A perfect portfolio to retire on

This balanced portfolio provides better returns and income, with less risk

Advertisement

This balanced portfolio provides better returns and income, with less risk

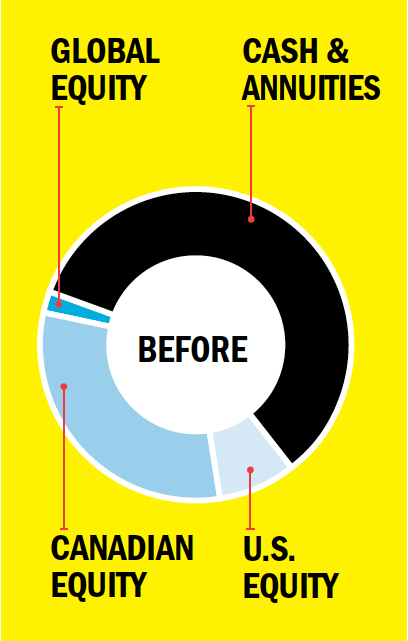

David Barton, a 68-year-old real estate agent, plans to join his wife Doreen, 62, in retirement by 2016. Decades of toil has netted the Winnipeg couple a large, six-figure nest egg, 60% of which is safeguarded in annuities and cash. The remaining 40% of their portfolio is mainly comprised of Canadian dividend-paying stocks—many of them oil and gas—as well as a couple of mutual funds. However, now the Bartons are concerned they’re not properly diversified. “We’ve set aside an additional $75,000 to cover expenses for three years if the market goes south,” says David. “But I’d like more U.S. holdings—maybe in ETFs.”

David Barton, a 68-year-old real estate agent, plans to join his wife Doreen, 62, in retirement by 2016. Decades of toil has netted the Winnipeg couple a large, six-figure nest egg, 60% of which is safeguarded in annuities and cash. The remaining 40% of their portfolio is mainly comprised of Canadian dividend-paying stocks—many of them oil and gas—as well as a couple of mutual funds. However, now the Bartons are concerned they’re not properly diversified. “We’ve set aside an additional $75,000 to cover expenses for three years if the market goes south,” says David. “But I’d like more U.S. holdings—maybe in ETFs.”

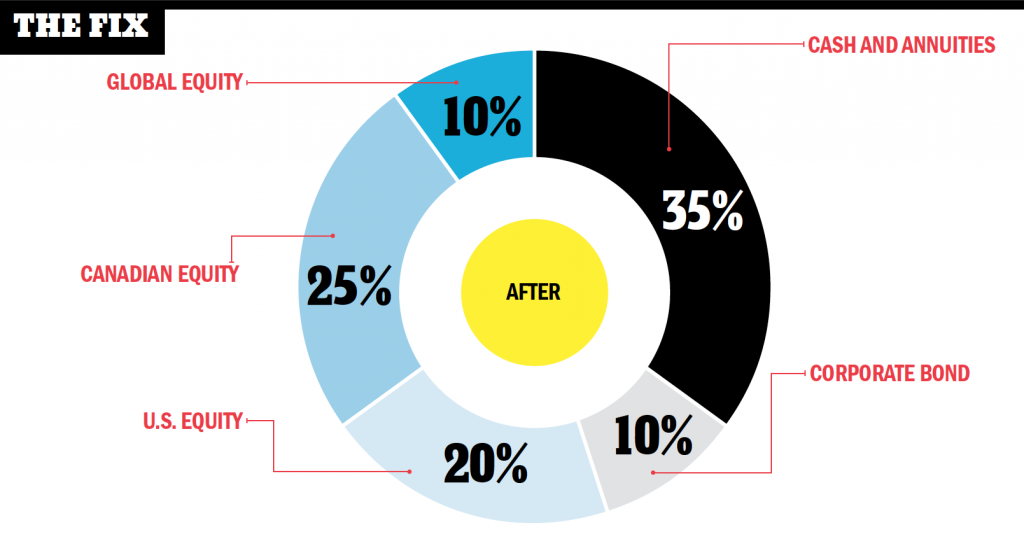

Senior investment adviser Allan Small, of the Allan Small Financial Group with HollisWealth, agrees the Bartons need a more balanced approach. He wants the couple to keep their sizable annuities and $75,000 emergency fund, and use the remaining cash to increase the equity exposure of their portfolio to 55%. Part of this strategy will also involve ditching their pricey mutual funds and building the right mix out of individual high-yield stocks. “That will give them great growth and income for life,” says Small, adding that their portfolio is big enough that they don’t need too many ETFs or mutual funds to get a good mix. “Staying clear of them will keep their costs very low.”

In addition to cashing in their mutual funds, Small wants the Bartons to sell off a third of their Canadian dividend-paying stocks—mainly the telecom, and oil and gas holdings—and keep just three: TransCanada Corp., Enbridge and Interpipeline, since they have a history of increasing dividends. They should also increase their Canadian bank holdings, bringing their total Canadian equity portfolio holdings to 25%.

At the same time, the couple’s U.S. stock holdings should be increased to 20% of their portfolio. In total, they will be holding about 15 individual stocks, with a 10% holding in a low-cost global mutual fund rounding out their equity holdings, and a 10% holding in a corporate bond filling out their fixed income allocation. “This new portfolio gives them more diversification as well as less risk.”

Do you want a portfolio makeover from MoneySense? If so, send an email describing your situation to [email protected]

Senior investment adviser Allan Small, of the Allan Small Financial Group with HollisWealth, agrees the Bartons need a more balanced approach. He wants the couple to keep their sizable annuities and $75,000 emergency fund, and use the remaining cash to increase the equity exposure of their portfolio to 55%. Part of this strategy will also involve ditching their pricey mutual funds and building the right mix out of individual high-yield stocks. “That will give them great growth and income for life,” says Small, adding that their portfolio is big enough that they don’t need too many ETFs or mutual funds to get a good mix. “Staying clear of them will keep their costs very low.”

In addition to cashing in their mutual funds, Small wants the Bartons to sell off a third of their Canadian dividend-paying stocks—mainly the telecom, and oil and gas holdings—and keep just three: TransCanada Corp., Enbridge and Interpipeline, since they have a history of increasing dividends. They should also increase their Canadian bank holdings, bringing their total Canadian equity portfolio holdings to 25%.

At the same time, the couple’s U.S. stock holdings should be increased to 20% of their portfolio. In total, they will be holding about 15 individual stocks, with a 10% holding in a low-cost global mutual fund rounding out their equity holdings, and a 10% holding in a corporate bond filling out their fixed income allocation. “This new portfolio gives them more diversification as well as less risk.”

Do you want a portfolio makeover from MoneySense? If so, send an email describing your situation to [email protected]

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email