Bank of Canada optimistic but maintains rate

But global and domestic growth expected in 2016

Advertisement

But global and domestic growth expected in 2016

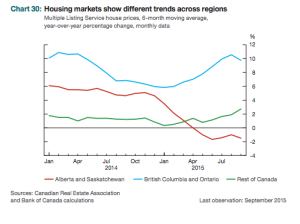

The BoC credits lower mortgage rates to the growing mortgage debt, especially in B.C. and Ontario. However, they also pointed out that these low rates are also contributing to “other forms of consumer” debt and spending. “As a result, the overall ratio of debt to disposable income has edged higher.”

Still the BoC is optimistic. Despite “weak activity in 2015, global economic growth is expected to strengthen over 2016-17.” This projected stabilization extends to the housing market and household debt levels—mainly because of the projected uptick in interest rates that analysts predict will come in as early as 2016. “Looking ahead, the housing market and household indebtedness are expected to stabilize over the projection period as the economy gains strength and household borrowing rates begin to normalize.”

The Bank of Canada is committed to examining the vulnerability associated with increasing household debt with a greater analysis scheduled for release in December 2015.

Already earlier this year the Bank of Canada lowered the overnight rate—which directly impacts variable mortgage rates—once in January and another in July, both times in an effort to stimulate the economy and offset some of the impact from a collapse in oil prices that began November 2014.

Read more from Romana King at Home Owner on Facebook »

The BoC credits lower mortgage rates to the growing mortgage debt, especially in B.C. and Ontario. However, they also pointed out that these low rates are also contributing to “other forms of consumer” debt and spending. “As a result, the overall ratio of debt to disposable income has edged higher.”

Still the BoC is optimistic. Despite “weak activity in 2015, global economic growth is expected to strengthen over 2016-17.” This projected stabilization extends to the housing market and household debt levels—mainly because of the projected uptick in interest rates that analysts predict will come in as early as 2016. “Looking ahead, the housing market and household indebtedness are expected to stabilize over the projection period as the economy gains strength and household borrowing rates begin to normalize.”

The Bank of Canada is committed to examining the vulnerability associated with increasing household debt with a greater analysis scheduled for release in December 2015.

Already earlier this year the Bank of Canada lowered the overnight rate—which directly impacts variable mortgage rates—once in January and another in July, both times in an effort to stimulate the economy and offset some of the impact from a collapse in oil prices that began November 2014.

Read more from Romana King at Home Owner on Facebook »

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Condo owners hoping to buy a house are stuck in a stalled market as sales in Canada continue to...

CMHC says rents in some major cities are easing due to increased supply and slower immigration, but renters are...

A MoneySense reader asks about survivor benefits for spouses. Here’s how defined benefit and CPP survivor payments work in...

Created By

Ratehub

If you’re thinking about buying your first recreational property, now may be the right time. Here's what to know.

We’ve put together all the tools and strategies you need to manage the shock of renewing your home loan...

If you’re worried about a recession in Canada, you’re not alone. Here’s what to expect and how you can...

Canadians accustomed to annual tax refunds may be surprised to owe tax in retirement and have government benefits clawed...

Want to buy a cottage but you’re priced out of the market? Co-ownership could be the answer. Here’s what...

First-time home buyers in Canada could save hundreds on monthly mortgage costs through the federal government’s plan to waive...