Investing for the future without a pension plan

Rose's conservatism is holding her back.

Advertisement

Rose's conservatism is holding her back.

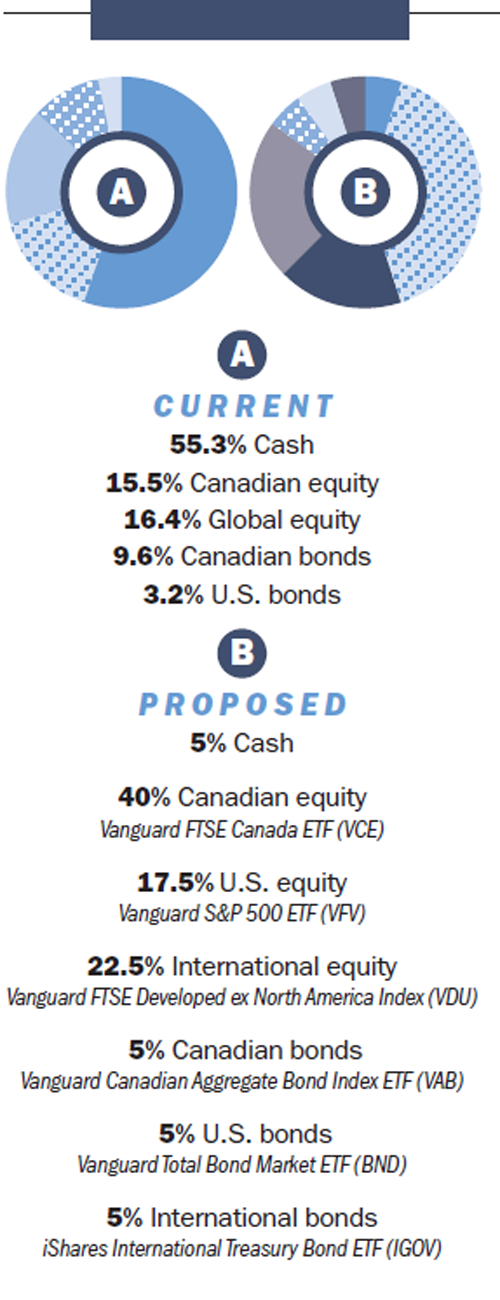

The Solution

The SolutionShare this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email