Perfect advisor for your financial planning needs

There are three main types of advisors—here's what you need to know to pick the right one

There are three main types of advisors—here's what you need to know to pick the right one

The word “frustrating” best describes Todd Wilson’s recent experience seeking information about mutual fund investments at his bank’s local branch. Even after talking with four different staffers, he still hadn’t received the help he needed. The problem? “There was no advice,” says the Edmonton-based engineer (whose name we’ve changed to protect his privacy). Wilson was hoping to get knowledgeable second opinions on his mutual fund preferences and to hear the relative merits of investing in TFSAs vs RRSPs. But instead, he says, “their attitude was, ‘If you want to invest, let me know and I’ll do the transaction for you.’”

Wilson’s discontentment is well justified. Simply put, there’s a lot more to a proper investment process than merely picking investments. Your advisor needs to first thoroughly understand your financial circumstances, and should be someone you can turn to for sound advice at all times. Your advisor should also be forthright about fees, meet with you periodically, rebalance your portfolio as required, and report in clear terms how it has performed. “This is a much more holistic process than just finding those securities that are going to produce the best return,” says Stephen Horan, managing director at the CFA Institute and co-author of The New Wealth Management.

Unless you’re a strict do-it-yourself investor, you can expect to pay a decent amount of money for investment advice. But provided you’re getting good service, that cost can be well worth it—particularly when you’re close to retirement or retired and don’t have much latitude for making mistakes. In what follows, we show what you should expect from a qualified advisor and how to make sure you get it.

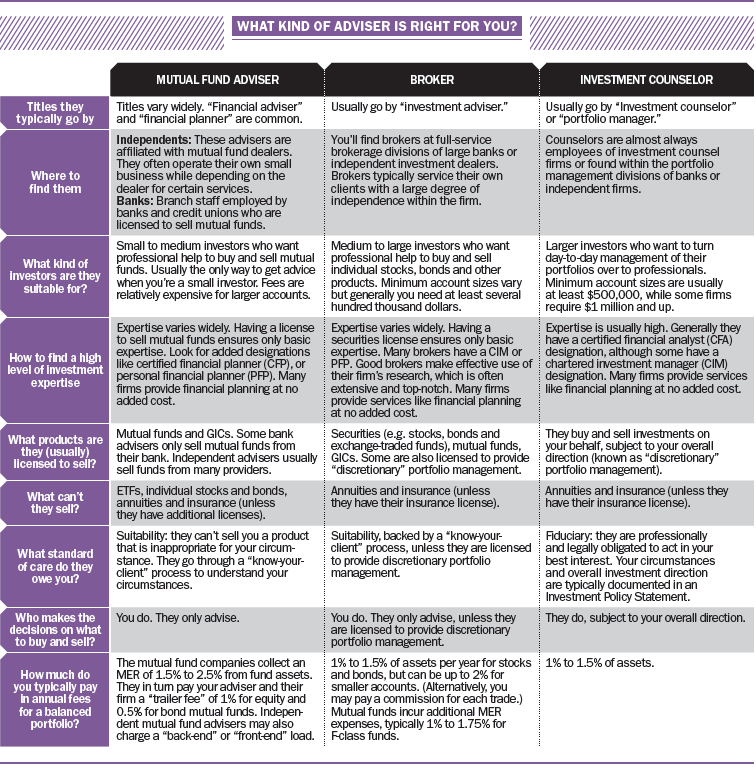

As Todd Wilson discovered, finding a well-qualified financial professional isn’t always easy. Still, there are plenty of experienced professionals out there in different types of financial institutions who can provide high quality assistance. (See “What kind of advisor is right for you?” above.) Often the challenge is knowing what to look for and then figuring out where to find it.

The first thing to understand is that advisors need only basic investment knowledge to be licensed to sell mutual funds or securities. This means advisor expertise varies widely. If you’re beginning a search, a good starting point is to ask for referrals from people you trust, particularly if they have strong investment knowledge.

Another approach is to delve into an advisor’s experience and credentials. For in-depth knowledge of investments and constructing a portfolio, the chartered financial analyst (CFA) designation is particularly respected, although the chartered investment manager (CIM) designation is also well-regarded. (Disclosure: I have a CFA designation.) If you want good investment knowledge and broader financial planning expertise, the certified financial planner (CFP) designation is reputable. The personal financial planner (PFP) designation, often found among bankers and brokers, is not as strong, but it is also respected. Many bank branches have financial planners on staff, so if you’re looking for knowledgeable advice in a bank branch, ask for an accredited financial planner.

Many advisors use the preparation of a full financial plan as a starting point for investing. Sometimes they will prepare a plan themselves. In other cases, they’ll get a specialist on staff to do it. Often it won’t cost you anything extra beyond regular investment fees. But even if you’re not interested in a full-blown financial plan, having an adviser with a financial planning background can still prove useful. For example, any financial planner worth his or her salt should be able to provide a good answer to Wilson’s question about the relative merits of investing in a TFSA or RRSP. “As a financial planner, it’s going to be much easier to demonstrate value added,” says Cary List, president of the Financial Planning Standards Council.

The investment process itself should start with your advisor getting an in-depth understanding of your needs and situation. This should include your main real-world financial objectives, such as saving for retirement or for your child’s education, while taking into consideration your investment knowledge level and risk tolerance. An adviser must also determine your short-term and intermediate withdrawal needs, as well as the time horizon for drawing down your portfolio in retirement. Your current—and likely future—tax situation is key too.

Although regulators require advisors to ask and document this kind of information, your adviser needs to do more than go through the motions. “Has he taken the time to really understand the client or did he just tick off a bunch of boxes and start recommending things?” is how Eric Kirzner, professor of finance at the University of Toronto’s Rotman School of Management, puts it. While investment knowledge is important, he says, so is personal rapport and trust. “You’ve got to convince yourself that you have someone that really has your interests at heart.”

Your advisor then has to structure your portfolio. A key driver for getting it right is setting an appropriate overall asset allocation that fits your personal circumstances—particularly, in getting the right mix between fixed income and equity, but also in specifying the types of equities and fixed income. Special care needs to be taken if you’re retired or close to it. That’s because in the event of a market meltdown, retirees can be vulnerable to the risk of having to sell investments at beaten down prices in order to provide funds to live on, which is known as “sequence of returns risk.” That can potentially devastate a portfolio so much it can’t recover. As a result, it’s a good idea to structure your portfolio so it can meet your cash flow requirements for the first five to 10 years of retirement without having to sell investments at possibly distressed prices.

Advisors can also help you keep a level head. Many studies have shown investors are prone to letting their emotions get the better of their investment decisions, causing them to load up on stocks in bull markets, then to become fearful and sell in bear markets—which are precisely the wrong things to do. “A good adviser has the ability to calm things down, provide a stabilizing influence and take a dispassionate view of the market,” says Richard Deaves, co-author of Behavioral Finance: Psychology, Decision-making and Markets and professor of finance at McMaster University’s DeGroote School of Business.

Your advisor should meet with you regularly—at least once a year—to review your portfolio. Adjustments may be necessary due to changing personal circumstances, or the need to rebalance if your holdings diverge substantially from target allocations. Your adviser should also show you the percentage return for your portfolio as a whole and for major asset categories. Ideally these should be compared to benchmarks, where appropriate.

Unfortunately, many investors are left in the dark as to how their portfolio is really doing because their advisors don’t report this critical information. But if your adviser doesn’t provide it routinely like they should, often you can get it by just asking. Soon, however, it will be mandatory. Starting in mid-2016, Canadian securities regulators will require investment firms to provide annual performance reports that show the percentage returns of your investments.

It’s up to you to make sure your advisor is knowledgeable, understands your situation thoroughly, follows a proper investment process, is forthright about fees, communicates regularly and reports on your returns. An advisor’s services can be expensive, but you can get enormous value with the right advice.

A good advisor should help you understand clearly the fees you pay for advice. But whenit comes to mutual fund fees, manyinvestors are left confused. For instance, a 2013 Investment Funds Institute of Canada survey found that only 48% of mutual fund investors were very confident or confident in their knowledge of any fees they pay with their mutual funds. To help clarify this, here’s the basics on how mutual fund advisors are compensated.

Trailing Commission

This is a fee buried in the Management Expense Ratio (MER) that provides the predominant source of compensation to advisors and the companies they’re affiliated with. It typically amounts to 1% per year for equity funds and 0.5% for bond funds, and continues as long as you hold the funds. If your advisor charges you a fee based on a percentage of your assets (common among brokers but rare among mutual fund advisors), then they should sell you “F-series” mutual funds with lower MERs that don’t include trailing commissions. If you’re a do-it-yourself investor buying mutual funds in a discount brokerage, you should buy “D-series” mutual funds with reduced trailing commissions, or mutual funds offered by providers that don’t include trailer fees at all (such as Leith Wheeler, Mawer and Steadyhand).

Deferred Sales Charge

Also known as a “back-end load,” this is a one-time charge (typically up to 6%) that you pay the mutual fund provider if you sell a fund set up this way within a set holding period, usually five to seven years. Typically, the amount of the potential charge gradually diminishes over the lock-in period. In my view, this charge is onerous.

Front-End Sales Charge

Also known as a “front-end load,” this is a one-time charge (typically up to 5%) that the advisor charges you directly up front for buying a mutual fund. This isn’t a competitive practice these days and is rarely levied. However, in many situations advisors can charge this fee if they choose (and you agree), even though the advisor is also getting a trailer fee. My advice is don’t agree to it.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Learn how the federal government’s 2024 budget can affect you and your money.

U.S. inflation comes in hot, Delta says revenge travel is alive and well, doubling your CPP benefits, and AI...

History repeats (or rhymes) itself in latest market upswing, FHSA celebrates its first birthday, investors getting rich from stocks,...

When you die, capital gains tax might apply to some of your assets. Can life insurance help shelter your...

Here’s how to get your free ticket to attend the MoneyShow Canada Virtual Expo.

Trump sells unprofitable company for billions, the U.S. is an oil king, GameStop struggles continue, and tech rules the...

Financial experts debunk old money myths and offer advice that many Canadians might find more helpful today.

Inflation falls, Fedex jumps 13%, earnings soften for Power Corp and Couche-Tard, and S&P 500 gets two new members.

You don’t want to miss the conversion deadline at the end of the year you turn 71—you’ll be on...

Presented By

National Bank of Canada