Digging for gold in Canadian small caps

Last issue, we looked at big returns from the top 100 U.S. small stocks. Here are the best Canadian small caps.

Advertisement

Last issue, we looked at big returns from the top 100 U.S. small stocks. Here are the best Canadian small caps.

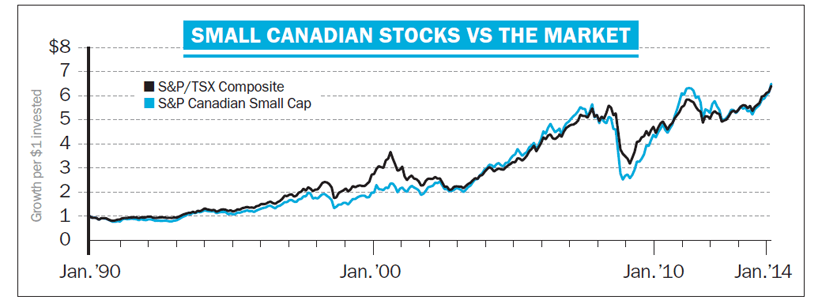

Consider a study in What Works on Wall Street. James O’Shaughnessy divided U.S. stocks in 10 groups by market capitalization, tracking them from 1927 to 2009.

He found the smallest stocks gained an average 10.9% annually, while average stocks climbed 10.5%. Returns varied only slightly as size rose; stocks in the third largest group fared better than average, with gains of 10.6% a year. But the real laggards were the largest stocks, which advanced only 8.8% per year.

As a result, long-term data supports the idea of tilting away from large stocks. Otherwise, small size in and of itself doesn’t provide a huge advantage. Investors are better off looking for good stocks based on fundamentals.

This works well for the MoneySense Top 200, which focuses on the largest Canadian stocks by revenue, not market cap. Due to space constraints, we leave out many small companies from our annual survey. This column should help to rectify that.

Each stock in the Top 200 is graded for its value and growth appeal. For growth, we favour firms that have increased sales and earnings per share at a good clip. We like strong returns on equity, healthy market performance over the last year, and low-to-moderate price-to-sales ratios. For value, we prefer stocks selling at modest price-to-book-value ratios versus peers and the market. High debt loads are negative and extra points go to profitable ventures paying dividends. Those in the top of the class must possess all these qualities.

The Dec/Jan MoneySense contains some interesting stocks with market caps under $1 billion: Aecon Group (ARE), Cervus Equipment (CVL), Canam Group (CAM), Newalta (NAL), and Martinrea International (MRE).

Stocks with good grades too small to make it into the Top 200 include Akita Drilling (AKT.A), Automodular (AM), Clarke (CKI), EGI Financial (EFH), Exco Technologies (XTC), High Arctic Energy Services (HWO), and HNZ Group (HNZ.A).

But as with all screening processes, you occasionally get a dud. It’s particularly important to give small stocks more scrutiny.

Tiny Automodular (AM) provides an object lesson on the danger of buying small stocks based only on financials. The autoparts company in Ajax, Ont., scored well on value and was only slightly lacking on the growth side. It pays a 10% dividend yield, trades at five times trailing earnings, and its earnings have grown nicely. Sadly, the numbers don’t account for a looming disaster: its main customer, Ford Motor Co. (F), said it won’t need Automodular’s services by the end of 2014. Gulp!

Automodular is looking for other business, but the search isn’t going well. A dramatic business change is likely, which precludes an investment by non-specialists.

The picture is brighter at EGI Financial Holdings (EFH), which scores well on value and growth. This small property and casualty insurance firm in Mississauga, Ont., focuses on non-standard auto and other speciality insurance. I bought it for my own portfolio and it’s still interesting. It trades at 12 times earnings, has a small discount to book value, and pays a 3% dividend yield. If you’re in the market for a small stock, it may be worth a second look.

Norm Rothery, CFA, PhD, is the founder of StingyInvestor.com. Follw him on twitter at @NormanRothery

Consider a study in What Works on Wall Street. James O’Shaughnessy divided U.S. stocks in 10 groups by market capitalization, tracking them from 1927 to 2009.

He found the smallest stocks gained an average 10.9% annually, while average stocks climbed 10.5%. Returns varied only slightly as size rose; stocks in the third largest group fared better than average, with gains of 10.6% a year. But the real laggards were the largest stocks, which advanced only 8.8% per year.

As a result, long-term data supports the idea of tilting away from large stocks. Otherwise, small size in and of itself doesn’t provide a huge advantage. Investors are better off looking for good stocks based on fundamentals.

This works well for the MoneySense Top 200, which focuses on the largest Canadian stocks by revenue, not market cap. Due to space constraints, we leave out many small companies from our annual survey. This column should help to rectify that.

Each stock in the Top 200 is graded for its value and growth appeal. For growth, we favour firms that have increased sales and earnings per share at a good clip. We like strong returns on equity, healthy market performance over the last year, and low-to-moderate price-to-sales ratios. For value, we prefer stocks selling at modest price-to-book-value ratios versus peers and the market. High debt loads are negative and extra points go to profitable ventures paying dividends. Those in the top of the class must possess all these qualities.

The Dec/Jan MoneySense contains some interesting stocks with market caps under $1 billion: Aecon Group (ARE), Cervus Equipment (CVL), Canam Group (CAM), Newalta (NAL), and Martinrea International (MRE).

Stocks with good grades too small to make it into the Top 200 include Akita Drilling (AKT.A), Automodular (AM), Clarke (CKI), EGI Financial (EFH), Exco Technologies (XTC), High Arctic Energy Services (HWO), and HNZ Group (HNZ.A).

But as with all screening processes, you occasionally get a dud. It’s particularly important to give small stocks more scrutiny.

Tiny Automodular (AM) provides an object lesson on the danger of buying small stocks based only on financials. The autoparts company in Ajax, Ont., scored well on value and was only slightly lacking on the growth side. It pays a 10% dividend yield, trades at five times trailing earnings, and its earnings have grown nicely. Sadly, the numbers don’t account for a looming disaster: its main customer, Ford Motor Co. (F), said it won’t need Automodular’s services by the end of 2014. Gulp!

Automodular is looking for other business, but the search isn’t going well. A dramatic business change is likely, which precludes an investment by non-specialists.

The picture is brighter at EGI Financial Holdings (EFH), which scores well on value and growth. This small property and casualty insurance firm in Mississauga, Ont., focuses on non-standard auto and other speciality insurance. I bought it for my own portfolio and it’s still interesting. It trades at 12 times earnings, has a small discount to book value, and pays a 3% dividend yield. If you’re in the market for a small stock, it may be worth a second look.

Norm Rothery, CFA, PhD, is the founder of StingyInvestor.com. Follw him on twitter at @NormanRothery

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email