Get in with no regrets

How first-time buyers managed to buy into this real estate market

How first-time buyers managed to buy into this real estate market

“This year. I’m buying a home.”

This was the mantra that kept Jason Arias going in the few years after the Toronto firefighter had finalized his divorce. Part of his motivation came from the fact that he was living in his parents’ basement. The bigger reason was his daughter. “I needed my own space and a place that my seven-year-old daughter could call home.” But there was a problem. A big problem. “I just couldn’t afford anything in the city,” recalls Jason. Worse still, the typical solutions such as moving further out of the city or buying a smaller place weren’t really options. “My daughter’s mom lives downtown and I didn’t want to move so far away that I couldn’t be a big part of my child’s life.” Yet, every time he checked out a downtown condo he just couldn’t make the math work. “I could maybe afford a one bedroom but even then the $500 to $700 extra in monthly maintenance fees were outrageous.” And renting seemed absurd to Jason. “It was tough to find a rental and even when I did, I felt like I was throwing money away.”

About to throw in the towel and resign himself to a few more years in his parents’ basement, Jason came across “a miracle” and ended up buying it—a two-bedroom, new-build condo in North York that fit his budget. And it started with a web search on affordable housing.

Jason isn’t the only Canadian struggling to get into the housing market. Since 2001, the typical Canadian home has more than doubled in value. This substantial increase in property prices has created an affordability crisis that’s hit first-time buyers hard, particularly in the nation’s two hottest real estate markets, Toronto and Vancouver. Statistics from the Bank of Canada show that as many as 10% of households walk what BoC Governor Stephen Poloz calls the “insolvency line.” In December 2015, Poloz went as far as to warn the nation that our ever-increasing mountain of household debt was “the most-important vulnerability to [Canada’s] financial system.” According to BoC statistics, the most vulnerable are Canadians aged 45 and younger. These are the workers with less job security and who usually earn less money. Roughly 10% of mortgage holders hold the lion’s share of Canada’s household debt (a whopping 350% when compared against annual gross income). Poloz also notes that those Canadians with high-household debt have actually doubled since 2008, when the global economic crisis hit. The rise is due, in part, to the growing number of first-time buyers—those scraping together a down payment just to get into the market and who are now vulnerable to any interest rate hikes. Even so, the ranks of first-time buyers surprisingly continue to swell, with homeownership hitting an all-time high in 2014, when almost 68% of Canadians owned a piece of the real estate market.

Yet, there is a question that begs an answer: If the new cohort of first-time buyers carry lower pay and less secure jobs, how are they managing to get into the housing market? And what can we learn from them? We talked to first-time buyers from across Canada to find out how they did it. What we found is that there’s more than one way to make owning a home goal work. But, quite often, there are a few key concepts that must be followed. Here’s what these first-time buyers learned about achieving their homeownership dream.

After splitting with his wife, Jason moved into his parents’ basement. “It was supposed to be temporary, but I was there for a couple of years,” he recalls. The advantage was that the shift-worker was able to save about $25,000 for his own place. But even this wasn’t enough. “Maybe I could’ve bought a place, but the ongoing monthly expenses would have left me with nothing,” he says, “and that’s no way to live.” Then, one night, in a moment filled with despair and frustration, he sat down in front of his computer and typed in the words: Affordable housing. It’s a moment that changed his life.

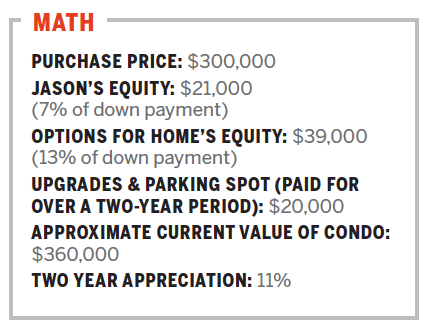

Within weeks Jason was in the backroom of a Toronto Public Library, near Lawrence and Bathurst listening to an Options For Homes sales pitch. “It was a no-frills seminar by a builder who offered buyers as much as 13% credit towards a 20% down payment on a condo unit,” recalls Jason. This equity top-up meant Jason could avoid adding more than $10,000 in CMHC mortgage loan insurance fees to his costs. It also meant he could buy now, rather than sitting on the sidelines for a few more years.

“Really consider all the costs of homeownership, including maintenance fees, parking, even utilities,” says Jason

Today, Jason is the proud owner of an 810-square-foot, two-bedroom condo unit with floor-to-ceiling windows located in the up-and-coming Englemount community (just beside Toronto’s famous Forest Hill neighbourhood). “We have a home. I’m building equity and I can still take my little girl out for treats.”

Truth is, Jason already knew about a few municipal, provincial and federal homeownership assistance programs, but he wasn’t eligible. “Many are geared to income, and with an annual salary of just over $40,000 per year, I made too much,” he says. Other programs require that the homeowner fit into specific criteria. For instance, Habitat for Humanity builds just over 200 homes per year, but you must be a low-income family to qualify. What Jason learned is that Options For Homes doesn’t operate under those constraints. As a not-for-profit builder, the aim is to “help anyone that could qualify for a mortgage, to get into the housing market,” explains Mary Pattison, director of sales and marketing for the builder.

To be able to afford this, Options For Homes takes a no-frills approach to their buildings: There are no pools, saunas or weight rooms, no 24-hour concierge and no fancy foyer artwork. Not only does this keep ongoing monthly maintenance costs down, but what’s saved is passed on to the buyer, in the form of an equity credit. “Options For Homes provides up to 13% equity to each buyer,” says Pattison. “This becomes a registered second mortgage that’s paid back in full, either when the owner decides to sell or rent out the unit.”

How do you take a $20,000 inheritance and turn it into $230,000 in just four years? Buy a house with friends, fix it up and sell it. Simple, right? Not quite.

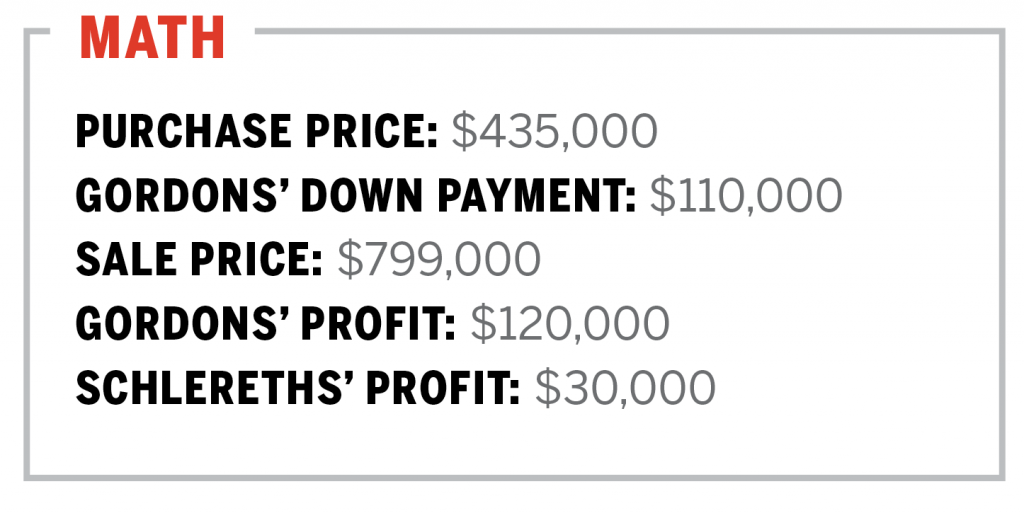

In 2010, Rachel Gordon’s grandpa left her a small inheritance. At the time, she and her husband Josiah wanted to buy a home. They weren’t alone. Rachel’s good friend, Claudie and her husband Miguel Schlereth also wanted to get into the property market, but they didn’t have any money saved for a down payment. So the two couples struck a deal. The Gordons would use their inheritance to buy a tiny post-war bungalow with an unfinished basement in Newmarket, Ont. The Schlereths would renovate the basement and occupy the suite. Once done, they’d sell it, use the money to buy a larger home, renovate it too and flip it. All together.

By October 2012, the two couples were the proud new owners of a dilapidated three-story “character” home, also in the Newmarket area. “It was listed at $580,000, but it was in such rough shape that we bargained the price down to $435,000,” says 35-year-old Josiah.

“If you’re buying a house to flip with a friend, remember that it’s a business decision. You’re not doing it to have a better friendship, you’re doing it to have a better financial future,” says Josiah.

At the time of purchase, both couples had the option of taking an equity stake in the flip-house but the Schlereths only chose sweat equity, so the two couples came to an agreement: Rachel and Josiah would go on the title for the home and take responsibility for the cost of the renovations and for the majority of the monthly costs; everyone would live in the home during the renovations, which would last for about two years, at which point the house would go back on the market. Once sold, the Gordons would receive approximately 70% of the profit and the Schlereths would get about 30%, once all expenses had been reimbursed and fees paid.

“Looking back, it would’ve been a good idea to have a signed contract,” says Josiah. “It seems like a cold thing to do. We’re all friends, we all agree. But a renovation is a fluid project and a contract would’ve standardized the process and kept everyone’s interests safe.” Take for instance, the moment when the Schlereths realized that, for the sake of their own sanity and for the friendship, they just had to move out. It was just a few months left on the renovations, but, as Josiah recalls, “it was hard for four adults and four children to share such a small space.”

Also renovations on an old, worn-down house don’t follow a simple path. “We’d have a renovation plan, only to find a problem that had to be dealt with immediately,” explains Josiah. Like when the city’s water pipe, that ran under the house, burst, leaking water into the home’s foundation. “I had to rent equipment to trench the concrete before getting a plumber to fix the pipes,” says Josiah. And on and on it went. They’d spend a few days tackling a scheduled part of the renovation, only to have a problem crop up, at an unanticipated cost and adding time to the overall project. “At one point, we only had one, shared living room and one working bathroom and when you add job losses, business start-ups, parenting styles, and the stress a newborn baby brings, you can imagine how hard it was for all of us.”

But they did it. The Schlereths moved out while the renovations were completed and in June of 2015, the home went on the market. Two months later it was sold. Yet, when asked if he’d ever again buy a house with a friend to renovate, sell and earn a profit Josiah’s reply is instantaneous: “No.” He adds, “there’s no way we could’ve bought our current house without all the work we did with our friends on the flip house, but it came with a lot of stress and strain. I’m glad we did it. Financially it put us in a much better position. I just don’t want to do it again.”

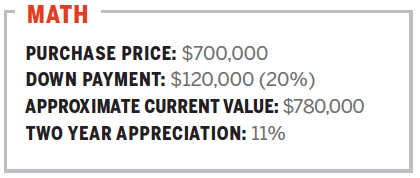

Jessica Whiting, 30, and her husband Chris 39, consider themselves fortunate. They have a beautiful family, complete with two-year-old Benjamin and another child on the way. They live in a family-sized home in Calgary and own a trailer in Invermere, B.C. But, like many non-native Calgarians, they long for the day when they can pack it all in and move full-time back to their home province. “All of our family is in B.C.,” says Jessica, “and with little ones you really begin to miss your roots.” Yet, just over three years ago they weren’t thinking about retirement, proximity to extended family or work/life balance. They were first-time home buyers saving and struggling to just get into the market. “I’m a type-A personality,” confesses Jessica, “so our house-hunting took us all over Calgary and into about 90 homes before we settled on a place in the Strathcona Hill neighbourhood.” What guided Jessica and Chris on their search was their spreadsheet of must-haves, would-likes and the deal-breakers. (Jessica even went as far as to give each value a weighting, so she could see how each property rated on their desire list.) “I was trying to find and buy a 20-year solution,” she says, “which is very hard. You never really know what’s going to happen.” In the end, the couple settled on what they thought was the perfect four-bedroom, 2,400-square-foot home. “It had a huge front yard,” says Jessica, “but now that I have a toddler I realize how little we can use that big green space in the front, because it opens up to the road. We just never realized that having a small backyard would be a hindrance for such an active little guy.”

“Don’t buy a forever home. Buy a right-now home; a home that will last you six to 10 years, then reevaluate at that time,” advises Jessica

Still, she doesn’t think they did too badly. “We don’t have a mountain view, but we’re perched on a hill with a lovely view of downtown Calgary.” Better still, because they stuck to their budget, they know that they can carry the house on just Chris’s salary of about $120,000 per year. That means Jessica’s part-time hours as a freelance graphic artist provides the family with extra spending cash. “Doing it this way meant going back to work was a choice, rather than a need. It gave us options, and that’s a great feeling.”

Yet, despite all the planning and number crunching, the couple were caught off-guard with the details. For instance, they purchased a home with an unfinished basement, which they turned into a mortgage-helper rental suite. “Between the cash we saved and the RRSP money we used through the Home Buyers’ Plan, we managed to put $120,000 down. Our mortgage was still big, at $580,000, but it was manageable, particularly with the extra rental income.” But a year passed and both Jessica and Chris realized that even with the extra cash the complications of being a landlord didn’t suit them. Also, it was hard to find a tenant that didn’t mind newborn baby screams and, now, the pitter-patter of toddler feet. “That extra money looked great on paper,” says Jessica, “but we just didn’t realize how much we valued our privacy.” A year in, the Whitings stopped renting out their basement.

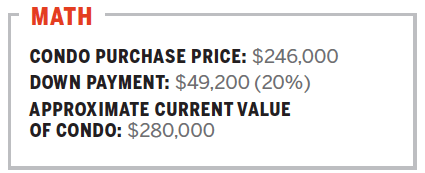

Jenna Pettinato, 32, and Nick Mizera, 29, had a goal: Find a resale condo in the east end of Toronto, that would allow them the chance to grow as a family. As a result, the couple looked at more than 80 units before settling on a 550-square-foot, one-bedroom unit way out on the west side of town. “It wasn’t a compromise,” says Jenna. “It was a strategy.”

While the couple watched friends stretch their budgets, they decided to be realistic. Rather than spending $120,000 more to get a second bedroom, Nick and Jenna took a good, hard look at their current needs and their future plans.

“We realized, this isn’t our forever home,” says Jenna. “We didn’t need to plan for every contingency.” Rather than focus on how much space they could buy, the couple focused on their budget. The goal was to keep the mortgage, interest and property tax payments to about $1,200 per month—what they previously paid in rent. One reason was that at the time of purchase, in September 2015, Nick was still a freelance writer with irregular pay (he’s known as the Gentleman Journalist). “We needed to know that we could carry the place and build equity on just one salary,” he explains. And the move west? “We realized that being in a particular neighbourhood wasn’t as important as whether or not we could continue doing what we loved.” These days, Nick and Jenna are planning their wedding, while enjoying what they call their “big backyard,” Toronto’s waterfront. “When we do move, we probably won’t head back into the city,” says Jenna. Instead, the couple have their sights set on commuter-friendly Hamilton, Ont. Still, Nick confesses, “we’re never going to own a sprawling 3,000-sq-ft home. We never want to live beyond our means.”

“We realized, this isn’t our forever home,” says Jenna. “We didn’t need to plan for every contingency.” Rather than focus on how much space they could buy, the couple focused on their budget. The goal was to keep the mortgage, interest and property tax payments to about $1,200 per month—what they previously paid in rent. One reason was that at the time of purchase, in September 2015, Nick was still a freelance writer with irregular pay (he’s known as the Gentleman Journalist). “We needed to know that we could carry the place and build equity on just one salary,” he explains. And the move west? “We realized that being in a particular neighbourhood wasn’t as important as whether or not we could continue doing what we loved.” These days, Nick and Jenna are planning their wedding, while enjoying what they call their “big backyard,” Toronto’s waterfront. “When we do move, we probably won’t head back into the city,” says Jenna. Instead, the couple have their sights set on commuter-friendly Hamilton, Ont. Still, Nick confesses, “we’re never going to own a sprawling 3,000-sq-ft home. We never want to live beyond our means.”

Related:

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Learn how the federal government’s 2024 budget can affect you and your money.

Presented by

Ratehub.ca