Single retirees: The power of one

Meet three sixty-something singles who breezed past those obstacles and made it work

Advertisement

Meet three sixty-something singles who breezed past those obstacles and made it work

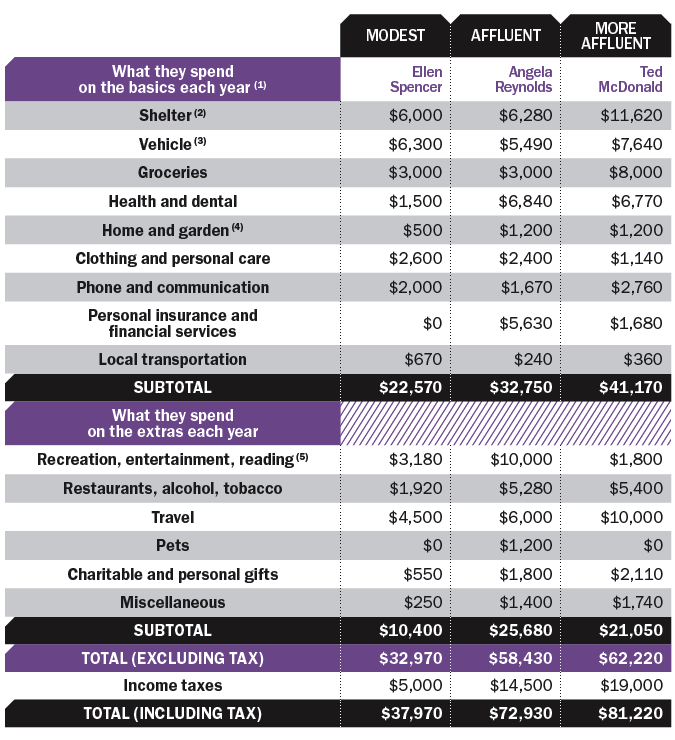

(1) Annie Kvick of Money Coaches Canada helped estimate these budgets. (2) Includes property taxes, utilities, maintenance, home insurance, rent and mortgage payments. (3) We’ve added $2,000 a year for depreciation. (4) Includes cleaning supplies, furnishings, appliances, garden supplies and services. (5) Includes computer equipment and supplies, recreation vehicles, games of chance, educational costs.

(1) Annie Kvick of Money Coaches Canada helped estimate these budgets. (2) Includes property taxes, utilities, maintenance, home insurance, rent and mortgage payments. (3) We’ve added $2,000 a year for depreciation. (4) Includes cleaning supplies, furnishings, appliances, garden supplies and services. (5) Includes computer equipment and supplies, recreation vehicles, games of chance, educational costs.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

We check in on some champions of early retirement nearing their own finish line of financial independence.

What inflation, investment return, and life expectancy assumptions should Canadians use for retirement planning? Here’s what financial planners recommend.

The Saskatchewan Pension Plan gives Canadians another way to save for retirement, with low fees, locked-in contributions, and...

The FIRE movement promises early retirement, but high costs and income realities make it difficult. Here’s what the math...

Experts explore whether financial independence is compatible with long-term travel, highlighting remote work, geoarbitrage, and cost-efficient “bleisure” lifestyles.

Robert has been taking RRIF withdrawals beyond the minimum required amount to gift to his kids and to reinvest...

A University of Calgary study found that over one-third of senior homeowners worry about affording basic home maintenance, suggesting...

It’s almost impossible to do, but the mindset around spending all your savings can help you make the best of the...

In the likelihood of a protracted conflict, these experts think people in or close to retirement need to review...

Rising costs, debt, and delayed planning are leaving many Canadians unprepared. Here’s what’s behind the gap and how to...