RRSP vs TFSA: Which should you top up in retirement?

The TFSA wins because it's flexible

Advertisement

The TFSA wins because it's flexible

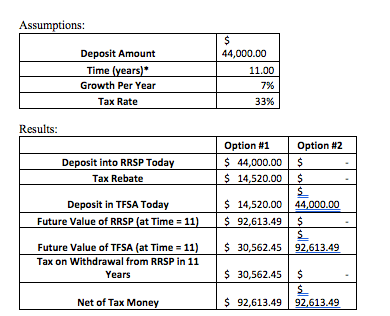

Q: I’m a 60-year-old retired school teacher as of this past July 2017. I have $44,000 in unused RRSP contribution room. Should I max out my contribution room on my 2017 taxes? Or just stick to topping up my TFSA?

—Chris

A: Hi Chris. Thanks for the question. Please note that RRSP only counts as a deduction against “earned income” which includes:

Q: I’m a 60-year-old retired school teacher as of this past July 2017. I have $44,000 in unused RRSP contribution room. Should I max out my contribution room on my 2017 taxes? Or just stick to topping up my TFSA?

—Chris

A: Hi Chris. Thanks for the question. Please note that RRSP only counts as a deduction against “earned income” which includes:

Conclusion: Both result in the same end value since you are facing a constant tax rate. Further, your RRSP must be converted upon your 71st birthday whereas you can leave your TFSA to grow for as long or short as you desire. Additionally, it is usually recommended to draw out of your RRSP rather than your TFSA earlier in retirement as your TFSA will incur no tax upon your passing or any withdrawals as compared to your RRSP which will be taxed fully.

What we can conclude is this. If your income will be staying constant throughout your retirement I would advise you to top up your TFSA rather than your RRSP for the following reasons

Conclusion: Both result in the same end value since you are facing a constant tax rate. Further, your RRSP must be converted upon your 71st birthday whereas you can leave your TFSA to grow for as long or short as you desire. Additionally, it is usually recommended to draw out of your RRSP rather than your TFSA earlier in retirement as your TFSA will incur no tax upon your passing or any withdrawals as compared to your RRSP which will be taxed fully.

What we can conclude is this. If your income will be staying constant throughout your retirement I would advise you to top up your TFSA rather than your RRSP for the following reasons

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Could moving your RRIF into segregated funds lower estate taxes? Maybe—but higher fees and other trade-offs could leave your...

Scenario-based planning can help you build a financial plan by testing “what ifs” and turning uncertainty into informed, realistic...

It’s almost impossible to do, but the mindset around spending all your savings can help you make the best of the...

Retirement planning for couples with a significant age difference calls for realistic projections but also flexibility.

Short answer: Yes. But to take advantage of this amazing tax shelter, you need to understand the CRA’s rules...

Many investors disparage bonds—with good reason. You have to determine what problems these investments solve and whether there are...

Under what circumstances can you obtain the greatest tax savings on this $2,000 credit?

Different retirement income strategies using registered accounts produce different outcomes. You must pick your priorities.

If you receive a severance package, you’ll have choices to make around your finances. Here’s how to make the...

While most Canadians will benefit from continuing to contribute until the day they retire, some will be better off...