How much more you need to afford a home now

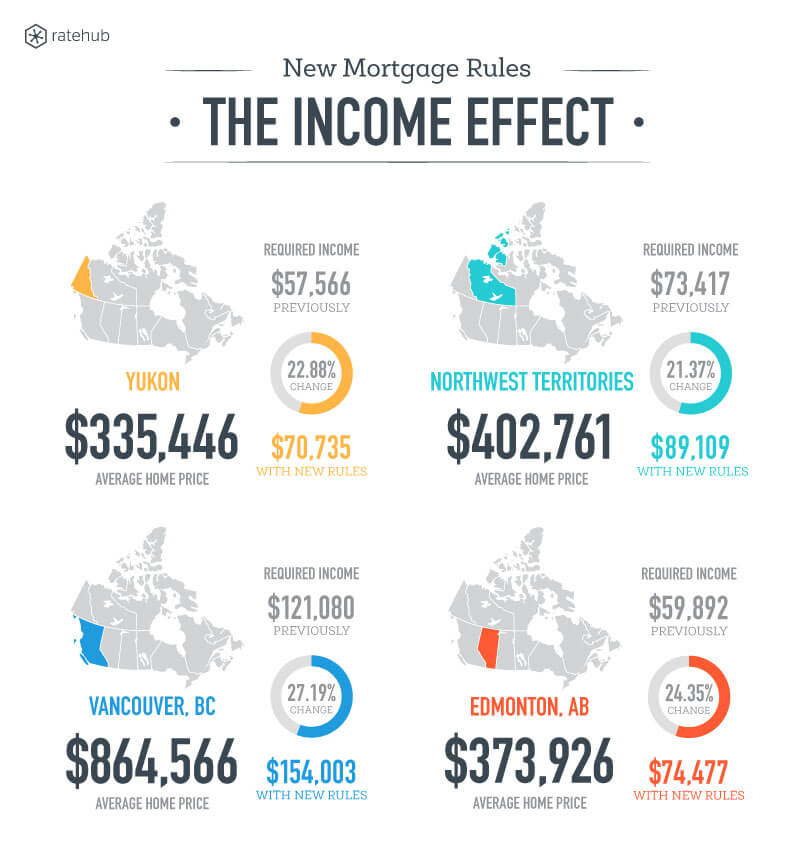

People in Vancouver need to a 27% higher income after new mortgage rules

People in Vancouver need to a 27% higher income after new mortgage rules

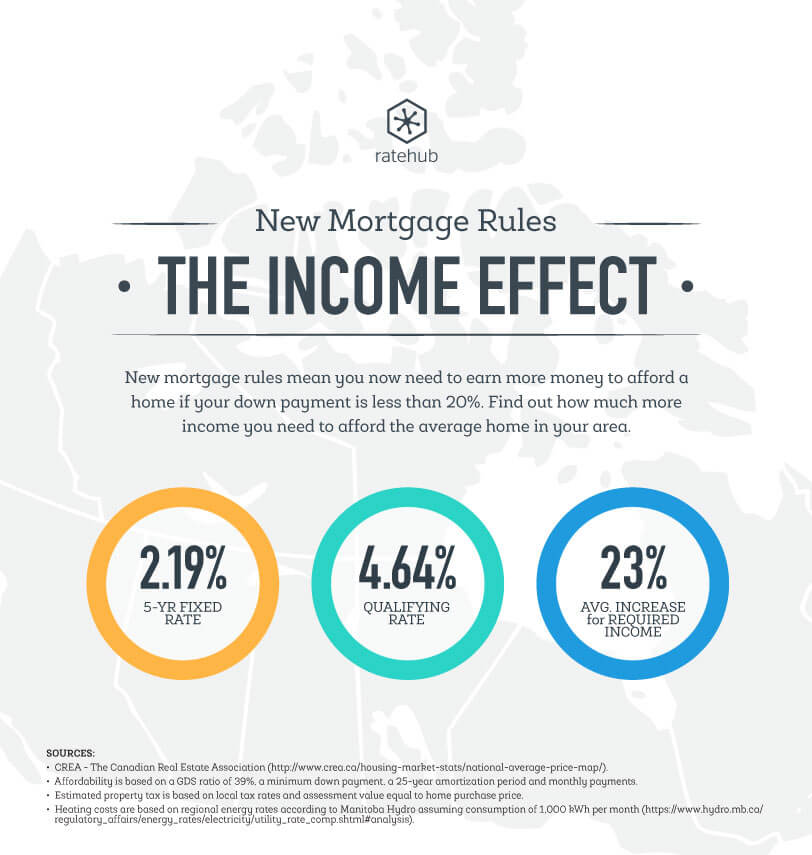

We all know that last month the federal Liberals made changes to mortgage rules across Canada, mainly requiring a stress test for borrowers of the common five-year fixed rate mortgage. Borrowers are now required to qualify for loans at the Bank of Canada’s posted rate (about two percentage points higher than current offered rates). Sure, we’ve heard the numbers, but it’s difficult for the average home buyer to fully know what all this means for purchasing power and their bottom line.

Well, now we know. Mortgage rate site Ratehub.ca has crunched the numbers for several cities across Canada and what they found was consistent throughout—it’s going to take a much larger household income to buy a home than just a year ago.

In fact, they found that to get an insured mortgage on an average-priced house, you will need at least 20% more income than you did before the rules came into place last month.

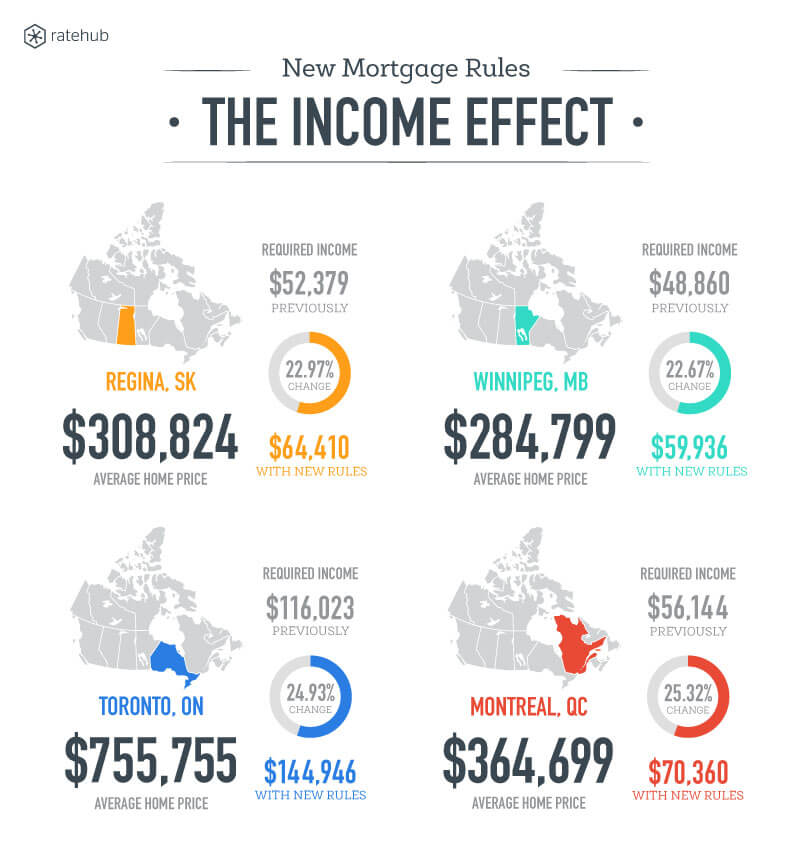

For instance, in Toronto, you’ll need nearly 25% more income (an extra $29,000 or so) than before to afford an average house. In Montreal you’ll need 25% more as well— an extra $14,216 in income. Meanwhile in Edmonton you’ll need 24% more income (an extra $14,585).

Since most of our paycheques won’t be keeping up with these price increases, what you’re likely to see is a decline in home sales and moderating or slowly declining house prices.

Check out Ratehub’s charts below showing how much more income you’ll need for an insured mortgage on an average-priced house in Canada as well as their website for up-to-date mortgage info and other resources to help you with your financial decision-making.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Equifax Canada says it’s exploring how rent data could factor into credit scores to help make credit and financial...

Extreme weather is the new norm, so it’s smart to prepare for power outages. Battery backup power could be...

When is capital gains tax payable on the sale of property? And at what rate are capital gains taxed?...

Understanding industry jargon can make you a better real estate investor.

Learn how the federal government’s 2024 budget can affect you and your money.

The data behind the top places to buy real estate in Canada.