Why longer car loans should worry you

After 5 years, chances are you'll owe more than the car is worth

After 5 years, chances are you'll owe more than the car is worth

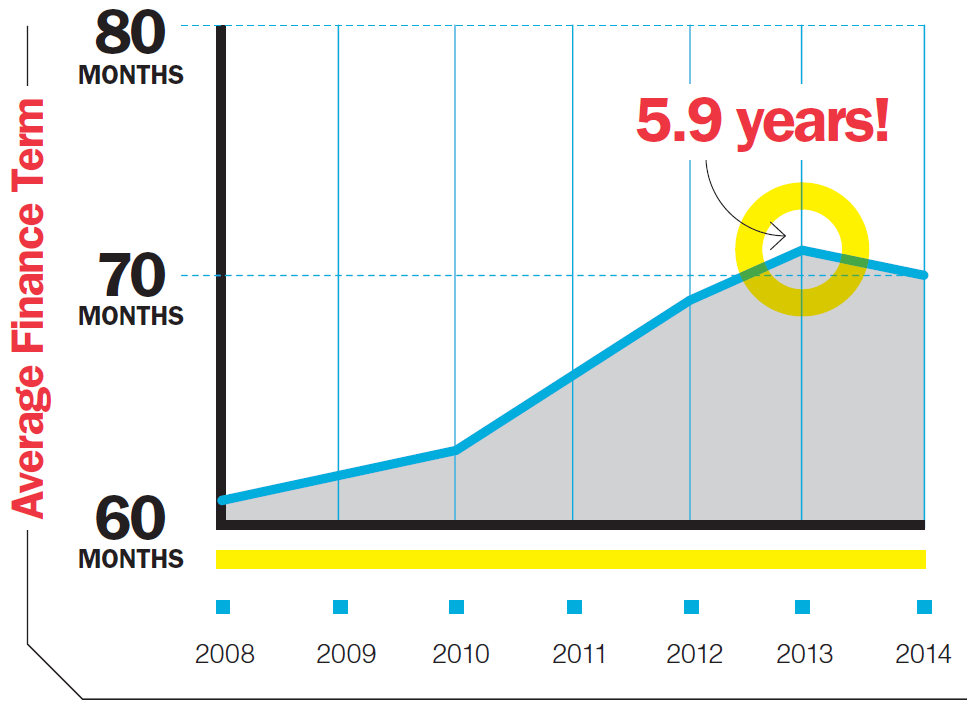

Thanks to interest rates as low as 0%, Canadians are taking on longer car loans. In fact, it’s not unheard of to see payments stretched out to 96 months or eight years, says Car Help Canada’s Mohamed Bouchama. Even though car prices are rising, “people love the low monthly payments,” he says. The problem is when you go to trade in your car after four or five years and find out you owe more in payments than what the vehicle’s worth. “That’s called negative equity,” says Bouchama.

Source: J.D. Power & Associates

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

For some repairs and maintenance, you can bring your ride to any car repair shop or mechanic in Canada....

Insurance is high on frequently stolen vehicles. Here’s how to reduce your premiums.

What a car loan can do to your credit and borrowing capacity, and how interest and add-ons really do...

What is car insurance, how much does it cost, and how can you find the best coverage for your...

The Canadian government will send out carbon pricing rebates in April 2024. See how much you can expect to...

Created By

Kruzee

If shopping is your hobby, or you want discounts on everything—from groceries to a new car—check out this list...

Roadside assistance is something you never think about—until you need it. Having one of these credit cards will ensure...

Are you a first-time car buyer in Canada? Here’s how to choose a vehicle, negotiate the price and finance...

If you’re looking for a used electric vehicle, put the Mustang Mach-E on your list. This award-winning EV offers...