How much you really need to retire

Here's the cost of a typical middle-class retirement

Advertisement

Here's the cost of a typical middle-class retirement

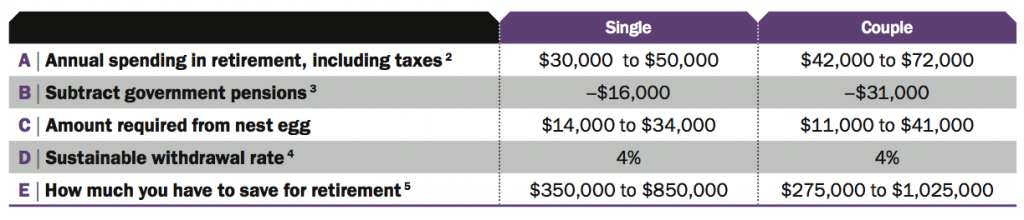

Notes: (1) All amounts are in 2014 dollars, reflecting current purchasing power. Spending projections for subsequent years are adjusted for inflation, so real purchasing power would be unchanged. (See “What’s Your Magic Number” in the Summer 2013 issue for more.) (2) Typical middle-class income before tax. Assumes a paid-for home. (3) Typical annual amount for Canada Pension Plan and Old Age Security based on retiring at age 65, assuming a fairly long career at average salaries or better. (CPP and OAS are adjusted to pay more if deferred, and CPP is adjusted to pay less if started earlier.) We’ve assumed no employer pension, but this should be included here if you have one. (4) Approximate amount that can be withdrawn from initial nest egg if retiring at age 65, with only a small risk of outliving the money, based on a rough consensus of experts. (5) Required at start of retirement at age 65 (C/D). You’ll need more if you retire earlier, or less if you retire later.

Notes: (1) All amounts are in 2014 dollars, reflecting current purchasing power. Spending projections for subsequent years are adjusted for inflation, so real purchasing power would be unchanged. (See “What’s Your Magic Number” in the Summer 2013 issue for more.) (2) Typical middle-class income before tax. Assumes a paid-for home. (3) Typical annual amount for Canada Pension Plan and Old Age Security based on retiring at age 65, assuming a fairly long career at average salaries or better. (CPP and OAS are adjusted to pay more if deferred, and CPP is adjusted to pay less if started earlier.) We’ve assumed no employer pension, but this should be included here if you have one. (4) Approximate amount that can be withdrawn from initial nest egg if retiring at age 65, with only a small risk of outliving the money, based on a rough consensus of experts. (5) Required at start of retirement at age 65 (C/D). You’ll need more if you retire earlier, or less if you retire later.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Canada's top finfluencers share how they built trust, grew audiences and navigate increasing regulatory scrutiny in a rapidly maturing...

Incorporating can eliminate the need to pay CPP contributions if you are self-employed but there are trade-offs that should...

Artificial intelligence is best at overcoming the friction that stops you from taking up new pursuits, users insist.

Could moving your RRIF into segregated funds lower estate taxes? Maybe—but higher fees and other trade-offs could leave your...

Here’s how Canada’s Old Age Security pension works, who’s eligible for OAS, when you can start receiving benefits, and...

We check in on some champions of early retirement nearing their own finish line of financial independence.

What inflation, investment return, and life expectancy assumptions should Canadians use for retirement planning? Here’s what financial planners recommend.

The Saskatchewan Pension Plan gives Canadians another way to save for retirement, with low fees, locked-in contributions, and...

The FIRE movement promises early retirement, but high costs and income realities make it difficult. Here’s what the math...