Redemption from redemption fees

Rob and Christine are clients of a well-known investment firm but they want lower MERs. Should they bite the bullet?

Advertisement

Rob and Christine are clients of a well-known investment firm but they want lower MERs. Should they bite the bullet?

![Portfolio_Builder_banner_1256X300[2][2][2]](https://www.moneysense.ca/wp-content/uploads/2016/05/Portfolio_Builder_banner_1256X300222.jpeg)

Rob and Christine work for a youth-and-social-service agency and have no debt of any kind. After selling two rental properties and winding down their printing company, they realized their biggest yearly expense was fees on their investments.

“It’s hard to receive financial advice from an ‘adviser’ we feel is more of a box checker,” says a frustrated Rob. “When they lock us into DSCs, they receive up to 4.2% in commissions and we receive a mere 0.1% reduction in fees. Win-win? I think not.”

MoneySense showed their portfolio to Justin Bender, portfolio manager for PWL Capital in Toronto. He calculates they have been paying 2.58% in fees (more than $15,000 annually) and are getting little in the way of service.

Exiting the original crop of mutual funds would have meant redemption charges of $19,315. However, they withdrew the maximum 12% in 2013 and another 3% early in 2014. PWL’s analysis shows they will break even by May 2015: that’s when the savings from the lower ETF management fees will exceed the cost of the redemptions.

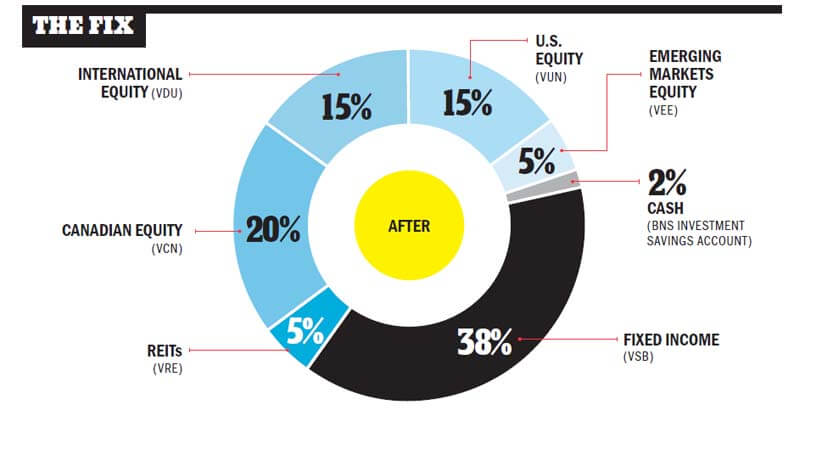

Total MER of the revamped all-Vanguard ETF portfolio (tickers shown in Fix) is a stingy 0.20%: under 10% of what the couple’s previous funds charged to cover similar asset classes. Using proper asset location, Bender put the 40% position in fixed income (and cash) in the RRSPs and TFSAs; the 55% in equity ETFs goes into taxable accounts, along with a 5% weighting in a real estate ETF.

Do you want a portfolio makeover from MoneySense? If so, send an email describing your situation to [email protected]

Rob and Christine work for a youth-and-social-service agency and have no debt of any kind. After selling two rental properties and winding down their printing company, they realized their biggest yearly expense was fees on their investments.

“It’s hard to receive financial advice from an ‘adviser’ we feel is more of a box checker,” says a frustrated Rob. “When they lock us into DSCs, they receive up to 4.2% in commissions and we receive a mere 0.1% reduction in fees. Win-win? I think not.”

MoneySense showed their portfolio to Justin Bender, portfolio manager for PWL Capital in Toronto. He calculates they have been paying 2.58% in fees (more than $15,000 annually) and are getting little in the way of service.

Exiting the original crop of mutual funds would have meant redemption charges of $19,315. However, they withdrew the maximum 12% in 2013 and another 3% early in 2014. PWL’s analysis shows they will break even by May 2015: that’s when the savings from the lower ETF management fees will exceed the cost of the redemptions.

Total MER of the revamped all-Vanguard ETF portfolio (tickers shown in Fix) is a stingy 0.20%: under 10% of what the couple’s previous funds charged to cover similar asset classes. Using proper asset location, Bender put the 40% position in fixed income (and cash) in the RRSPs and TFSAs; the 55% in equity ETFs goes into taxable accounts, along with a 5% weighting in a real estate ETF.

Do you want a portfolio makeover from MoneySense? If so, send an email describing your situation to [email protected]

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email