There’s no return without risk

Raman Singh wants to be sure that his savings are still there when he goes to buy a home

Advertisement

Raman Singh wants to be sure that his savings are still there when he goes to buy a home

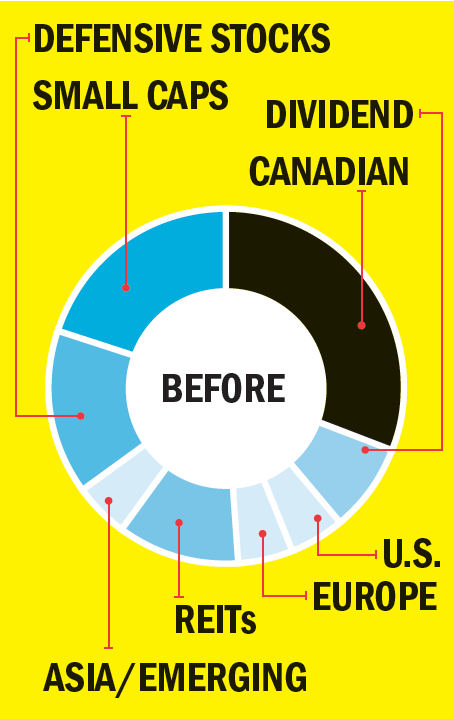

As a CFP with PWL Capital Inc., Shannon Dalziel comes across this situation often: money needed for short-term goals (less than three years) invested using an aggressive asset allocation. “Investing like this exposes the money to unnecessary risk,” says Dalziel. “This may prevent him from reaching his goal of home ownership in two years.” Dalziel suggests Singh save the riskier investments for his long-term retirement portfolio where time is on his side.

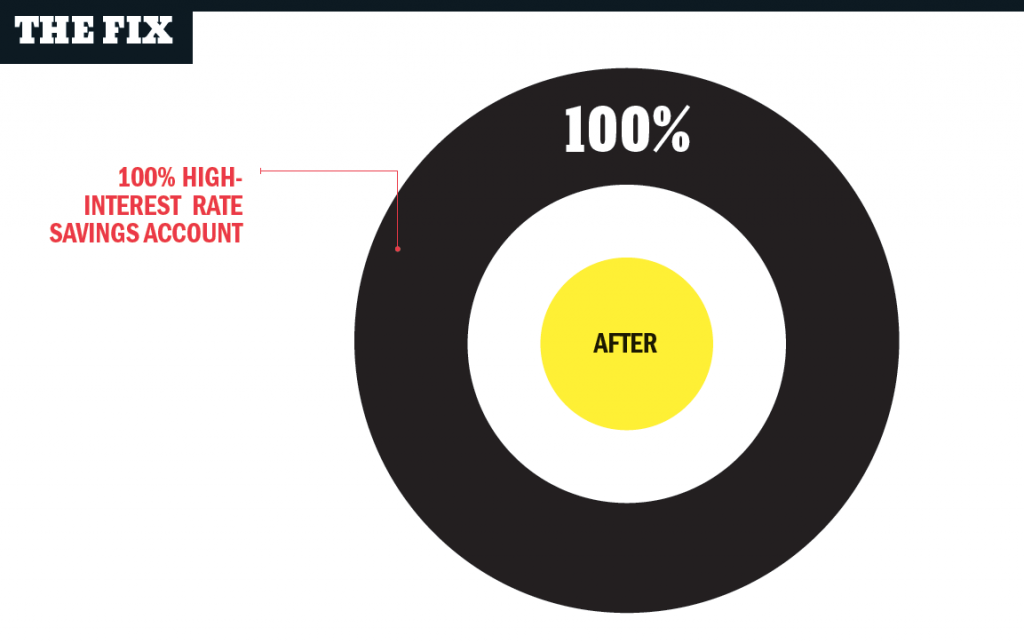

She recommends Singh sell the current investments earmarked for the home purchase and put the money in a high-interest rate savings account inside a Tax-Free Savings Account—a safe, conservative strategy for the short term. He should shop for the best interest rate and ensure the account is insured by the Canadian Deposit Insurance Corp. One option is the Oaken Financial savings account, which offers a competitive 1.75% rate (oaken.com/oaken-savings-account). With a simplified investment strategy in place, Singh can now focus on what he can control: his savings. “He should set up a monthly automatic plan that allows him to save with ease,” says Dalziel.

Since Singh plans to save $15,000 annually, he will reach his goal of a $40,000 house down payment in less than two years. “Once this goal is reached, and the money is safely set aside, Raman can look to invest his long-term retirement portfolio in a more aggressive asset allocation at low cost,” says Dalziel.

As a CFP with PWL Capital Inc., Shannon Dalziel comes across this situation often: money needed for short-term goals (less than three years) invested using an aggressive asset allocation. “Investing like this exposes the money to unnecessary risk,” says Dalziel. “This may prevent him from reaching his goal of home ownership in two years.” Dalziel suggests Singh save the riskier investments for his long-term retirement portfolio where time is on his side.

She recommends Singh sell the current investments earmarked for the home purchase and put the money in a high-interest rate savings account inside a Tax-Free Savings Account—a safe, conservative strategy for the short term. He should shop for the best interest rate and ensure the account is insured by the Canadian Deposit Insurance Corp. One option is the Oaken Financial savings account, which offers a competitive 1.75% rate (oaken.com/oaken-savings-account). With a simplified investment strategy in place, Singh can now focus on what he can control: his savings. “He should set up a monthly automatic plan that allows him to save with ease,” says Dalziel.

Since Singh plans to save $15,000 annually, he will reach his goal of a $40,000 house down payment in less than two years. “Once this goal is reached, and the money is safely set aside, Raman can look to invest his long-term retirement portfolio in a more aggressive asset allocation at low cost,” says Dalziel.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

A MoneySense reader asks what tax and probate implications she might face if she inherits a rental property held...

A MoneySense reader wants to give money to his spouse to invest. Can he avoid Canada’s income attribution rules?

A MoneySense reader wants input on the tax implications of her investment withdrawals, but she can’t get a straight...

RBC Direct Investing has introduced commission-free trades on 50 exchange-traded funds (ETFs) from partner iShares.

The latest earnings reports for Canadian investors from the cybersecurity and convenience-store giants.

The tax-free savings account is a great wealth-building tool, but it’s sadly misunderstood. Here are seven TFSA features Canadians...

Here’s why mutual funds don’t travel well across international borders—and what Canadian investors can do instead.

Good news for Canadian investors in these apparel and grocery companies, as both report higher earnings and sales.

Retirement Club for Canadians offers a sounding board and resources for people who manage retirement finance all on their...