Is pet insurance worth it in Canada?

To determine if pet insurance is worth it, take a look at the current costs of pet care in Canada and consider how much you have saved for visits to the vet.

Advertisement

To determine if pet insurance is worth it, take a look at the current costs of pet care in Canada and consider how much you have saved for visits to the vet.

When your budget is tight, it’s only natural to wonder if adding a pet insurance premium to your list of expenses is worth it. While it might make sense for some pet owners, others might do better by focusing on saving for pet expenses with a high-interest yield account.

We’ll walk you through the current landscape of pet insurance and discuss current premium costs to help you decide if purchasing a policy makes sense for your pet and your wallet.

Watch: Is pet insurance worth it?Pet insurance is similar to health insurance, but it’s for your pet. Just like with a health insurance policy, you’ll pay a monthly fee, called a premium, to keep the policy active so your furry friend is covered.

If your pet needs medical care, you’ll take them to the vet as usual. As long as the reason for the visit is covered by your insurance policy, you’ll pay only your deductible and any co-pay, and the insurance provider will cover the rest (or pay up to the coverage limit).

Some conditions may be excluded—pet insurance doesn’t usually cover pre-existing conditions, older pets, specific breeds, or alternative methods of treatment. It also doesn’t typically cover preventative care and dental work unless you purchase a wellness add-on.

Before making any decision that will impact your finances, it’s wise to consider the benefits and drawbacks.

| Pros | Cons |

|---|---|

| Financial peace of mind as veterinary costs continue to rise | Hard to find coverage for an older pet or one with a pre-existing condition |

| More affordable the younger your pet is | Typically have to pay for care upfront before being reimbursed by insurance |

| May allow you to afford treatments that would otherwise be out of reach | Coverage can vary, so read policy documents closely |

| Easier to budget for your pet’s care | May end up paying more in premiums than you receive for care |

| Premiums increase over time (typically annually) |

Several factors determine how much you could pay each month for pet insurance, including your pet’s breed, location, age, and medical history. Plus, there are factors you can control, such as the deductible, annual limit on coverage, and what percentage of costs your insurer reimburses.

Keep in mind that as your pet ages, the cost of caring for and insuring it increases. Some insurance companies even set a maximum age limit on coverage, so enrolling your pet while it’s young and healthy could unlock more affordable rates.

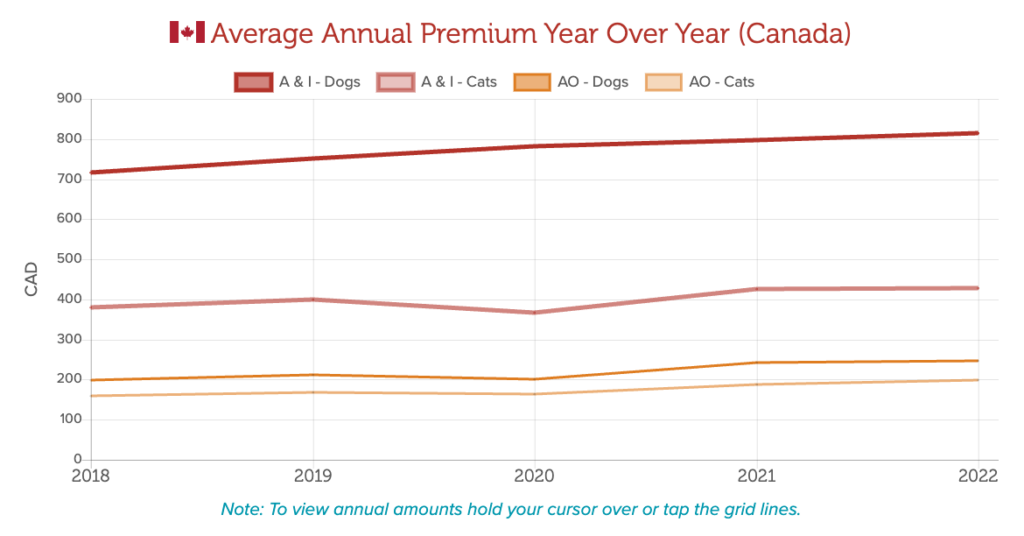

According to data from the North American Pet Health Insurance Association (NAPHIA), in 2024, the average monthly premiums in Canada were:

The more coverage and benefits you get, the higher the price tag. For this reason, it’s important to consider the pros and cons to decide whether purchasing insurance is worthwhile for you.

The cost of pet insurance has risen steadily over the past decade or so. The average annual increase for accident and illness insurance was 6.5% for dog owners and 15.24% for cat owners.

Inflation, increased wages of veterinary staff, and higher medical costs have all contributed to the rise in pet insurance premiums since the pandemic; however, higher costs are also tied to advancements in the medical care that pets receive. Vet clinics are increasingly able to treat life-threatening conditions like cancer and other diseases, but it can be expensive.

Before deciding whether or not to get insurance, pet owners must weigh the possibility of paying thousands of dollars out-of-pocket for medical procedures vs. paying ongoing monthly premiums.

There are several strategies you can use to keep pet insurance costs low:

Shop around and compare policies. Insurers each have unique offerings and calculate premiums differently. Get multiple quotes to find the most affordable rate, but be sure you’re comparing similar coverages.

Choose a higher deductible. The higher your deductible, the lower your premium will be. That said, be sure you choose a deductible amount that you can afford to pay at a moment’s notice if your pet requires urgent care.

Choose a lower annual limit. This is the maximum amount of money your pet insurance company will pay out to you every year. Once you’ve reached that threshold, you’ll be on the hook for any additional veterinary costs.

Ask about discounts. If you have multiple pets, it’s worth asking if you can get a discount from your provider for insuring them both (or all). Typically, you have to enroll each pet and pay separate premiums.

Like any insurance product, the value of pet insurance largely depends on your unique situation. If you’re unsure whether or not you should spring for a pet insurance policy, see if any of these situations describe you and your pet.

Pet insurance might be worth it if…

Pet insurance may not be worth it if…

If you’re still undecided, think about getting accident-only coverage, which works like emergency insurance.

If you don’t want pet insurance or it doesn’t fit into your budget but need a backup plan, here are some other options to consider:

As a pet parent, you don’t ever want to face a financial barrier when it comes to getting quality care for your pet. Be sure to research all the options so you are aware of what’s available to you.

The cost of pet insurance can be steep, which prevents many people from purchasing coverage. And, if you do have pet insurance, you’ll typically have to pay for care upfront and get reimbursed after your claim is approved. Unless you have a wellness add-on, insurance won’t typically cover routine check-ups and procedures, like vaccines and dental care.

Costco offers pet insurance through Pets Plus Us, but the coverage is limited. General checkups and dentistry are not covered, and coverage limits are on the low side. When we turned to Reddit to learn more, we found mixed opinions, with many people saying coverage was dropped or claims were denied.

Yes, your pet insurance provider can deny coverage if your pet has a pre-existing condition or has reached a maximum age for coverage. Treatments like alternative therapies are also often excluded. Be sure to read your policy terms carefully so you understand what is covered.

Your insurance provider may raise your premium after you file a claim. With this in mind, you may not want to claim small, inexpensive visits since they could cost more in the form of higher monthly costs. In general, insurance is best used to cover expensive emergencies, such as surgery or treatment for a serious illness.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

More Canadians are exploring alternatives to the Big Six. Learn what to compare before switching banks and how to...

Whether a U.S.-listed ETF is worth buying depends on foreign exchange costs, taxes, MERs, and your investment account.

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Artificial intelligence is transforming markets, but retirees should approach the AI investing theme with caution and a well-diversified portfolio.

Rising temperatures can mean higher electricity bills. Experts share simple ways Canadians can stay cool while using less energy.

The pursuit of the perfect financial decision has quietly become one of the biggest obstacles to making any decision...

Cogeco reports a steep quarterly loss tied to its U.S. business, while Electrovaya jumps on an Amazon agreement and...

The biggest financial barrier for newcomers isn't always knowledge, but understanding how familiar words take on new meanings...

Financial principles can be timeless, but the tactics behind them often aren't. Here's why some money advice deserves a...

My pet insurance has gone up 34% since enrolling my dog. This is now not worth it in my mind. Putting money in a HISA can defray the costs I would have paid the insurer.