Minimize investment fees to improve returns

Here's a great tool for keeping your focus on the fees you're paying.

Advertisement

Here's a great tool for keeping your focus on the fees you're paying.

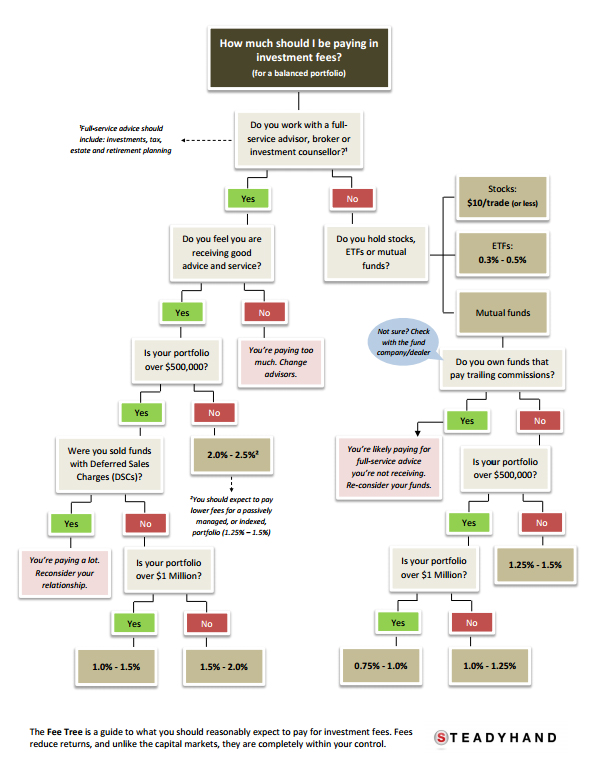

The guys and gals at Steadyhand, one of Canada’s low-fee, no-commission actively-managed mutual funds providers, have put together something they call “The Fee Tree.” Working with the conventional family tree structure and with their analysis focused on a balanced portfolio, they describe the range of fees Canadian investors should reasonably expect to pay if they’re working with a full-service adviser, broker, investment counsellor, or if they manage their own investments with a discount brokerage.

After initially determining what type of investment plan you’re using, the Fee Tree quickly branches off into more nuanced questions appropriate to your particular situation. Along the way, good advice is given. Some of it is dead simple but important nonetheless: if you’re not receiving appropriate advice and service, you absolutely need to change advisers. But elsewhere more deft advice is provided as it relates to fees. For instance, if you were sold funds with deferred sales charges (DSC: those nasty back-end fees that lock investors into products for years), you’re paying a lot and should reconsider your relationship with your adviser, Steadyhand says. My advice would, however, would be more pointed: Don’t walk away from your adviser, RUN!

For those not working with active advisers, there are also good reminders of how low fees can be if you build your own portfolio with cheap exchange-traded funds (ETFs), in which management expense ratios (MERs) can be as little as 0.30% (so Steadyhand’s Fee Tree declares, although some are as low as 6 or 7 basis points). As for mutual funds, Steadyhand’s advice seems to be limited to actively managed funds in which a do-it-yourself investor should be able to build a balanced portfolio with an MER of around 1.0% (with the caveat, of course, that you’re not buying funds that pay a trailing commission). Missing from Steadyhand’s analysis, however, are low-fee index mutual funds. For instance, with TD’s e-Series funds you could build a balanced Couch Potato portfolio with an MER of about 0.40%. Check out MoneySense Editor-at-Large Dan Bortolotti’s Canadian Couch Potato blog for more details.

All in all, though, Steadyhand’s Fee Tree is a great tool for keeping your focus on the fees you’re paying in exchange for service and advice. The cover story (“Best Tips Ever“) from MoneySense‘s current 15th Anniversary issue really hammers away at that point here: Investors must always watch out for hidden fees and biased advised, and keep costs low in order to keep more of their returns.

If you’re not satisfied with the fees you’re paying, as Steadyhand’s Scott Ronalds succinctly puts it, “maybe it’s time to shake the tree.”

The guys and gals at Steadyhand, one of Canada’s low-fee, no-commission actively-managed mutual funds providers, have put together something they call “The Fee Tree.” Working with the conventional family tree structure and with their analysis focused on a balanced portfolio, they describe the range of fees Canadian investors should reasonably expect to pay if they’re working with a full-service adviser, broker, investment counsellor, or if they manage their own investments with a discount brokerage.

After initially determining what type of investment plan you’re using, the Fee Tree quickly branches off into more nuanced questions appropriate to your particular situation. Along the way, good advice is given. Some of it is dead simple but important nonetheless: if you’re not receiving appropriate advice and service, you absolutely need to change advisers. But elsewhere more deft advice is provided as it relates to fees. For instance, if you were sold funds with deferred sales charges (DSC: those nasty back-end fees that lock investors into products for years), you’re paying a lot and should reconsider your relationship with your adviser, Steadyhand says. My advice would, however, would be more pointed: Don’t walk away from your adviser, RUN!

For those not working with active advisers, there are also good reminders of how low fees can be if you build your own portfolio with cheap exchange-traded funds (ETFs), in which management expense ratios (MERs) can be as little as 0.30% (so Steadyhand’s Fee Tree declares, although some are as low as 6 or 7 basis points). As for mutual funds, Steadyhand’s advice seems to be limited to actively managed funds in which a do-it-yourself investor should be able to build a balanced portfolio with an MER of around 1.0% (with the caveat, of course, that you’re not buying funds that pay a trailing commission). Missing from Steadyhand’s analysis, however, are low-fee index mutual funds. For instance, with TD’s e-Series funds you could build a balanced Couch Potato portfolio with an MER of about 0.40%. Check out MoneySense Editor-at-Large Dan Bortolotti’s Canadian Couch Potato blog for more details.

All in all, though, Steadyhand’s Fee Tree is a great tool for keeping your focus on the fees you’re paying in exchange for service and advice. The cover story (“Best Tips Ever“) from MoneySense‘s current 15th Anniversary issue really hammers away at that point here: Investors must always watch out for hidden fees and biased advised, and keep costs low in order to keep more of their returns.

If you’re not satisfied with the fees you’re paying, as Steadyhand’s Scott Ronalds succinctly puts it, “maybe it’s time to shake the tree.”

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email