Investment returns: A great decade, after all

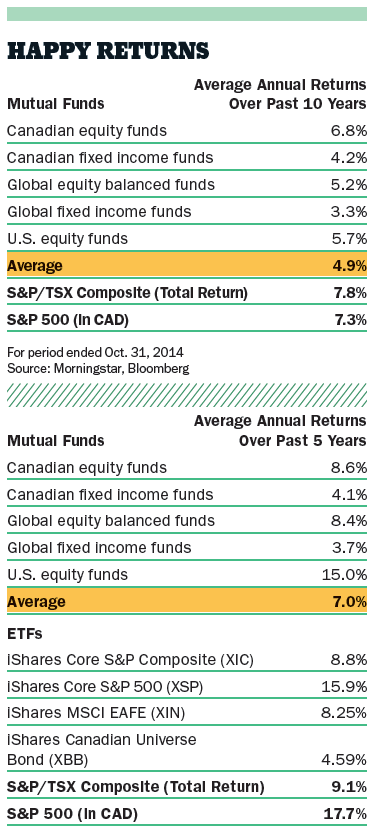

Investors who stayed in the markets have done remarkably well over the past 10 years—something we couldn’t have said as little as five years ago

Advertisement

Investors who stayed in the markets have done remarkably well over the past 10 years—something we couldn’t have said as little as five years ago

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email