How your credit score works

What's measured, how to read it and what it will cost you.

Advertisement

What's measured, how to read it and what it will cost you.

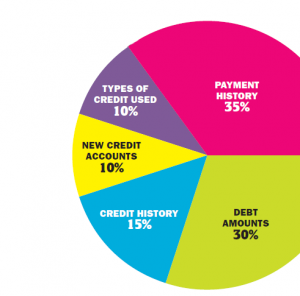

The FICO score, the basis for most credit scores, consists of five major categories based on data in your credit report. The percentages in the chart reflect how important each of the categories is in determining how your FICO score is calculated. The biggest factors are how much debt you have, whether you’ve paid your bills on time and how long your credit history is. You may also be penalized if you don’t have a good mix of types of credit and if you’ve opened too many new accounts recently.

The FICO score, the basis for most credit scores, consists of five major categories based on data in your credit report. The percentages in the chart reflect how important each of the categories is in determining how your FICO score is calculated. The biggest factors are how much debt you have, whether you’ve paid your bills on time and how long your credit history is. You may also be penalized if you don’t have a good mix of types of credit and if you’ve opened too many new accounts recently.

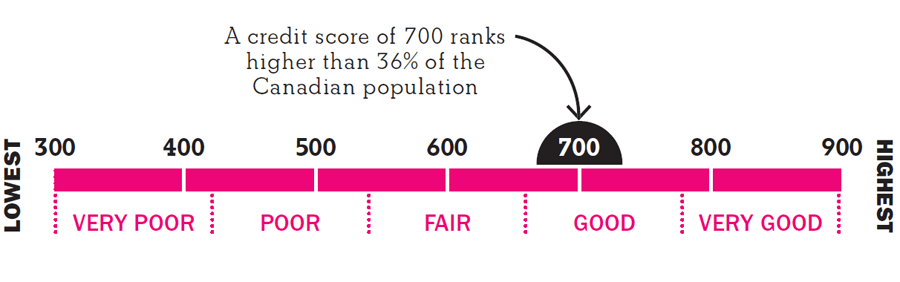

Your credit score rates creditworthiness out of a possible 900 points, and compares your credit standing to that of other Canadians. Lenders generally consider you a good credit risk if your score falls between 660 and 724. Anything below 560 is poor.

Your credit score rates creditworthiness out of a possible 900 points, and compares your credit standing to that of other Canadians. Lenders generally consider you a good credit risk if your score falls between 660 and 724. Anything below 560 is poor.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Navigating student financial aid in Canada? Learn how loans, grants, scholarships, and private options can help pay for post-secondary...

Disabled students in Canada face higher costs for postsecondary education. Here’s a guide to grants, scholarships, and supports that...

Canada is built around borrowing, credit scores, and financing. For many newcomers, adapting to that system can feel overwhelming.

Placing a few bets during the World Cup may feel low-stakes, but experts say it’s easy to lose track...

A new study shows that 41% of Canadians believe bankruptcy is a moral failing, at a time when insolvencies...

As side hustles become more popular, Canadians are looking for bank accounts that can help them track their income,...

Bank of Canada holds its 2.25% rate for a fourth time amid inflation risks from oil prices, affecting mortgages,...

Most Canadian parents are saving for their child’s education, but few feel confident it will be enough. Here’s why...

Canadians appear to be managing economic pressures overall, but deeper data and lender results reveal growing pockets of credit...