Even the rich need an investment plan

Will the Batemans be able to make their money last?

Advertisement

Will the Batemans be able to make their money last?

If you visit Morley and Sandy Bateman in their beautiful home on any given weekend, chances are you’ll find them packing their bags for one of the exotic locations they travel to throughout the year. Their latest vacation was a week in France, complete with wine tasting, fancy dinners in five-star restaurants and jaunts to the opera, symphony and local festivals. “Over the last 22 years, we’ve travelled to Europe 200 times, sometimes just for the weekend,” says Morley, a dentist in Toronto. “France and Italy is our ‘up north.’ Instead of driving up the highway to cottage country, we go to Paris or Capri for a few days. No cottage maintenance, no cutting the grass. It’s wonderful.”

The Batemans want to grow their money so they have enough to retire in two years and support the luxurious lifestyle they crave. That will be tough, because most of their money is in cash earning almost nothing. “I panicked and sold all our stocks in 2011,” Morley says. “Now I feel paralyzed when I try to buy stocks because I really feel we’re in a stock market bubble.”

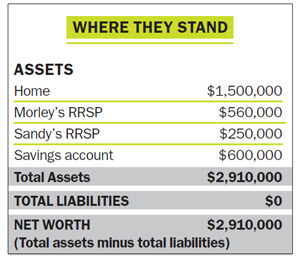

The Batemans (whose names we’ve changed) have assets most couples would envy: a spacious $1.5 million home in a prime Toronto neighborhood and more than $1.4 million in RRSPs and other savings. Their annual income is a combined $200,000, though just two years ago it was closer to $300,000. Morley sold his dental business last year for $500,000. He now works four days a week and earns a $150,000 salary. Sandy owns a travel agency in Oakville, Ont., and earns $50,000.

The Batemans are both 58, have a 26-year-old daughter, Katrina, who’s now financially independent. They want to retire at age 60, when they plan to sell Sandy’s travel agency for about $300,000. That would give them a net worth of roughly $3.2 million.

“We’ve been very lucky in that we’ve both worked at jobs we loved and made good incomes,” says Sandy, who’s been in the travel business for more than 30 years. “But we’re ready to retire and start the next phase of our lives.”

Their plan is to sell their home and buy two properties: a $700,000 home in Florida and a $500,000 condo in Toronto. The remaining $300,000 will pad their retirement savings. Add that to the $1.4 million they already have, and another $300,000 Sandy expects to get from the sale of the travel agency and in two years they’d have a total investment portfolio of around $2 million (not including real estate).

“We like the idea of living part of the year like snowbirds,” says Sandy. “The cost of living is a lot lower in Florida than Canada so there will be some savings there. And while we plan to pare down our travel as we get older, we do plan to spend about $40,000 a year on travel until age 75.”

The Batemans say they don’t plan to leave a large estate for their daughter. They paid more than $500,000 in private-school tuition for Katrina, and she’s now a chartered accountant. “If there’s money left in the estate at the end, that’s fine,” says Morley. “But as an accountant she’ll always earn a good living. She doesn’t need money from us.”

If their portfolio proves too small to sustain their planned lifestyle, the Batemans would consider working past 60. “I love my job and could stay longer if I have to,” says Morley. “Sandy, too. If she sold the travel agency she could still work as a consultant while we spend a few months in Florida every year.”

One thing is certain: the couple’s investment portfolio will have to generate most of the income they live on in their golden years. While they will both be entitled to full CPP and Old Age Security, neither has a company pension. The problem is they don’t have a workable investment plan yet: all their money is in cash. “I know that is not smart,” says Morley. “But with all this talk of the U.S. debt ceiling, the sequester and a weak economy, I’m not sure what the smartest way to build a portfolio would be right now. I have always done all of our investing, and I think dividend-paying stocks would probably be ideal for a conservative retirement portfolio. I’m just not sure how to do it, or whether $2 million will be enough. We feel stuck.”

The couple expects to need $120,000 in pre-tax income in retirement, with a large share of that earmarked for travel. That’s a passion Morley and Sandy have always shared. Morley grew up in Toronto, where his dad was a doctor who travelled a lot. Then he went to high school in Geneva, which is where his love for Europe really deepened. “My family went to Europe every year. I got my taste for travel from those family experiences, and from my four years attending high school there.”

Sandy’s dad was a businessman who also had wanderlust. “He took my sister and me everywhere with him,” Sandy says. “I loved it. It felt natural for me to go into the travel business.”

Morley completed an undergraduate degree in science at the University of Toronto and a master’s degree and doctorate from Tufts University in Boston. Sandy has an undergraduate degree in biology from McGill. Soon after graduation in 1978, she got a job at a small travel agency. “I was in the agency by myself most of the time, so I learned the ropes quickly,” she says. In 1986, Sandy had an opportunity to buy her own travel agency, and jumped at it. “I’m a businessperson at heart.”

When Morley and Sandy met in 1990 they quickly stumbled on their common interest. “Sandy was my patient,” laughs Morley. “We bonded while she sat in my dental chair with a mouth full of cotton. Isn’t that romantic? We learned we both loved travel and I asked her for a date. She said yes, probably after all the drugs I pumped into her.”

At the time, Sandy was a single mom with a daughter from a previous relationship. When the couple married in 1991, Morley adopted Katrina. Six years later they bought their tony Toronto home for $429,000. Over the next 10 years they had two major expenses: Katrina’s private school bills, which amounted to $540,000 (including U.S. university fees), and their mortgage, which they paid off in 2004. “We paid the mortgage off quickly and Katrina’s school fees were worth it,” says Sandy.

All through the years, both Morley and Sandy made their maximum RRSP contributions, but didn’t put anything into their Tax-Free Savings Accounts. “I understand the tax implications of the TFSA,” says Morley. “And I know we should both put $25,500 into the accounts, but I just never got around to doing it.”

Until recently, Morley had the couple’s money invested in stocks like the Bank of Montreal, Royal Bank, Altria (formerly Philip Morris) and General Electric; most of the couple’s portfolio was split evenly between growth and dividend paying stocks.” But Morley, who insists he’s quite the risk taker in other areas of his life, panicked and sold all their stocks. The money—$810,000—now sits in cash in their RRSPs. They have another $600,000 in a non-registered account: most is money from the sale of Morley’s dental business.

The only thing the couple feels they need before they retire is a good investment plan. “We need to make sure our portfolio will spin off enough income,” says Morley. “I need to understand how best to rebuild my portfolio to make our retirement truly stress-free.”

Morley and Sandy Bateman have done many things right. “They have a lot of money to work with,” says Marc Lamontagne, a financial adviser with Ryan Lamontagne in Ottawa. “With $2 million by age 60 in RRSPs and non-registered accounts, they certainly have enough money to fund their retirement, but not if they have it sitting in cash.”

Heather Franklin, a fee-for-service adviser in Toronto, agrees they need to implement an investment plan to make sure their portfolio is sustainable. “There are a lot of options they haven’t considered, especially regarding their real estate. Unless they make some key choices, an affluent retirement is not a guarantee.”

Jim Otar, an independent financial adviser in Toronto, says the Batemans will have to regularly review their options as they approach age 65 to ensure they won’t outlive their money. To do that, here’s what the Batemans should do.

Rebuild their portfolio. The problem with managing your own investments is you’re often ruled by your impulses. “Morley’s sale of his entire portfolio in 2011 is not unusual,” says Lamontagne. “People get very fearful, especially when they’re coming up to retirement.”

Lamontagne notes that if the Batemans can achieve a 3% real rate of return (after taxes and inflation), they will be able to achieve their retirement goals of living comfortably, wintering in Florida and travelling the world. But to achieve that target rate of return, they’ll need to stick to a long-term plan and make sure they don’t abandon it if we experience another market crash. “Morley is knowledgeable, but he gets frozen by emotion,” says Lamontagne. “They’d benefit from having someone else manage their money.”

Lamontagne suggests the Batemans hire an investment counselling firm to manage their portfolio. Such firms usually charge a management fee of 1% or less on a $2 million portfolio. To help ease Morley’s anxiety he should keep an amount equal to two years of living expenses in cash. “That way he’s not forced to sell anything when markets are down,” says Lamontagne. “He can replenish the cash account when stock markets recover.”

Franklin believes Morley can manage on his own if he sticks to dividend-paying stocks and checks in with a fee-for-service planner annually. “He just needs a little help,” she says. “He was on the right track.” The cost? About $1,000 annually. A dividend strategy should also help Morley ignore the ups and downs of the market. “Although dividend stocks will fluctuate in value over time, most large-cap dividend-paying companies maintain their dividends through all market conditions,” says Franklin. “That’s very reassuring.”

Otar agrees, but stresses the Batemans should keep most of their portfolio in fixed-income investments, which should reduce volatility and make it much easier for them to stay disciplined. He says the couple can do well with a portfolio that’s 35% in dividend-paying stocks and 65% in laddered GIC rates if both Morley and Sandy delay retirement until age 62 and save as much as possible in registered accounts until their retirement.

“Morley should also consider working part time six months a year to age 65, and perhaps buy a cheaper Florida property in four years,” says Otar. “These things will help guarantee their money doesn’t run out before age 95.”

Reconsider buying a house in Florida. Although the Batemans can afford to buy a $700,000 home in Florida, Franklin is opposed to investing such a large sum in that state’s real estate market. “I don’t think they’ve thought this through carefully,” she says. “The Batemans will need to consult cross-border tax lawyers, take into account U.S. exchange rates and higher property taxes for non-residents, as well as the volatile Florida property market in a few years when they decide to sell.” They will also have to budget for high condo maintenance fees—easily $20,000 or more annually. “That will be a huge financial drain for them.”

Franklin would like to see the couple invest that $700,000 and simply rent whenever they want to go down south. She notes that for $5,000 a month they can rent a luxurious condo anywhere in Florida. “They can add that $700,000 to their investment portfolio and it will stay in Canada and grow with preferential tax treatment, with no U.S. laws and taxes to muddy the waters.” If they insist on buying, they should sell the Florida home by age 80 if they want their money to last until age 95—assuming a 3% annual increase on the Florida home.

Put money into TFSAs. The Batemans need to top up their TFSAs. In their 60s, their tax situation will get more complex and they’ll have to plan for such things as the Old Age Security clawback, which currently kicks in on incomes over $70,954. Any interest or dividends they earn inside a TFSA will not count as taxable income, so sheltering some of their investments will improve their bottom line.

The couple should review their financial plan annually and seek the advice of a good tax lawyer as they near age 65, at which point both will be eligible to collect full CPP and OAS. “Markets, interest rates and the inflation environment change quickly,” concludes Otar. “They will want to make sure to stay on the right track all through retirement.”

Would you like MoneySense to consider your financial situation in a future Family Profile? Drop us a line at [email protected]. If we use your story, your name will be changed to protect your privacy.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email