increase (for some), Netflix chills, U.S. bank earnings solid, and will the loonie...

Tech industry warns that the budget's capital gains proposals could cause “irreparable harm.”