How to pay for your kids’ education

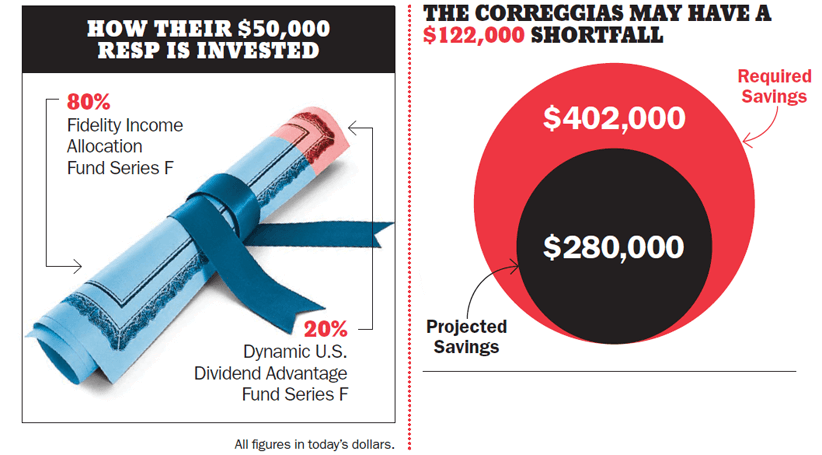

Achille and Heidi Correggia of Brantford, Ont. want to pay tuition for all their three kids. Are they saving enough?

Advertisement

Achille and Heidi Correggia of Brantford, Ont. want to pay tuition for all their three kids. Are they saving enough?

Do you want MoneySense to see if you’re on track to meet your own financial goal? If so, drop us a line at [email protected]

Do you want MoneySense to see if you’re on track to meet your own financial goal? If so, drop us a line at [email protected]

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Moving to the U.S. can change how an RESP works. CESG eligibility may stop, and U.S. tax rules can...

Most Canadian parents are saving for their child’s education, but few feel confident it will be enough. Here’s why...

Opening an RESP is a smart move—but how it’s set up can affect who controls the money, access to...

Find out which Canadian robo-advisors offer the lowest fees, helpful support, best returns, and most account types with the...

Your RRSP contribution limit comes from unused deduction room plus 18% of last year’s income. Use our RRSP calculator...

Despite rising costs and economic uncertainty, saving for your child’s education pays off in lifelong income, health, and opportunities.

A MoneySense reader asks what tax and probate implications she might face if she inherits a rental property held...

A MoneySense reader wants to give money to his spouse to invest. Can he avoid Canada’s income attribution rules?

A MoneySense reader wants input on the tax implications of her investment withdrawals, but she can’t get a straight...