A growth portfolio for the long term

If you have a pension, you probably don't need the fixed income exposure that comes with balanced fund

If you have a pension, you probably don't need the fixed income exposure that comes with balanced fund

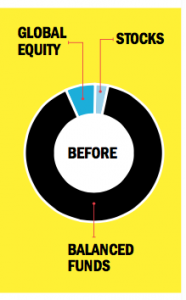

Srinivas Velanki, a 52-year-old engineer from Edmonton, has a defined-benefit pension plan and real estate properties. Right now his low six-figure retirement portfolio is  invested mostly in an RRSP of 90% balanced mutual funds, 7% global equity funds and the remaining 3% spread among three stocks: Corus Entertainment, Canadian National Railway and Canadian Pacific Railways. Now he wants to switch to a high-growth stock portfolio (no dividends required) and exchange-traded funds. “I want the money to travel in retirement, so I’m aiming big. I’d like an average annual return of 10% over the next 20 years.”

invested mostly in an RRSP of 90% balanced mutual funds, 7% global equity funds and the remaining 3% spread among three stocks: Corus Entertainment, Canadian National Railway and Canadian Pacific Railways. Now he wants to switch to a high-growth stock portfolio (no dividends required) and exchange-traded funds. “I want the money to travel in retirement, so I’m aiming big. I’d like an average annual return of 10% over the next 20 years.”

Minimizing exposure to fixed income by reducing exposure to balanced funds is a good move mainly because Velanki’s core retirement needs will be taken care of with his pension and other savings. “Investors who rely on bond products to keep them safe and provide a reasonable rate of return could be very disappointed for many years,” explains Miles Clyne, a portfolio manager with the Tycuda Group at MacDougall Investment Counsel Inc. in Langley, B.C. Current low interest rates and the impact of rising rates in the future, are “foretelling a not-so-pretty picture.”

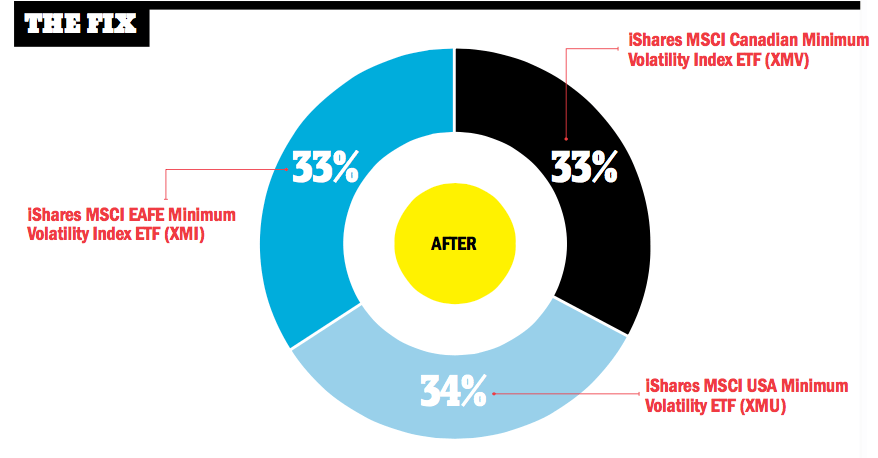

If Velanki is looking for a buy-and-hold strategy with minimal trading, Clyne recommends low-volatility ETFs. These use a number of strategies to maximize returns, including shorting the market index, which allows the investor to profit from falling stock markets. Clyne recommends Velanki keep it simple and build a portfolio that holds equal weightings in just three low-volatility ETFs: iShares MSCI EAFE Minimum Volatility Index ETF (XMI), iShares MSCI Canadian Minimum Volatility Index ETF (XMV) and iShares MSCI USA Minimum Volatility ETF (XMU). “Getting a 10% return over a market cycle should be doable with this portfolio,” says Clyne.

Still, if Velanki is a bit more conservative, Clyne suggests low-risk investments with any additional contributions. A short-term laddered corporate bond ETF, such as the iShares 1–5 Year Laddered Corporate Bond ETF (CBO), would be appropriate and he could use the gains to rebalance his portfolio.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Presented By

Embark Student Corp.

Breaking your mortgage to get a better interest rate could save you thousands of dollars. Here’s what you should...

Has your home insurance premium gone up? We get to the bottom of why rates are on the rise...

You've poured lots of money into your RRSP. How do you get it out without paying a fortune in...

Thinking about a career change or worried you won’t escape the next round of layoffs? Follow our tips to...

You can do more than survive in Canada—choose where to put your wisely and over the long term you'll...