RRSP vs. TFSA: Which is right for you?

Are you a middle income earner? It's a coin toss

Advertisement

Are you a middle income earner? It's a coin toss

*Update: As of January 1, 2016, the TFSA limit has decreased from $10,000 to $5,500

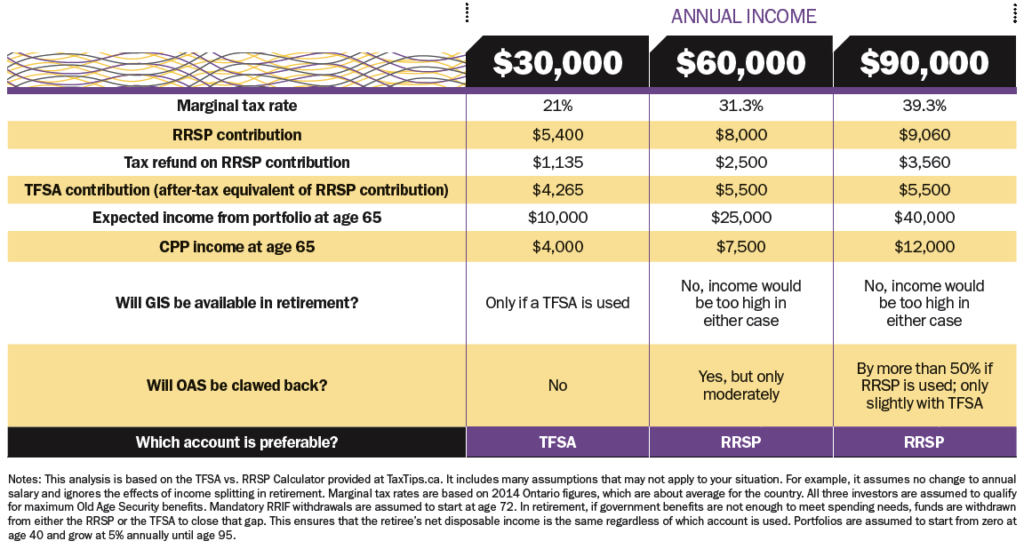

Not sure whether to use an RRSP or TFSA for your retirement savings? That’s a common question. In general, those earning a low income (under $35,000 or so) should favour the TFSA, while high-income earners are likely to be better off with an RRSP. For those earning a moderate income, however, it’s a coin flip.

The table below illustrates this idea for three 40-year-old investors at different income levels. Someone earning $30,000 and expecting to withdraw $10,000 annually after age 65 is in danger of losing the Guaranteed Income Supplement if he or she uses an RRSP. At the other end of the spectrum, a high-income earner may see significant Old Age Security clawbacks from RRIF withdrawals, but would still be better off with an RRSP because that would be more than offset by the greater tax savings when contributions are made.

Remember, this illustration only helps you decide which contribution to make with your first $5,500 of after-tax savings. If you can save more than that and you’re in a middle-income bracket—where the differences between the two accounts are modest—you could max out your TFSA and put the rest in your RRSP. And if you’re a high income earner maxing out your RRSP, use a TFSA for additional savings.

There are a few circumstances when it makes sense to avoid RRSPs.

1. You expect to be in a higher tax bracket in retirement.

If you expect to earn a generous pension, the combined income from your pensions and your RRSP or RRIF withdrawals in retirement could drive you into a higher tax bracket than when you working.

2. You earn a low income.

If you earn less than $35,000 annually you should forgo RRSPs altogether, says pension expert Malcolm Hamilton. In retirement, withdrawals from RRSPs and RRIFs can lead to clawbacks of Old Age Security and other government programs like the Guaranteed Income Supplement. “The lower your income, the more likely you’ll be a recipient of these government income-tested benefits in retirement. You don’t want to mess with that,” says Hamilton.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

RBC Direct Investing has introduced commission-free trades on 50 exchange-traded funds (ETFs) from partner iShares.

The latest earnings reports for Canadian investors from the cybersecurity and convenience-store giants.

Here’s why mutual funds don’t travel well across international borders—and what Canadian investors can do instead.

Most registered retirement savings plans are eventually converted to registered retirement income funds. Here’s what to know about RRIF...

Good news for Canadian investors in these apparel and grocery companies, as both report higher earnings and sales.

Retirement Club for Canadians offers a sounding board and resources for people who manage retirement finance all on their...

Dollarama reports increases in profits and sales, Transat deals with Canadian travellers avoiding the U.S., and Roots sees Q1...

This Toronto-based fintech continues to attract Canadian investors with its low-fee robo-advisor, discount brokerage and money management services.

Canada’s original asset-allocation ETF is still a good all-in-one investment, but it can have its flaws. Here are add-ons...