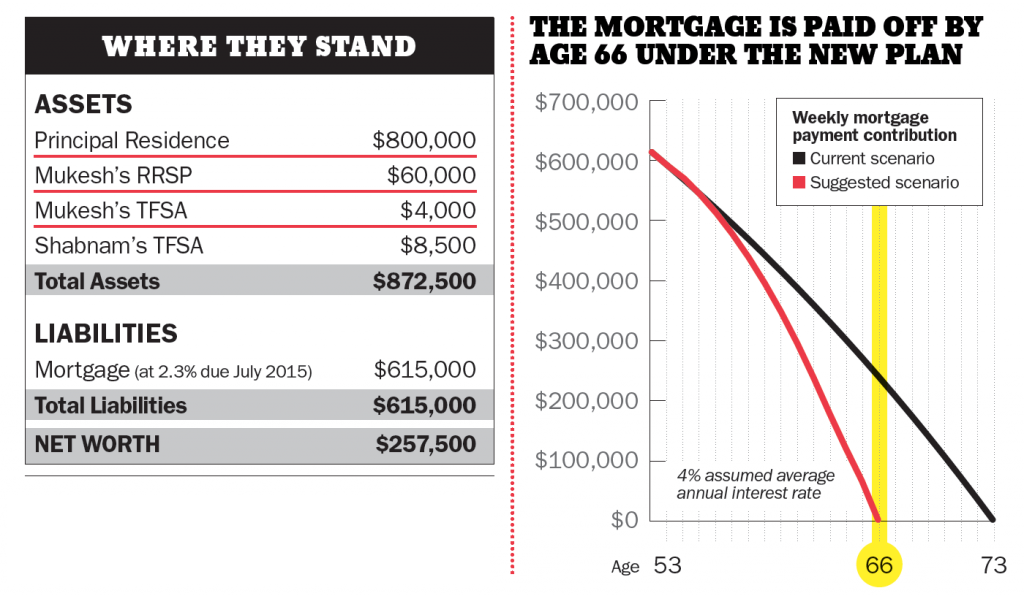

How to pay off the mortgage faster

This couple doesn't want to carry any debt into retirement

Advertisement

This couple doesn't want to carry any debt into retirement

Do you want MoneySense to see if you’re on track to meet your own financial goal? If so, drop us a line at [email protected],

Do you want MoneySense to see if you’re on track to meet your own financial goal? If so, drop us a line at [email protected],

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Created By

Ratehub

If you’re thinking about buying your first recreational property, now may be the right time. Here's what to know.

We’ve put together all the tools and strategies you need to manage the shock of renewing your home loan...

Created By

Ratehub.ca

Sponsored By

Coast Capital

You have so many options for finding the best mortgage rate for you. Here’s how you can compare some...

Sponsored By

Cambrian Credit Union

Canada’s central bank says the trade war is threatening progress on financial stability, creating higher risks and the potential...

Created By

Ratehub.ca