Once you hit six figures, moving to ETFs and individual stocks can lower your investing costs and significantly boost returns. Here’s how to do it right

This article is 1 year old. Some details may be outdated.

Advertisement

(Photograph by Erik Putz)

A fancy new café opened recently in my neighbourhood and I’ve been happily testing out the beverages and baked goods it has on offer. After years of living in a good-coffee desert, the variety of choices is a little overwhelming.

In a similar way, once your portfolio grows beyond the $100,000 mark, a slew of new investing options become available. Determining which ones to use can be a daunting task and the stakes are much higher than those faced by the patrons of new cafés.

But just because you have access to new options doesn’t mean you should use them. The simple balanced methods highlighted in the preceding “Where to invest $10,000” section are still good choices. However, if you want a more customized approach with even lower fees, and you can handle market swings, then some of these new possibilities might be right for you.

The super-sized spud

In the preceding section I suggested starting with a small balanced portfolio composed of four TD Bank e-Series Funds, which cost only 0.44% per year in management fees. But once you have more money, you should think about opening a discount brokerage account and replacing those index funds with lower-cost exchange traded funds (ETFs). By doing so, you can lower your fees considerably, which will improve your performance over the long run, especially for larger accounts.

While ETFs usually have lower annual fees, they come with a catch: most brokerages charge a commission of $10 or so to buy or sell them.

Buying a portfolio of four ETFs would result in four commissions, so if you reinvest your dividends annually and make additional purchases each year at the same time, then your total cost will be about $40 per year. It doesn’t sound like a lot, but a $40 annual cost on a $10,000 portfolio is equivalent to a 0.40% annual fee, which is quite high.

The situation changes once your portfolio hits the $100,000 mark, however, because the brokerage costs become relatively small in percentage terms. For instance, $40 in commissions represents 0.04% of $100,000 portfolio. That’s why, when you hit the big leagues, I think it’s time to move to a balanced portfolio of ETFs. For instance, you could simply replace the Couch Potato portfolio in the last section with the following:

■ 40% Vanguard Canadian Aggregate Bond Index ETF (VAB)

■ 20% Vanguard FTSE Canada All Cap Index ETF (VCN)

■ 20% Vanguard U.S. Total Market Index ETF (VUN)

■ 20% Vanguard FTSE Developed ex North America Index ETF (VDU)

This balanced ETF portfolio provides broad exposure to the stock and bond markets for a total fee of only 0.18% annually plus the relatively small trading costs needed to set it up and maintain it. As a result, moving to ETFs can cut the annual cost of the Couch Potato Portfolio by about 50%.

Beating index funds with stocks

Once you have a larger portfolio, you may also start to consider buying individual stocks. It’s a good idea to start with a core balanced portfolio like the one I just discussed and use only a relatively small amount of money to buy stocks. New stock pickers might aim to put 5% to 10% of their overall portfolio into stocks. If you do, you should lighten up on your stock ETFs by the same amount to maintain your asset allocation.

When it comes to picking stocks, I recommend taking a long-term approach, avoiding unnecessary trading, and keeping your costs low. By doing so, you might actually beat index investors at their own game.

Consider the case of an investment trust that got its start way back in 1935. At the time, it was set up to buy and hold 30 large dividend-paying stocks. It acted like a super-passive index fund that used very simple rules. The trust held onto its stocks indefinitely and would only make changes in the event of corporate actions like mergers, accusations or spin-offs.

The amazing thing is, the trust is still going today and is now called the Voya Corporate Leaders Trust Fund. After all these year it holds 22 stocks and, as you might imagine, its portfolio looks a little peculiar, with out-sized holdings in Union Pacific, Berkshire Hathaway, and Exxon.

Despite its nearly catatonic level of passivity, from 1971 through to 2015 the trust generated average annual returns of 11.6%, which bested the S&P 500’s annual gains of 10.6%. It outperformed by 1 percentage point annually without doing much at all.

I don’t suggest adopting the trust’s current portfolio, but new stock pickers should emulate its philosophy.

If you’re keen on giving it a go, focus your efforts first on the Canadian stock market. While Americans have thousands of large stocks to choose from, there are only a few dozen big companies that trade on the TSX. For instance, you could replace a part of the Canadian component of your Couch Potato portfolio with, say, 20 Canadian dividend payers.

One way to build a buy-and-hold dividend portfolio is to get a few ideas from the Dogs of the TSX method I highlight in my Value Hunter blog at MoneySense.ca. The strategy involves buying the 10 highest-yielding stocks in the large-cap S&P/TSX 60 index, holding them for a year, and then moving into a new group of high yielders.

However, a very passive portfolio can be built by holding on to the stocks indefinitely and adding any new stocks that appear on the Dogs list each year. If you do so, it should be possible to build a reasonably diversified list of 20 dividend-paying stocks in just a few years.

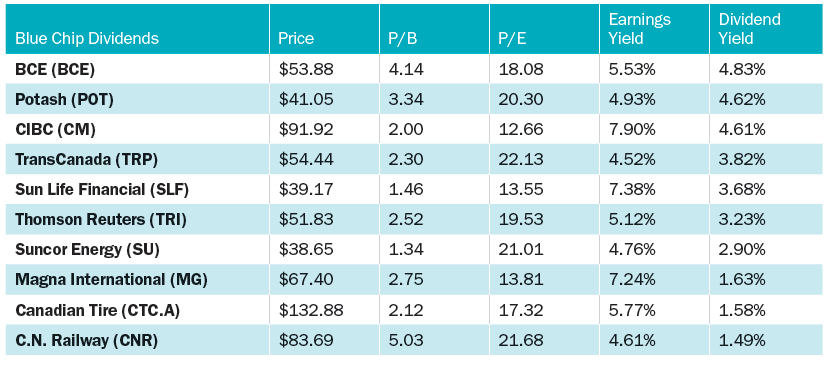

That said, the current list of Dogs is heavily concentrated in financials and telecoms and I’d personally want to begin with a little more diversification by industry. To help start you off, the table “Ten stocks to start out with” on page 41 shows a selection of high-yielding stocks in the S&P/TSX 60 that come from different industry groups.

There are pros and cons for both stock picking and index investing, but no matter which you choose, it’s best to stick with simple and easy to understand low-fee methods. With a bit of luck, they’ll fund more than a few trips to your local coffee bar.

Ten stocks to start out with

Source: Bloomberg, April 2, 2015. (Norm Rothery may hold these securities.)

(Photograph by Jaime Hogge)

Jin Won Choi, 33, his wife Jennifer, 35, and 7-month old Madeleine, London, Ont.

Stocks for the long run

Jin Won Choi and his wife Jennifer first started investing in stocks seven years ago and they’ve never looked back. Today, the entire equity portion of their portfolio is invested in individual stocks and Jin says they’ve enjoyed at 20% average annual return on their stocks since 2008. The London, Ont., couple, who had their first child, Madeleine, seven months ago, has 30% of their portfolio in fixed income (“that’s our safety net,” says Jin), 40% in oil and gas stocks (“because they’re cheap and I’m going to hold on for the long term”) and the remaining 30% in bank, technology and retail stocks. The couple’s goal is to live off the income from their investments in a few years, “but for now, we’re happy to just keep building both our portfolio—and our family,” Jin says.

Beating index funds with stocks

Beating index funds with stocks I don’t suggest adopting the trust’s current portfolio, but new stock pickers should emulate its philosophy.

If you’re keen on giving it a go, focus your efforts first on the Canadian stock market. While Americans have thousands of large stocks to choose from, there are only a few dozen big companies that trade on the TSX. For instance, you could replace a part of the Canadian component of your Couch Potato portfolio with, say, 20 Canadian dividend payers.

One way to build a buy-and-hold dividend portfolio is to get a few ideas from the Dogs of the TSX method I highlight in my Value Hunter blog at MoneySense.ca. The strategy involves buying the 10 highest-yielding stocks in the large-cap S&P/TSX 60 index, holding them for a year, and then moving into a new group of high yielders.

However, a very passive portfolio can be built by holding on to the stocks indefinitely and adding any new stocks that appear on the Dogs list each year. If you do so, it should be possible to build a reasonably diversified list of 20 dividend-paying stocks in just a few years.

That said, the current list of Dogs is heavily concentrated in financials and telecoms and I’d personally want to begin with a little more diversification by industry. To help start you off, the table “Ten stocks to start out with” on page 41 shows a selection of high-yielding stocks in the S&P/TSX 60 that come from different industry groups.

There are pros and cons for both stock picking and index investing, but no matter which you choose, it’s best to stick with simple and easy to understand low-fee methods. With a bit of luck, they’ll fund more than a few trips to your local coffee bar.

I don’t suggest adopting the trust’s current portfolio, but new stock pickers should emulate its philosophy.

If you’re keen on giving it a go, focus your efforts first on the Canadian stock market. While Americans have thousands of large stocks to choose from, there are only a few dozen big companies that trade on the TSX. For instance, you could replace a part of the Canadian component of your Couch Potato portfolio with, say, 20 Canadian dividend payers.

One way to build a buy-and-hold dividend portfolio is to get a few ideas from the Dogs of the TSX method I highlight in my Value Hunter blog at MoneySense.ca. The strategy involves buying the 10 highest-yielding stocks in the large-cap S&P/TSX 60 index, holding them for a year, and then moving into a new group of high yielders.

However, a very passive portfolio can be built by holding on to the stocks indefinitely and adding any new stocks that appear on the Dogs list each year. If you do so, it should be possible to build a reasonably diversified list of 20 dividend-paying stocks in just a few years.

That said, the current list of Dogs is heavily concentrated in financials and telecoms and I’d personally want to begin with a little more diversification by industry. To help start you off, the table “Ten stocks to start out with” on page 41 shows a selection of high-yielding stocks in the S&P/TSX 60 that come from different industry groups.

There are pros and cons for both stock picking and index investing, but no matter which you choose, it’s best to stick with simple and easy to understand low-fee methods. With a bit of luck, they’ll fund more than a few trips to your local coffee bar.