Making sense of the markets this week: July 30, 2023

Big tech still “magnificent” as telecoms disappoint, credit card giants trounce crypto and economic pessimists, U.S. Fed hike is taken in stride, and railways struggle.

Advertisement

Big tech still “magnificent” as telecoms disappoint, credit card giants trounce crypto and economic pessimists, U.S. Fed hike is taken in stride, and railways struggle.

Kyle Prevost, editor of Million Dollar Journey and founder of the Canadian Financial Summit, shares financial headlines and offers context for Canadian investors.

The U.S. tech earnings machine keeps on humming. While Microsoft did lower its guidance for the rest of the year, all three tech giants outperformed expectations again this quarter. When juxtaposed against the year-to-date performance of not-so-trusty old telecommunications firms at Verizon and AT&T, the comparison is rather stark. (All numbers below are presented in U.S. dollars.)

Before you run off to implement a tech-only investment strategy, remember that this year’s gains are already now baked into the share prices. Just because tech-stock momentum has only moved in one direction, it doesn’t mean share prices will keep rising. All of these tech companies will continue to make gobs of money, but the current sky-high valuations assume that not only will they remain incredibly profitable, but that those profits will increase from here.

That said, right now, I’d rather own The Magnificent Seven over AT&T or Verizon. The Economist recently reported on what the future might hold for AT&T and Verizon. It turns out that high interest rates, lawsuits about widely used, lead-encased cables, and stagnating new subscriber numbers, aren’t exactly what investor dreams are made of.

The U.S. Federal Reserve executed the widely anticipated 0.25% rate hike on Wednesday, taking the U.S.A.’s benchmark borrowing rate range from 5.25% to 5.50%.

In what has now become market watchers’ confusing monthly ritual, speculators tried to parse U.S. Fed chair Jerome Powell’s comments. Here’s some noteworthy quotes from his lengthy speech:

Markets initially reacted positively to the phrase “hold steady,” but they were basically flat that day, as there was little unexpected in Powell’s comments. In related news, we’re not the only ones beginning to seriously question whether we’re now going overboard on these rate hikes.

All numbers below are presented in U.S. dollars.

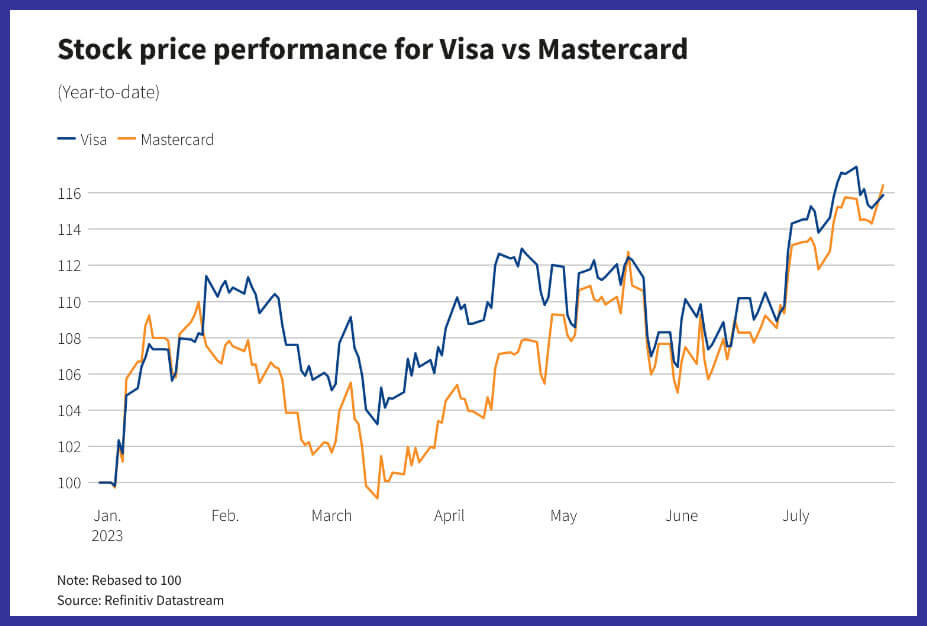

From the Visa front, chief financial officer Vasant Prabhu said, “The consumer is resilient and stable, [and] the travel recovery still has legs. We’re nowhere near the end of it.” And Mastercard’s chief executive officer Michael Miebach said, “Our positive momentum continued this quarter. We delivered strong revenue and earnings growth supported by resilient consumer spending, particularly in travel and experiences, and the continued strength in services. Cross-border travel volume showed strong growth again this quarter, reaching 154% of pre-pandemic levels.”

It’s pretty tough to worry too much about a recession when your credit card management teams are almost giddy about all the spending!

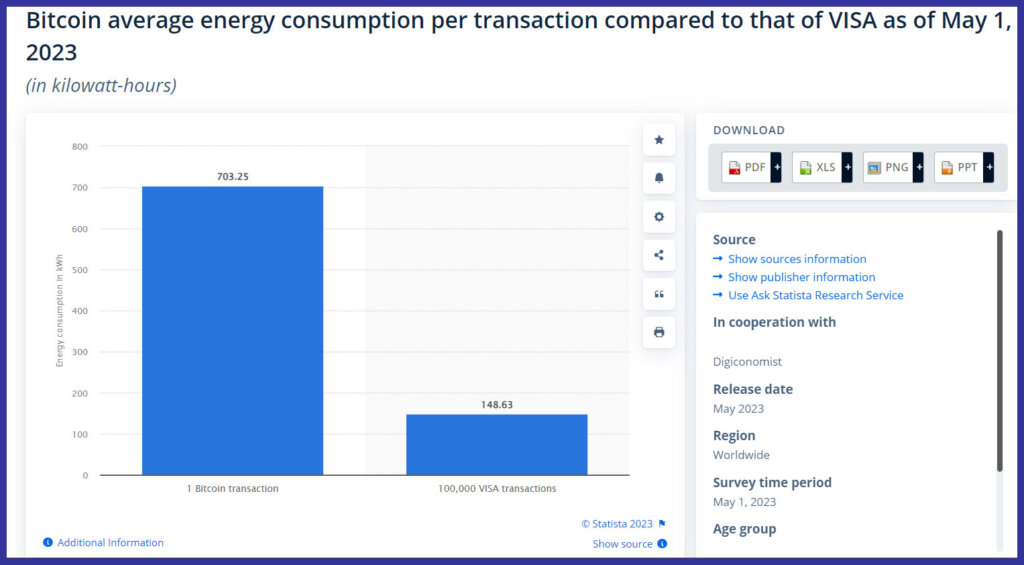

Because Mastercard and Visa are so ever-present in many of our lives, their consistent revenues and solid business fundamentals can, at times, fade into the background. As a quick reminder of just how impressive these credit companies are when it comes to supplying the lubricating transaction speed that allows our economic machinery to function, it might help to compare it to the blockchain technology darlings that will supposedly replace it.

To sum things up: Visa processes transactions about 3,400 times more quickly than Bitcoin, and it uses far less than 0.01% of the energy to do so. Clearly, the old guard is doing much better in payment processing than their old-school peers in communications over at Verizon and AT&T.

While all of what CP revealed may be true, and eventual predictions of increased value may well come to pass, this quarter the company suffered from the same issues that plagued CNR. Earnings per share came in at $0.83 (versus $0.93 predicted) and revenues were $3.20 billion (versus $3.24 billion predicted).

Creel did go on to say optimistically, “This is about the long game, it’s not about the first quarter of a new company.” Shareholders appeared to mostly agree as share prices were down less than 1% on Thursday. (For more information, check out our article on Canada’s railway stocks at MillionDollarJourney.com.)

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Financial principles can be timeless, but the tactics behind them often aren't. Here's why some money advice deserves a...

Building wealth as a couple takes more than smart investing. Here's why open communication about money is essential...

Why and how ETF closures happen, which warning signs to watch for, and what it means if a fund...

Nobody moves to Canada excited about price matching. When my family immigrated in 2019, I expected to spend countless...

Sponsored By

Equifax

Canada's top finfluencers share how they built trust, grew audiences and navigate increasing regulatory scrutiny in a rapidly maturing...

Bonds are considered safer than stocks, but higher interest rates can still lead to losses. Here's what investors need...

Incorporating can eliminate the need to pay CPP contributions if you are self-employed but there are trade-offs that should...