Downsizing: Go small, think big

Downsizing in retirement can add a sizeable chunk of income to your nest egg, paving the way for more security and enjoyment in your golden years

Advertisement

Downsizing in retirement can add a sizeable chunk of income to your nest egg, paving the way for more security and enjoyment in your golden years

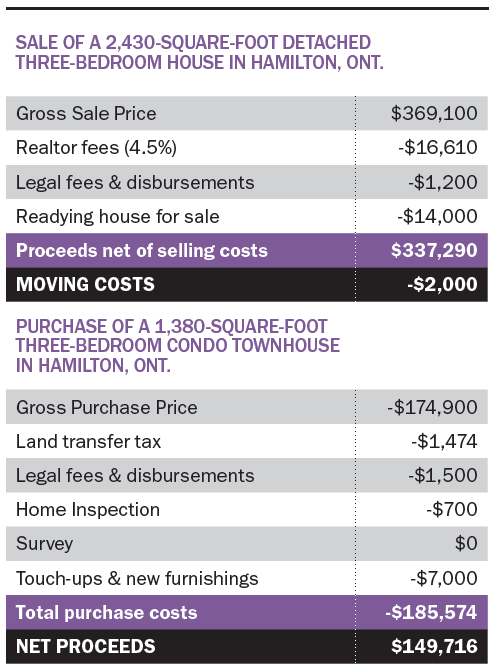

Notes: Prepared with the assistance of Melanie Reuter, Elizabeth Campbell and Don Campbell of the Real Estate Investment Network. Gross sale price, gross purchase price and land transfer tax are taken from actual recent real estate transactions in Hamilton, Ont. (In this case, the seller of the house and buyer of the townhouse are not the same.) The other figures are estimates. Realtor fees can vary from 2.5% to 6%. Money spent on readying house for sale as well as touch-ups and new furnishings will vary widely. Buyer is often required to commission a survey by the mortgage lender if the seller can’t produce one done fairly recently. In this case we’ve assumed no new survey is required. Land transfer taxes vary widely across Canada but most provinces have them. Purchase of a newly constructed home would be subject to additional costs, particularly GST. In this case, both properties are resales and not subject to GST.

Notes: Prepared with the assistance of Melanie Reuter, Elizabeth Campbell and Don Campbell of the Real Estate Investment Network. Gross sale price, gross purchase price and land transfer tax are taken from actual recent real estate transactions in Hamilton, Ont. (In this case, the seller of the house and buyer of the townhouse are not the same.) The other figures are estimates. Realtor fees can vary from 2.5% to 6%. Money spent on readying house for sale as well as touch-ups and new furnishings will vary widely. Buyer is often required to commission a survey by the mortgage lender if the seller can’t produce one done fairly recently. In this case we’ve assumed no new survey is required. Land transfer taxes vary widely across Canada but most provinces have them. Purchase of a newly constructed home would be subject to additional costs, particularly GST. In this case, both properties are resales and not subject to GST.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

We check in on some champions of early retirement nearing their own finish line of financial independence.

What inflation, investment return, and life expectancy assumptions should Canadians use for retirement planning? Here’s what financial planners recommend.

The Saskatchewan Pension Plan gives Canadians another way to save for retirement, with low fees, locked-in contributions, and...

The FIRE movement promises early retirement, but high costs and income realities make it difficult. Here’s what the math...

Experts explore whether financial independence is compatible with long-term travel, highlighting remote work, geoarbitrage, and cost-efficient “bleisure” lifestyles.

Robert has been taking RRIF withdrawals beyond the minimum required amount to gift to his kids and to reinvest...

A University of Calgary study found that over one-third of senior homeowners worry about affording basic home maintenance, suggesting...

It’s almost impossible to do, but the mindset around spending all your savings can help you make the best of the...

In the likelihood of a protracted conflict, these experts think people in or close to retirement need to review...

Rising costs, debt, and delayed planning are leaving many Canadians unprepared. Here’s what’s behind the gap and how to...