Are investment fees draining your portfolio?

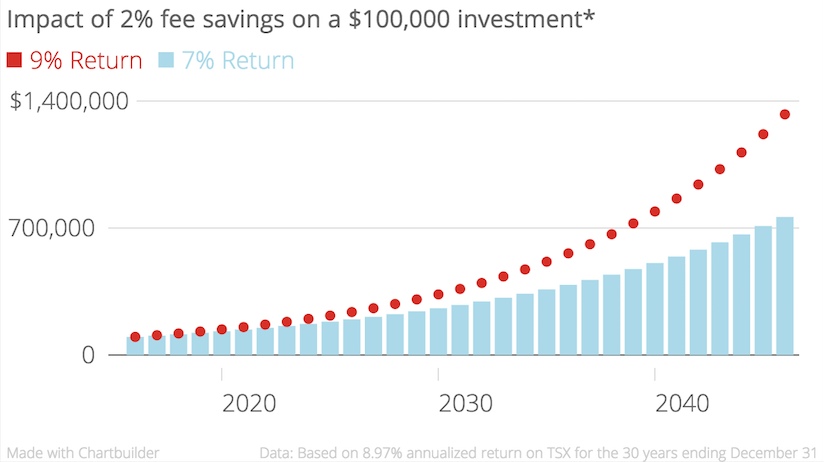

Saving just 2% on fees could earn you thousands more dollars over the life of your investments

Advertisement

Saving just 2% on fees could earn you thousands more dollars over the life of your investments

Want even more tips to shape up your finances? Join the Money Fit Club to curb spending, boost your earnings, lower your taxes and more!

Learn to tone your money muscles all year long with our interactive calendar and sign up for our weekly newsletter for advice straight to your inbox.

Want even more tips to shape up your finances? Join the Money Fit Club to curb spending, boost your earnings, lower your taxes and more!

Learn to tone your money muscles all year long with our interactive calendar and sign up for our weekly newsletter for advice straight to your inbox.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email