Why the 4% withdrawal rule may not be safe

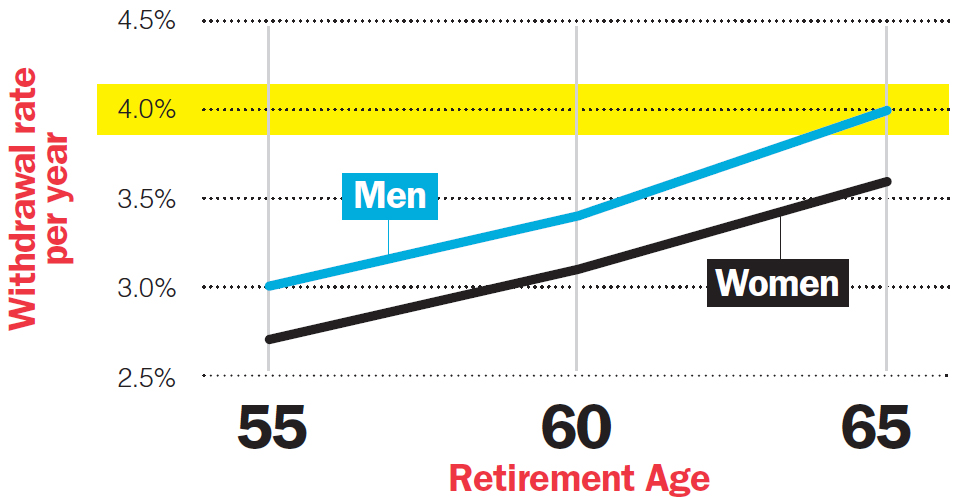

Women should instead budget for 3.6% or less for retirement withdrawals

Women should instead budget for 3.6% or less for retirement withdrawals

Retirement expert Moshe Milevsky hates the 4% rule. The decades-old maxim states that you can withdraw 4% of your nest egg each year after you retire and you’ll never run out of money. But Milevsky says for most individuals, it’s just not true. Sure, if you’re male, you retire right at 65 and you’re completely average, then it applies, he says. “But what’s average?” The rule doesn’t apply to women at all, he notes, because they live longer, so they’re more likely to run out. As the chart below shows, “average” women should instead budget for 3.6% or less to be safe.

Assumptions: Initial withdrawals are increased annually for inflation. Portfolio is invested 50% in stocks and 50% in bonds, and the inflation rate is 2%. Source: M. Milevsky and F. Habib, CANNEX

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

New analysis from the National Institute on Ageing makes a strong case for delaying Canada Pension Plan payments to...

You can still benefit from deferring Canada Pension Plan payments with less than maximum contributions.

Two siblings’ complex inheritance provides a case study in minimizing death taxes.

Capital gains tax inclusion rate will increase (for some), Netflix chills, U.S. bank earnings solid, and will the loonie...

Learn how the federal government’s 2024 budget can affect you and your money.

U.S. inflation comes in hot, Delta says revenge travel is alive and well, doubling your CPP benefits, and AI...

History repeats (or rhymes) itself in latest market upswing, FHSA celebrates its first birthday, investors getting rich from stocks,...

When you die, capital gains tax might apply to some of your assets. Can life insurance help shelter your...

Here’s how to get your free ticket to attend the MoneyShow Canada Virtual Expo.