Building a low-fee portfolio that lasts

No more high-fee Canadian equity mutual funds. It’s time for a new portfolio that delivers more income and better returns with less risk

Advertisement

No more high-fee Canadian equity mutual funds. It’s time for a new portfolio that delivers more income and better returns with less risk

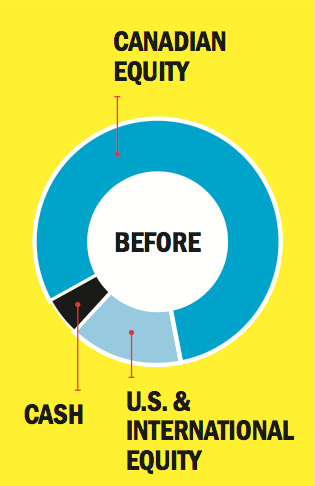

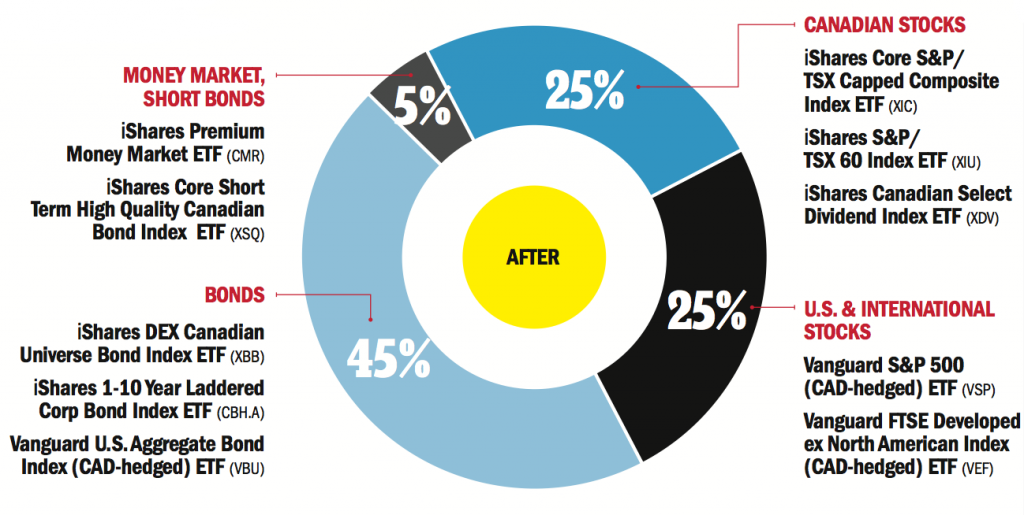

Cochrane, Alta. residents Edward, 60, and Penelope, 58, retired five years ago. Ed feels grateful to his former employer for his defined benefit pension plan, but he doesn’t feel that way about his adviser of 25 years. “We’re getting mediocre returns—we’re not even hitting the benchmarks,” he says. “We want a change.” Their portfolio includes $250,000 worth of Imperial Oil shares as well as registered and non-registered mutual funds. Their holdings are mostly in funds charging 2.2% in fees, with a whopping 80% weighted in Canadian equities. Their goal? “More income, more tax efficiency, and less fees.”

Cochrane, Alta. residents Edward, 60, and Penelope, 58, retired five years ago. Ed feels grateful to his former employer for his defined benefit pension plan, but he doesn’t feel that way about his adviser of 25 years. “We’re getting mediocre returns—we’re not even hitting the benchmarks,” he says. “We want a change.” Their portfolio includes $250,000 worth of Imperial Oil shares as well as registered and non-registered mutual funds. Their holdings are mostly in funds charging 2.2% in fees, with a whopping 80% weighted in Canadian equities. Their goal? “More income, more tax efficiency, and less fees.”

Do you want a portfolio makeover from MoneySense? If so, send an email describing your situation to [email protected]

Do you want a portfolio makeover from MoneySense? If so, send an email describing your situation to [email protected]

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email