Paying off the mortgage in 10 years

This couple is on track to pay off the mortgage by the time their kids go to college.

This couple is on track to pay off the mortgage by the time their kids go to college.

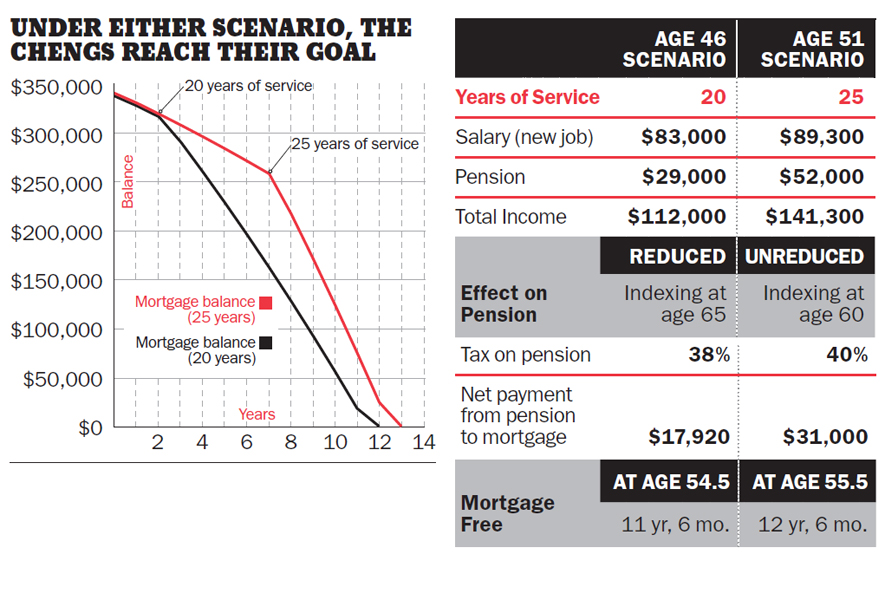

Derek and Julia Cheng, both 43, would love to pay off their $342,000 mortgage by age 55. “Our kids are 12 and 8,” says Derek, a police officer in Greater Vancouver. “We’d like to be mortgage-free by the time they’re in college.” Derek says he has two choices. He can work until 45, then retire from the force with an early but reduced annual pension around $22,000. Then he would take a job with a different police force and still earn $81,000 annually. Along with the $21,000 the Chengs now pay annually on the mortgage, Derek plans to put the entire $22,000 annual pension toward paying down the principal. “I’m just not sure if 10 years of extra payments will be enough to have the mortgage paid off by 55,” he says.

The second option is for Derek to retire from the force at 51. At that time, he thinks he would get an annual pension of $42,000. Again, he would get a job with a different police force and put the entire $42,000 annual pension towards the mortgage. “He’d love to do more volunteer work and possibly start a small business in his 50s,” says Julia, a part-time yoga instructor. “Paying off the mortgage quickly would help Derek achieve that goal.”

According to Tom Feigs, a financial planner with Money Coaches Canada in Calgary, Derek and Julia can have their mortgage paid off by age 55 using either scenario. “Derek is engaged in two ‘forced savings’ practices—building his pension and paying off the mortgage.” The police force Derek is with provides for a full and immediate pension after 25 years of service. Between 20 and 25 years, it is reduced by 5% per year to a maximum 25% reduction. Derek needs to reach his 20th year of service (in 2016) for his first opportunity at an immediate monthly entitlement and is just two years away from that milestone. After applying an income increase of 1.5% each year, Derek’s before-tax pension will be higher than he thinks. It would reach $29,000 annually if it starts in 2016 (at age 46) and $52,000 annually if he works until 51. Derek is on track to reach his goal using either scenario. “I think retiring at age 51 with the bigger pension is the more attractive path,” Feigs says. “Those extra five years of being in the force guarantees him a pension of $52,000 a year for life. I wouldn’t give that up.”

Do you want MoneySense to see if you’re on track to meet your own financial goal? If so, drop us a line at [email protected]

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Understanding industry jargon can make you a better real estate investor.

Learn how the federal government’s 2024 budget can affect you and your money.

The federal government is also raising the amount Canadians can pull from their RRSP to purchase a home through...

Created By

Ratehub

Canada may be likely to avoid a recession, but we won’t start recovering until the second half of 2024,...

Do Canadians have to file a trust tax return this year? What is a bare trust? What are the...

A new CMHC report says construction of new homes in Canada’s six largest cities remained near all-time high levels...

Financial experts debunk old money myths and offer advice that many Canadians might find more helpful today.

Presented By

National Bank of Canada