How much money will you need to retire?

We've calculated the nest egg you’ll need for different levels of income

Advertisement

We've calculated the nest egg you’ll need for different levels of income

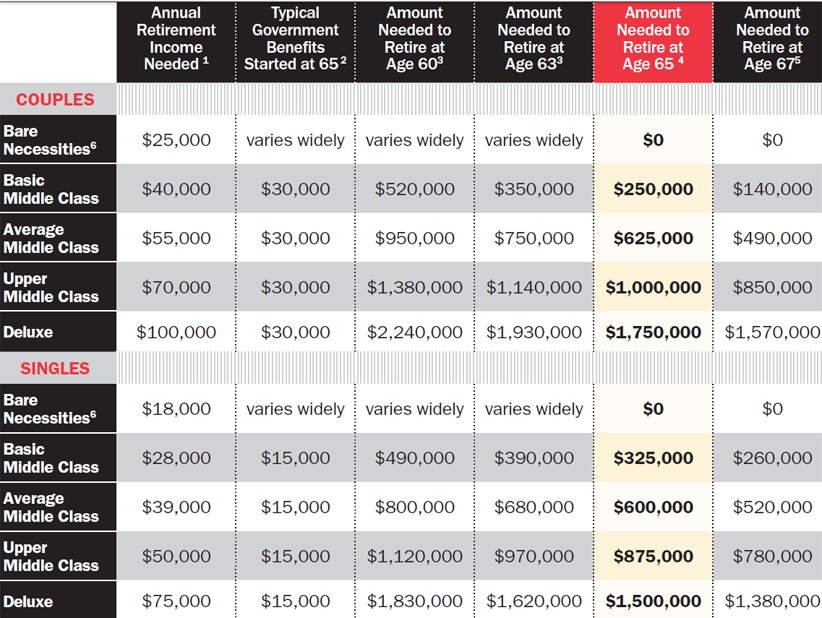

Notes: (1) Retirement income is before tax. Assumes no debt in retirement and for all categories except Bare Necessities, a paid-for home. (2) Typical amount for OAS and CPP based on fairly long work career at average wages or better. Assumes OAS started at 65. People born after March 1958 will start OAS later and need to adjust calculations. Figures shown assume no employer pension (although employer pension income can be added to this column if applicable.) (3) Assumes initial withdrawal rate of 3.5% for retirement at 60 and 3.8% for retirement at 63, plus inflation. Adjustments also made for starting CPP at early retirement date and for bridging OAS equivalent until OAS start date. (4) Calculated by taking (annual retirement income minus government benefits) x 25. This assumes a withdrawal rate of 4% of initial portfolio plus inflation. (5) Withdrawal rate 4.2% of initial portfolio plus inflation adjustments. Adjusted for OAS and CPP start at 67. (6) Retirement income necessary for “Bare Necessities” derived from Basic Living Expenses for the Canadian Elderly by Bonnie-Jeanne MacDonald, Doug Andrews and Robert Brown, based on typical basic senior’s living expenses averaged for five Canadian cities. Amounts in study adjusted for inflation using Statistics Canada Consumer Price Index. Government benefits in this case comprised of CPP, OAS, and the Guaranteed Income Supplement and vary widely but ensure roughly that necessities at least are covered. People born after March 1958 have to wait longer than age 65 to collect OAS and GIS.

Read the full article, “What’s your magic number?”

Notes: (1) Retirement income is before tax. Assumes no debt in retirement and for all categories except Bare Necessities, a paid-for home. (2) Typical amount for OAS and CPP based on fairly long work career at average wages or better. Assumes OAS started at 65. People born after March 1958 will start OAS later and need to adjust calculations. Figures shown assume no employer pension (although employer pension income can be added to this column if applicable.) (3) Assumes initial withdrawal rate of 3.5% for retirement at 60 and 3.8% for retirement at 63, plus inflation. Adjustments also made for starting CPP at early retirement date and for bridging OAS equivalent until OAS start date. (4) Calculated by taking (annual retirement income minus government benefits) x 25. This assumes a withdrawal rate of 4% of initial portfolio plus inflation. (5) Withdrawal rate 4.2% of initial portfolio plus inflation adjustments. Adjusted for OAS and CPP start at 67. (6) Retirement income necessary for “Bare Necessities” derived from Basic Living Expenses for the Canadian Elderly by Bonnie-Jeanne MacDonald, Doug Andrews and Robert Brown, based on typical basic senior’s living expenses averaged for five Canadian cities. Amounts in study adjusted for inflation using Statistics Canada Consumer Price Index. Government benefits in this case comprised of CPP, OAS, and the Guaranteed Income Supplement and vary widely but ensure roughly that necessities at least are covered. People born after March 1958 have to wait longer than age 65 to collect OAS and GIS.

Read the full article, “What’s your magic number?”

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Artificial intelligence is best at overcoming the friction that stops you from taking up new pursuits, users insist.

Could moving your RRIF into segregated funds lower estate taxes? Maybe—but higher fees and other trade-offs could leave your...

Here’s how Canada’s Old Age Security pension works, who’s eligible for OAS, when you can start receiving benefits, and...

We check in on some champions of early retirement nearing their own finish line of financial independence.

What inflation, investment return, and life expectancy assumptions should Canadians use for retirement planning? Here’s what financial planners recommend.

The Saskatchewan Pension Plan gives Canadians another way to save for retirement, with low fees, locked-in contributions, and...

The FIRE movement promises early retirement, but high costs and income realities make it difficult. Here’s what the math...

Experts explore whether financial independence is compatible with long-term travel, highlighting remote work, geoarbitrage, and cost-efficient “bleisure” lifestyles.

Robert has been taking RRIF withdrawals beyond the minimum required amount to gift to his kids and to reinvest...