Are you lying to yourself about debt?

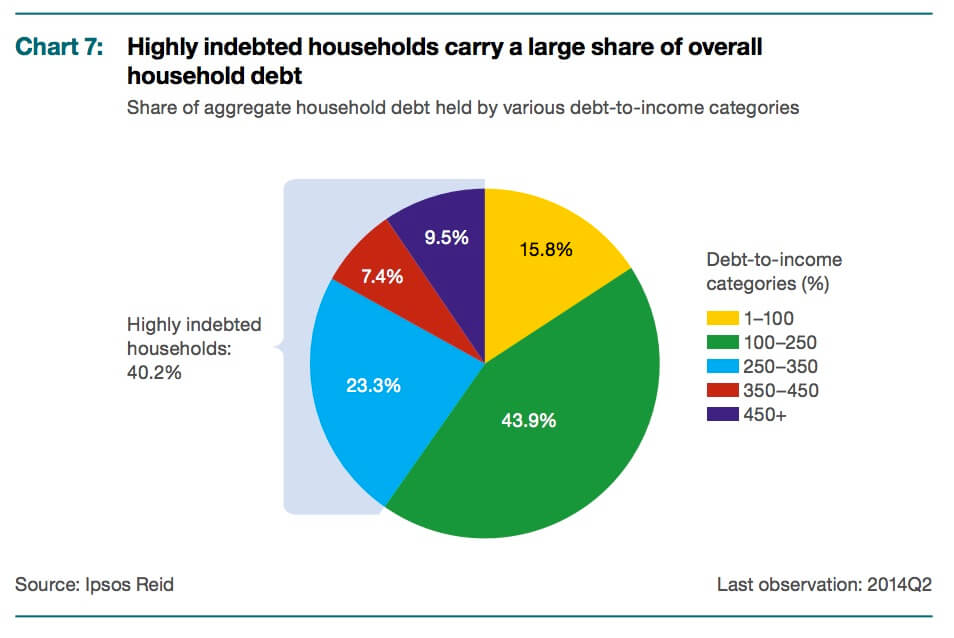

It’s clear Canadians are caught in a debt trap

Advertisement

It’s clear Canadians are caught in a debt trap

The recent jump in the household debt-to-income ratio also came before Bank of Canada Governor Stephen Poloz surprised everyone by cutting the overnight rate to 0.75 per cent from one per cent, where it had lingered since 2010. That’s almost certain to spur additional borrowing, and if incomes continue to stall out, the household imbalance is likely to break new records in the quarters ahead.

It’s clear Canadians are caught in a debt trap. The more they talk about digging themselves out, the deeper they sink.

This article originally appeared on Maclean’s.

The recent jump in the household debt-to-income ratio also came before Bank of Canada Governor Stephen Poloz surprised everyone by cutting the overnight rate to 0.75 per cent from one per cent, where it had lingered since 2010. That’s almost certain to spur additional borrowing, and if incomes continue to stall out, the household imbalance is likely to break new records in the quarters ahead.

It’s clear Canadians are caught in a debt trap. The more they talk about digging themselves out, the deeper they sink.

This article originally appeared on Maclean’s.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Created By

Ratehub

We’ve put together all the tools and strategies you need to manage the shock of renewing your home loan...

Wealthsimple is flexing against Canada’s big banks. Here’s how it plans to get your business.

Created By

Ratehub.ca

The Bank of Canada held its key rate at 2.75%, citing high uncertainty, tariffs and more.

Sponsored By

Coast Capital

From rent to hair styling, phone to internet plans, these expenses are surprisingly negotiable. How every young Canadian can...

If spiralling debt has you on the brink, a consumer proposal may be the right move. Here’s how it...

Helping a grandchild pay for post-secondary education is a smart gift that keeps giving. Here’s how to maximize your...