5 rules to pay less tax

Don't sweat the fine print and keep more of your money

Don't sweat the fine print and keep more of your money

Do you plan to be wealthy? Then it’s time to go to tax school. As your kids head back to the classroom to learn to read and write, you can learn basic taxation principles that will help you build wealth faster.

There’s a reason why those who have more, care more about taxes. They know that what’s truly important is your “real net worth”—the net value of assets after taxes, inflation and accumulation costs such as interest on debt and professional fees. It’s all about what you keep and what it’s worth when you need it. Learn these five important tax principles, and you’ll have a more enlightened view of what wealth is, and how to build it faster.

1. Understand what income is. Make it your business to understand tax jargon. Start by learning the definitions of income: total income, net income, taxable income, earned income for RRSP purposes—they all have different meanings. The most important of these is “net income,” because that’s the figure used in many federal and provincial tax credit calculations. When you know how to reduce your effective net income through deductions like RRSP contributions or investment carrying charges, you will tap into the most government benefits and pay the least federal and provincial taxes.

2. Don’t pay before you have to. One of the best ways to turn the tables in your favour is to refuse to overpay your taxes throughout the year. Think differently about your tax refund: it’s an interest-free loan you give to government. Instead, focus on reducing it and your taxes at the same time. Consider asking CRA to permit your employer to reduce tax withheld to take your RRSP contribution into account, thereby receiving your refund every two weeks, instead of next April.

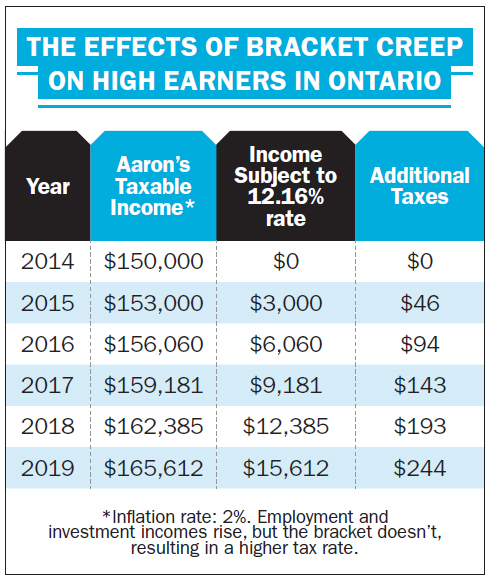

3. Offset bracket creep. If you can take control over your pre-tax earnings so you can invest more sooner, you’ll have an important hedge against inflation—a formidable foe that reduces future purchasing power. Governments can use inflation in their favour as a powerful tax collector. One way is through “bracket creep.”

The table above explains how this works against Aaron, a high income earner in Ontario. His salary is $140,000 and it’s indexed to inflation, plus he has $10,000 in investment income. The rate of tax he pays to the Ontario government on his next taxable dollar is 11.16%. Ontario recently introduced a new 12.16% rate, but right now, Aaron’s income is below the threshold. Unfortunately, not for long: as his income rises due to inflation, he will have to pay tax at a higher rate because of bracket creep.

The table above explains how this works against Aaron, a high income earner in Ontario. His salary is $140,000 and it’s indexed to inflation, plus he has $10,000 in investment income. The rate of tax he pays to the Ontario government on his next taxable dollar is 11.16%. Ontario recently introduced a new 12.16% rate, but right now, Aaron’s income is below the threshold. Unfortunately, not for long: as his income rises due to inflation, he will have to pay tax at a higher rate because of bracket creep.

Luckily there are three ways for astute savers like Aaron to fight back: With good tax planning, you can eliminate the tax on investment income using a TFSA (Tax-Free Savings Account), defer tax on employment income with an RRSP (Registered Retirement Savings Plan), and diversify and split income sources by transferring investment income to your spouse.

4. Reduce taxes as a family. Because we have a progressive tax system, the more you earn the more you pay. As well, different income sources attract different marginal tax rates. But when multiple income sources are earned by several taxpayers in the family, instead of just one, the household can successfully average taxes downward. Family income splitting is an important principle in tax-efficient wealth management—so do your tax planning as a family to fund important family milestones. An RESP (Registered Education Savings Plan) can be helpful here in transferring investment earnings to the university-bound.

5. Borrow wisely. When it comes to interest, you’ll be richer if you earn it, instead of paying it. But, if you must pay interest, make sure it’s deductible. Arrange your affairs to pay off non-deductible debt, like consumer credit cards and home mortgages. Then use your stronger cash flow position to invest in income-producing assets, like securities held in non-registered accounts, a rental property, or a business.

Remember, time is your most precious resource in beating wealth eroders like taxes, inflation, and non-deductible interest costs. Learning more about taxes will help you understand and execute your investment goals and tap into the wealth of knowledge your professional advisory team has. The best news? Those professional fees could be tax-deductible, too.

Evelyn Jacks is president of Knowledge Bureau, which offers e-learning at knowledgebureau.com. Evelyn tweets @evelynjacks and blogs at evelynjacks.com.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

New analysis from the National Institute on Ageing makes a strong case for delaying Canada Pension Plan payments to...

When is capital gains tax payable on the sale of property? And at what rate are capital gains taxed?...

Learn how capital gains are taxed and how to avoid paying more taxes than necessary when selling your assets....

Learn how the federal government’s 2024 budget can affect you and your money.

Can you still claim work-from-home expenses? What is capital gains tax and how does it work? We answer all...

Doing home renovations? Find out if there are any tax incentives that Canadians are able to claim.

Covered call ETFs aren’t for everyone. Here are some common misconceptions about this investment type, and who it’s best...

It’s challenging to balance education savings with the high cost of living. Here are six ways to invest in an...

Be prepared for the financial burdens of caring for aging parents by learning about the innovative strategies that could...

We have everything you need to know about tax credits, changes and deadlines, and more. Get the info you...

Just wanted to ask if there are any tools to use in order to not pay as much tax as I am paying right now?

I work with a company as an employee

But I pay too much tax and it’s not fare.

Due to the large volume of comments we receive, we regret that we are unable to respond directly to each one. We invite you to email your question to [email protected], where it will be considered for a future response by one of our expert columnists. For personal advice, we suggest consulting with your financial institution or a qualified advisor.