Am I on track to retire by age 55?

The Camerons need to stop saving for 5 years to pay for daycare.

Advertisement

The Camerons need to stop saving for 5 years to pay for daycare.

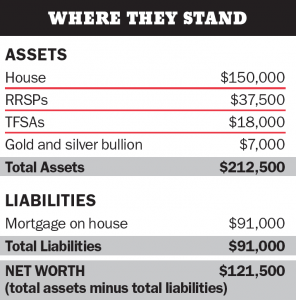

Right now, they’re on track to have their $91,000 mortgage paid off in seven years and are currently saving $15,000 annually in RRSPs and TFSAs. “We want to retire at 55 with $50,000 net a year, but as our family grows, we’re going to have to halt our savings program for five years,” says Mike, citing increased daycare costs. The couple only plans to continue paying into Lacy’s company pension plan after Baby No. 2 arrives.

To make up for lost time later, they plan to ratchet up their savings to $30,000 annually in seven years, when they’re mortgage-free and no longer reliant on daycare. They’ll then continue to invest in the same balanced and growth mutual funds that have returned 10% net annually for the past five years. “Will we still be on track to retire when I’m 55? And will our nest egg last to age 100?” asks Mike. “That’s what we’re hoping the numbers will show.”

Right now, they’re on track to have their $91,000 mortgage paid off in seven years and are currently saving $15,000 annually in RRSPs and TFSAs. “We want to retire at 55 with $50,000 net a year, but as our family grows, we’re going to have to halt our savings program for five years,” says Mike, citing increased daycare costs. The couple only plans to continue paying into Lacy’s company pension plan after Baby No. 2 arrives.

To make up for lost time later, they plan to ratchet up their savings to $30,000 annually in seven years, when they’re mortgage-free and no longer reliant on daycare. They’ll then continue to invest in the same balanced and growth mutual funds that have returned 10% net annually for the past five years. “Will we still be on track to retire when I’m 55? And will our nest egg last to age 100?” asks Mike. “That’s what we’re hoping the numbers will show.”

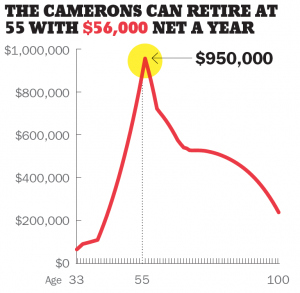

With just a 3% annual net return from their investments, Feigs calculates the couple’s portfolio will be worth $950,000 shortly after Mike turns 55, allowing them to withdraw $56,000 net annually—enough to finance a very nice lifestyle.

As it stands, though, Feigs recommends they stick with their planned retirement dates to give themselves more of a financial cushion. “Maintaining a $30,000 savings level annually will give them the flexibility to handle surprises,” he says. And because Lacy is enrolled in a company pension plan, Feigs advises that when the couple do resume their savings plan in seven years that Lacy contribute solely to her TFSA because she’s also in a low-income tax bracket. Mike, however, should use both RRSPs and TFSAs. With CPP, OAS and Lacy’s company pension payments, their portfolio will last until Mike turns 100, he says. “That’s great planning.”

Do you want MoneySense to see if you’re on track to meet your own financial goal? If so, drop us a line at [email protected]

With just a 3% annual net return from their investments, Feigs calculates the couple’s portfolio will be worth $950,000 shortly after Mike turns 55, allowing them to withdraw $56,000 net annually—enough to finance a very nice lifestyle.

As it stands, though, Feigs recommends they stick with their planned retirement dates to give themselves more of a financial cushion. “Maintaining a $30,000 savings level annually will give them the flexibility to handle surprises,” he says. And because Lacy is enrolled in a company pension plan, Feigs advises that when the couple do resume their savings plan in seven years that Lacy contribute solely to her TFSA because she’s also in a low-income tax bracket. Mike, however, should use both RRSPs and TFSAs. With CPP, OAS and Lacy’s company pension payments, their portfolio will last until Mike turns 100, he says. “That’s great planning.”

Do you want MoneySense to see if you’re on track to meet your own financial goal? If so, drop us a line at [email protected]

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Canada's top finfluencers share how they built trust, grew audiences and navigate increasing regulatory scrutiny in a rapidly maturing...

Incorporating can eliminate the need to pay CPP contributions if you are self-employed but there are trade-offs that should...

Artificial intelligence is best at overcoming the friction that stops you from taking up new pursuits, users insist.

Could moving your RRIF into segregated funds lower estate taxes? Maybe—but higher fees and other trade-offs could leave your...

Here’s how Canada’s Old Age Security pension works, who’s eligible for OAS, when you can start receiving benefits, and...

We check in on some champions of early retirement nearing their own finish line of financial independence.

What inflation, investment return, and life expectancy assumptions should Canadians use for retirement planning? Here’s what financial planners recommend.

The Saskatchewan Pension Plan gives Canadians another way to save for retirement, with low fees, locked-in contributions, and...

The FIRE movement promises early retirement, but high costs and income realities make it difficult. Here’s what the math...