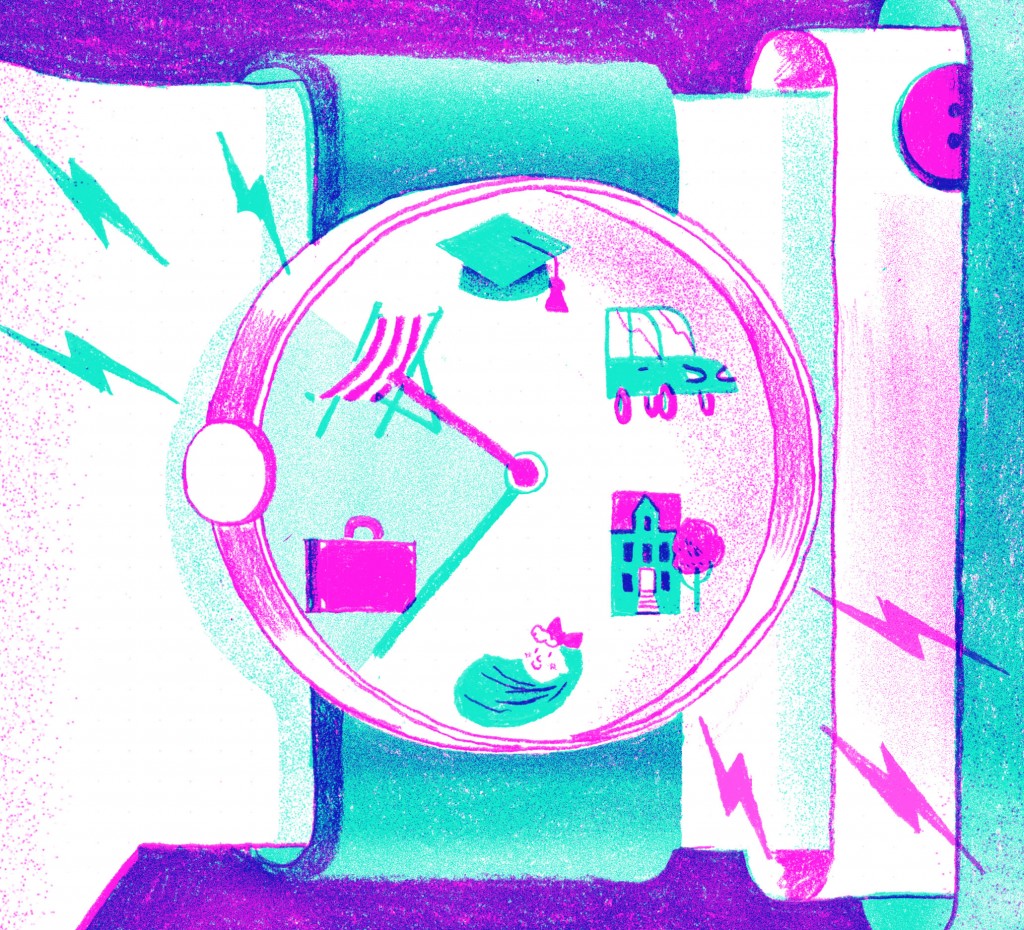

The right time to save for retirement

Your stage of life should help determine when you save

Your stage of life should help determine when you save

You’ve probably seen some of those studies hectoring Canadians about not saving enough for retirement. Often they draw that conclusion after presenting a survey, such as a recent one which found “only” 48% of Canadians are currently saving for retirement. If those kinds of studies make you feel guilty for not saving or not saving enough, you’re not alone. But are those studies telling you the right thing?

Everyone knows saving for retirement is a good thing, but like many good things, it can get pushed far beyond the point of where it makes sense. The truth is, there are many situations where saving for retirement shouldn’t be a priority. That’s especially true for people in the first half of their working lives who are struggling to buy a home or cover mortgage payments while starting a family. “In order to shame people into saving, we’ve sort of developed this national obsession with trying to make everyone feel guilty about not saving quite a bit, even at young ages when there’s no natural reason why they should be doing that,” says Malcolm Hamilton, well-known retirement expert and fellow with the C. D. Howe Institute.

Of course, when it does become the right time to save, you have to dig in and do it diligently. It’s all a question of timing. In what follows, we show how your stage of life should help determine when you should save, assuming you’re a typical middle class Canadian who expects at some point to own a home and perhaps have kids.

A lot of conventional financial advice assumes the one and only way to build financial savings is to do so at a steady clip at every point along the way, but that isn’t realistic for most people. “The conventional wisdom in Canada is first you form your retirement plan and then you try to fit your life around it,” says Hamilton. “It really should be quite the reverse. First you should figure out your life plan and then you should fit your retirement savings around it.”

As Hamilton points out, in the first half of most people’s working lives, they are just starting their careers and usually have modest incomes, but they also shoulder a disproportionate share of major life expenses such as getting an education, raising kids, and buying a home. In the second half of their working lives, most people experience the reverse: they usually achieve peak earnings while benefitting from diminishing expenses for raising children and the mortgage. There’s just a lot more natural scope to build up financial savings later.

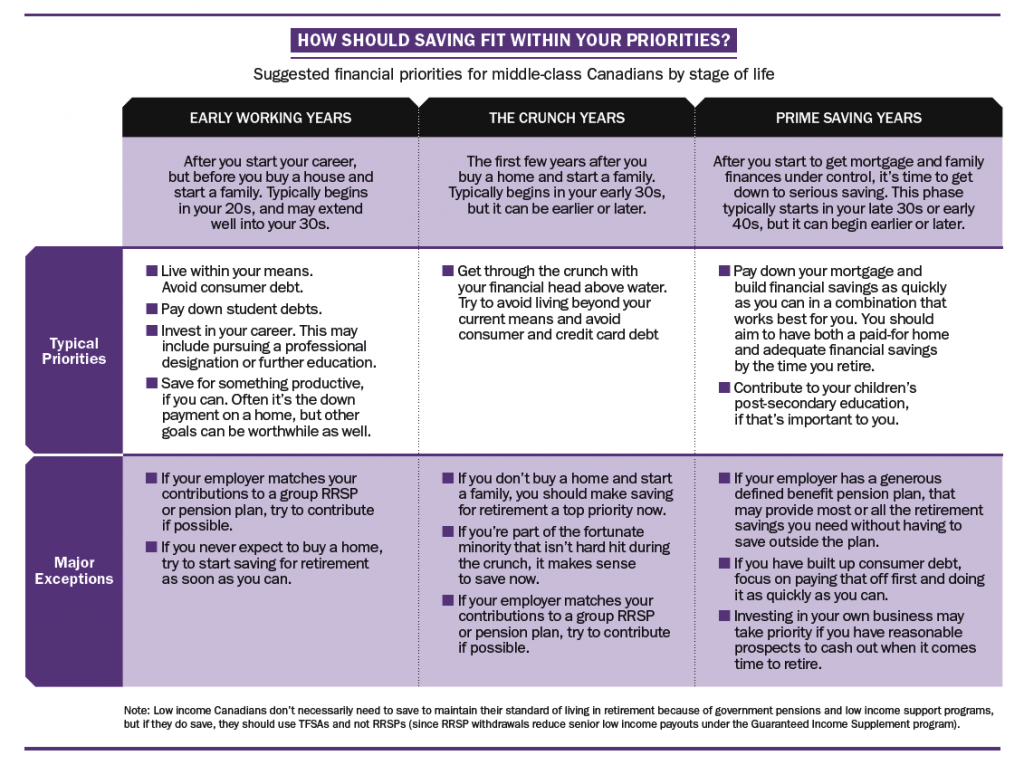

In the early working years—after you start your career but before you buy a home and start a family—it pays to get a good start financially. This stage typically happens in your 20s, and can often extend well into your 30s. At this point, you’re probably earning a modest salary, which should grow as you develop your career. The key financial priorities should be: live within your means, pay down any student debts you have as quickly as possible, avoid consumer debt and invest in your career. Oh yes, and since you probably lived frugally while you were at university or college, you will likely want to spend a bit of money enjoying life—which is okay if you don’t go overboard.

If you have money left after that, it’s certainly a wise idea to start saving. But for what? Few Canadians this age are motivated to salt away money dedicated to a retirement that might be 30 or 40 years away. The more realistic objective is to save for a productive purpose that is more immediate. In many cases, it means saving money towards the down payment on a house or condo. But it could be for going back to school or for buying a car needed for work.

Saving for any productive purpose will help make your financial situation easier down the road. Building up a down payment now can later help you buy a nicer home, or buy it sooner, or have a smaller mortgage (possibly avoiding extra fees for a high-ratio mortgage), or it just may give you more financial leeway during the crunch years to come.

Of course, the money doesn’t necessarily have to be committed in advance to one thing. How you use money saved in a TFSA is flexible, since there is no tax consequence when you take the money out.

While putting money into an RRSP is less flexible and ostensibly a commitment to saving for retirement, people can still borrow up to $25,000 each from their RRSP under the Home Buyers’ Plan when it comes time to buy a first home (although they have to pay it back under a strict schedule over 15 years or pay taxes on the money they withdrew).

» Home: Real estate investment or place place to live?

Now, consider what your priorities should be during the crunch years. This peak financial challenge usually comes in the first few years after shouldering the enormous cost of buying a family home and starting a family. It typically starts in your early 30s and lasts maybe five to eight years until your kids are in school full-time, although the precise timing, length and intensity can vary quite a bit.

During this period, it’s usually only the affluent who can afford to carry a mortgage, raise kids and save for retirement at the same time without major sacrifice. If that doesn’t describe you, consider what you’re willing to cut to make it work. “If you try to do all three at the same time, do you end up cheating yourself and your spouse, and your children? Only you can know that,” says Hamilton. “If you can’t provide your children all the educational and recreational opportunities you think they deserve, then saving for retirement isn’t a good idea. If you run up credit card debt and carry it, saving then is not a good idea.”

The main financial priority is often just keeping your head above water. That means making your regular mortgage payments and avoiding consumer or credit card debt if you can. If you manage that, you should realize you’re making progress even when it doesn’t look like it, because the principal component of your regular mortgage payment is gradually building up equity in your home. The other thing to realize is that the crunch usually ends naturally of its own accord. Mortgage payments are generally flat, but child-care costs tend to fall off when children reach school age, or income jumps when a stay-at-home spouse returns to work. Salaries usually rise over time, at least for inflation and often for promotional increases or pay increases tied to an experience-related salary grid.

Of course when you’re in the thick of the crunch years, it’s hard to see the light at the end of the tunnel. That’s why it helps to do a little planning. “If they have a clear plan and direction, they realize ‘we can catch up,’” says Sheila Walkington, financial planner and co-founder of Money Coaches Canada. “They can see as long as they stick to the plan, they’ll be okay.” But to make the plan work you have to get down to serious saving when the time is right.

As your finances improve, you reach your prime saving years. There is a time to save and it’s important you realize that time is now. You have three good options on how to do that. Which one makes the most sense depends on which best fits your preference and personality.

The mortgage first option, long advocated by Hamilton, makes a lot of sense if you hate debt and want to get the mortgage monkey off your back quickly. You pay it off as fast as you are able, and only then focus on saving for retirement (which you then do intensively in a concentrated period). Generally when you reach the switch-over point and focus on saving—ideally in your mid to late 40s but possibly in your early 50s—you’ve naturally started to think about retirement, which may help motivate you to save for it. A rapid reduction in mortgage debt also gives you greater flexibility in the event of later job loss and can help protect you if interest rates start to rise.

Another approach, favoured by Walkington, is to just continue to make regular mortgage payments and put all the extra money you can into building financial savings. You may find that putting the priority on building up financial savings in an RRSP or TFSA is more motivating than applying extra payments to building up mortgage equity because it is more visible. Meanwhile, the need to continue to make regular mortgage payments helps ensure discipline in your finances, while also gradually extinguishing the debt after perhaps 25 years.

As a third alternative, there is the classic Canadian compromise of going the savings route by contributing to an RRSP, but then applying the RRSP rebate to paying down the mortgage. That can work if you like to make progress on two fronts at the same time, points out Cynthia Holmes, a professor of real estate management at Ryerson University’s Ted Rogers School of Management. “If you contribute to RRSPs while you’re paying down the mortgage, then you can get a more diversified portfolio earlier.”

David Aston, CFA, MA, writes about personal finance. You can send him questions, comments and suggested article topics at [email protected]

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Managing lifestyle creep is challenging financially and psychologically, especially with inflation. Expert strategies keep day-to-day spending in check.

Bitcoin’s next “halving” is right around the corner. Here’s what you need to know.

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Earth Day is on April 22. Here’s how to invest sustainably, and other ways to help the planet.

MoneySense celebrates Earth Day by sharing our editors’ top tips for reducing waste, saving money and shrinking our environmental...

Understanding industry jargon can make you a better real estate investor.

Learn how capital gains are taxed and how to avoid paying more taxes than necessary when selling your assets....

Capital gains tax inclusion rate will increase (for some), Netflix chills, U.S. bank earnings solid, and will the loonie...