DRIP your way to investment success

Dividend reinvestment plans help build dividend income at little cost. They also protect long-term investors from crashes.

Advertisement

Dividend reinvestment plans help build dividend income at little cost. They also protect long-term investors from crashes.

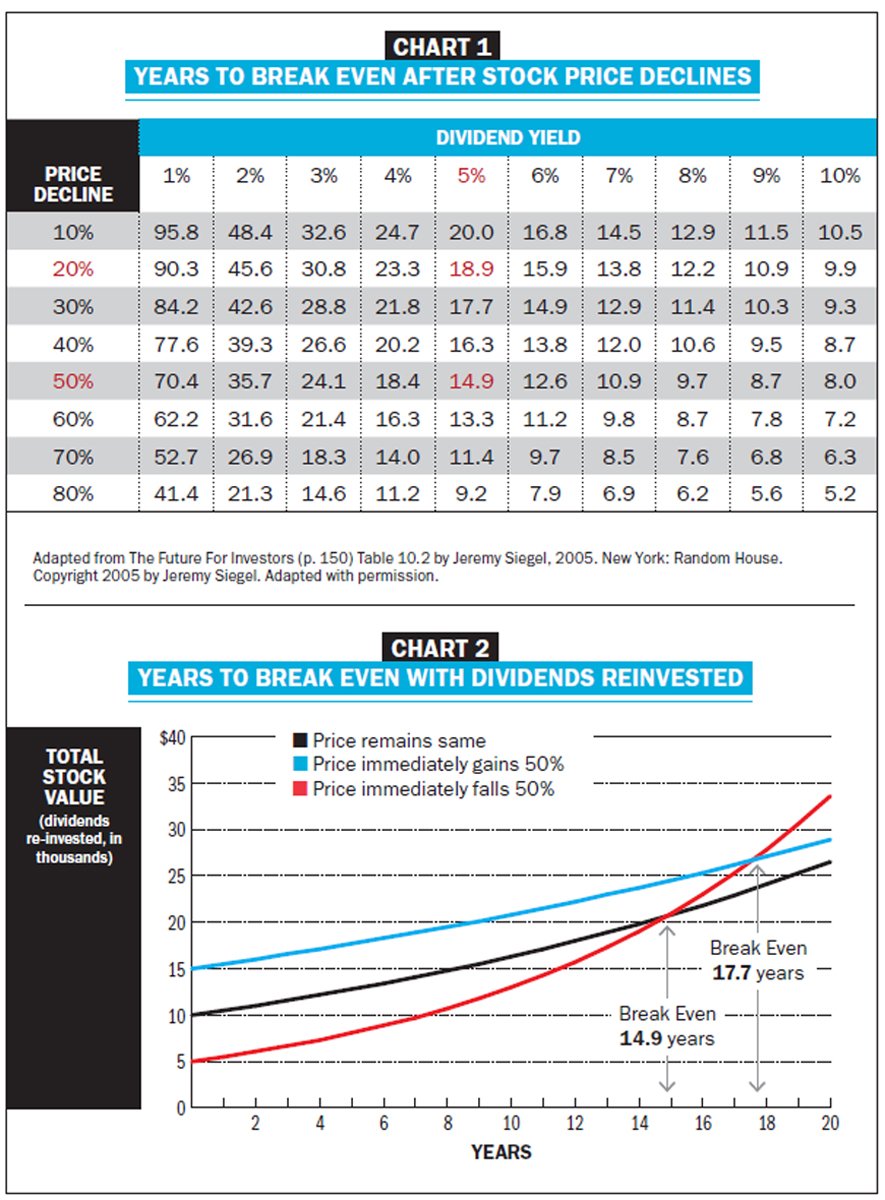

Chart 1 clearly demonstrates that across dividend yields and price declines, the more a stock falls, the less time it will take to recover from its losses. To reiterate Siegel’s point: “The value of these extra shares eventually surpasses the magnitude of the price decline, making the investors better off.”

Another easily observable generalization is the higher the dividend yield when dividends are reinvested, the less the number of years to recover from a price decline. At dividend yields of 5% and above, there is a distinct leveling off of their break-even points, eventually narrowing at 10% yields to between roughly six and 10 years.

Tables are good at presenting large amounts of data, but graphs make the points more easily understandable and memorable, so let’s bring this to life by rearranging the data and presenting it in Chart 2 in graphical form and continuing from our example.

In all scenarios, Chart 2 assumes an investor buys 500 shares of a $20 stock paying a constant annual dividend of $1.00 (or 5% yield) that’s reinvested. The black line shows the total value of the investment when a stock’s price remains unchanged at $20 throughout 20 years. It begins with $10,000 ($20 x 500 shares) and ends with just over $26,000 because of the reinvested dividends. Similarly, the red line represents its value after an immediate 50% price drop to $10 and the blue line after an immediate 50% increase in price to $30.

Confirming what we learned from Chart 1, the total value of a stock yielding 5% that suffered an immediate 50% decline in price and never recovered, intersects with the value of the unchanged black price line at 14.9 years. But the surprises don’t stop there. It’s not just when dividends are reinvested at lower prices (compared to unchanged prices) that an initially poor investment is transformed into a good one. This gives new meaning to the biblical expression “the last shall be first,” but also applies to “and the first last.” Further examination of Chart 2 reveals what I mean.

Leaving comparisons to Chart 1 behind, let’s use an even more extreme example. The blue line in Chart 2 shows the total stock value resulting from an instant 50% increase in the price that remains constant against that same 50% decline represented by the previously mentioned red line. As we can see, in about 17.7 years the stock that immediately dropped 50% in value surpasses its counterpart that had immediately increased by 50% just on account of the reinvested dividends acquired at lower cost.

That’s the power of reinvested dividends at lower prices. Over time, they can transform an instant winner into a longer term loser, making the first last and the last first. And we haven’t considered the gains when the price of a fallen stock recovers to its initial purchase price. Siegel referred to that result as the “Return Accelerator.” Also excluded was the positive effect of any possible dividend increases along the way.

There is however a problem with smaller account sizes, unless the stock is enrolled in a dividend reinvestment plan that can buy fractional shares. If this is not the case, it will be difficult for smaller accounts to balance the size of the investment to receive enough of a dividend to purchase at least one full share, while also maintaining an adequately diversified portfolio.

Consider a $50 stock yielding 3%. If dividends are paid quarterly, the investor receives $0.375 a share [($50.00 x .03) / 4]. But to receive enough cash from the quarterly dividend to purchase a full share would require an investment of $6,666.67 [($50.00 / $0.375) x $50.00]. And that assumes the stock never advances in price. To be safe, let’s add another 10% for that likelihood, bringing its cost to $7,333.34. And then use the Tax-Free Savings Account to demonstrate how account size can limit usefulness of dividend reinvestment plans that buy only full shares (rather than fractional amounts). Assume an individual has $31,000 in a TFSA and it holds only Canadian equities (to avoid paying unrecoverable withholding taxes on foreign dividends). To hold a minimum eight unrelated securities to diversify, that works out to $3,875.00 per holding. However we just calculated that $7,333.34 [$6,666.67 + 10% share price increase cushion] is needed to qualify for a single reinvested dividend share in future quarters. The more often a dividend is paid, the more the problem of being too small an investment size to qualify for reinvested shares when fractional share purchases are not available.

But if the same person controls a couple’s combined household TFSA accounts of $62,000, the $7,333.34 would meet the $7,750 [$62,000 / 8] investment amount for a minimum eight-stock diversification. This example of account type and size is just one of many angles to consider when making investment decisions. Something may be desirable when considered alone, but fail to meet the many broader needs of an investor. Portfolio design and construction are as important as security selection, and all individuals and households are in unique situations. One must balance and be mindful of competing demands. In this simple case the need to diversify conflicted with the need to have enough of a stock to take advantage of dividend reinvesting.

No wonder William Bernstein quipped in his 2001 book, The Intelligent Asset Allocator: “If you are a twenty-something just beginning to save, then get down on your knees and pray for a market crash.” Naturally, those approaching or in retirement won’t share that prayer, but we can be thankful for compounding reinvested dividends that keep giving—at any age.

This is behavioural finance at work. What seems to be common sense, reasonable and feels right doesn’t necessarily make as much money as what seems illogical, counterintuitive and feels bad.

The only problem is how many of us—regardless of investment time horizon —will enthusiastically embrace the next severe decline in our investment portfolios?

Fred Kirby is a fee-for-service certified financial planner, chartered investment manager and MBA, who writes an independent investment / financial planning newsletter from the outskirts of Armstrong, B.C.

Chart 1 clearly demonstrates that across dividend yields and price declines, the more a stock falls, the less time it will take to recover from its losses. To reiterate Siegel’s point: “The value of these extra shares eventually surpasses the magnitude of the price decline, making the investors better off.”

Another easily observable generalization is the higher the dividend yield when dividends are reinvested, the less the number of years to recover from a price decline. At dividend yields of 5% and above, there is a distinct leveling off of their break-even points, eventually narrowing at 10% yields to between roughly six and 10 years.

Tables are good at presenting large amounts of data, but graphs make the points more easily understandable and memorable, so let’s bring this to life by rearranging the data and presenting it in Chart 2 in graphical form and continuing from our example.

In all scenarios, Chart 2 assumes an investor buys 500 shares of a $20 stock paying a constant annual dividend of $1.00 (or 5% yield) that’s reinvested. The black line shows the total value of the investment when a stock’s price remains unchanged at $20 throughout 20 years. It begins with $10,000 ($20 x 500 shares) and ends with just over $26,000 because of the reinvested dividends. Similarly, the red line represents its value after an immediate 50% price drop to $10 and the blue line after an immediate 50% increase in price to $30.

Confirming what we learned from Chart 1, the total value of a stock yielding 5% that suffered an immediate 50% decline in price and never recovered, intersects with the value of the unchanged black price line at 14.9 years. But the surprises don’t stop there. It’s not just when dividends are reinvested at lower prices (compared to unchanged prices) that an initially poor investment is transformed into a good one. This gives new meaning to the biblical expression “the last shall be first,” but also applies to “and the first last.” Further examination of Chart 2 reveals what I mean.

Leaving comparisons to Chart 1 behind, let’s use an even more extreme example. The blue line in Chart 2 shows the total stock value resulting from an instant 50% increase in the price that remains constant against that same 50% decline represented by the previously mentioned red line. As we can see, in about 17.7 years the stock that immediately dropped 50% in value surpasses its counterpart that had immediately increased by 50% just on account of the reinvested dividends acquired at lower cost.

That’s the power of reinvested dividends at lower prices. Over time, they can transform an instant winner into a longer term loser, making the first last and the last first. And we haven’t considered the gains when the price of a fallen stock recovers to its initial purchase price. Siegel referred to that result as the “Return Accelerator.” Also excluded was the positive effect of any possible dividend increases along the way.

There is however a problem with smaller account sizes, unless the stock is enrolled in a dividend reinvestment plan that can buy fractional shares. If this is not the case, it will be difficult for smaller accounts to balance the size of the investment to receive enough of a dividend to purchase at least one full share, while also maintaining an adequately diversified portfolio.

Consider a $50 stock yielding 3%. If dividends are paid quarterly, the investor receives $0.375 a share [($50.00 x .03) / 4]. But to receive enough cash from the quarterly dividend to purchase a full share would require an investment of $6,666.67 [($50.00 / $0.375) x $50.00]. And that assumes the stock never advances in price. To be safe, let’s add another 10% for that likelihood, bringing its cost to $7,333.34. And then use the Tax-Free Savings Account to demonstrate how account size can limit usefulness of dividend reinvestment plans that buy only full shares (rather than fractional amounts). Assume an individual has $31,000 in a TFSA and it holds only Canadian equities (to avoid paying unrecoverable withholding taxes on foreign dividends). To hold a minimum eight unrelated securities to diversify, that works out to $3,875.00 per holding. However we just calculated that $7,333.34 [$6,666.67 + 10% share price increase cushion] is needed to qualify for a single reinvested dividend share in future quarters. The more often a dividend is paid, the more the problem of being too small an investment size to qualify for reinvested shares when fractional share purchases are not available.

But if the same person controls a couple’s combined household TFSA accounts of $62,000, the $7,333.34 would meet the $7,750 [$62,000 / 8] investment amount for a minimum eight-stock diversification. This example of account type and size is just one of many angles to consider when making investment decisions. Something may be desirable when considered alone, but fail to meet the many broader needs of an investor. Portfolio design and construction are as important as security selection, and all individuals and households are in unique situations. One must balance and be mindful of competing demands. In this simple case the need to diversify conflicted with the need to have enough of a stock to take advantage of dividend reinvesting.

No wonder William Bernstein quipped in his 2001 book, The Intelligent Asset Allocator: “If you are a twenty-something just beginning to save, then get down on your knees and pray for a market crash.” Naturally, those approaching or in retirement won’t share that prayer, but we can be thankful for compounding reinvested dividends that keep giving—at any age.

This is behavioural finance at work. What seems to be common sense, reasonable and feels right doesn’t necessarily make as much money as what seems illogical, counterintuitive and feels bad.

The only problem is how many of us—regardless of investment time horizon —will enthusiastically embrace the next severe decline in our investment portfolios?

Fred Kirby is a fee-for-service certified financial planner, chartered investment manager and MBA, who writes an independent investment / financial planning newsletter from the outskirts of Armstrong, B.C.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email