Mastercard, one of the biggest credit card networks, offers over 30 different credit cards in Canada, which can make shopping for a new card a little overwhelming. The good news: With so many cards, it’s easy to find one that meets your unique needs.

To help you get started, we selected the best Mastercards based on features like travel rewards, cash back, low interest, and more. We’ll highlight what we love and key factors to consider when comparing your options.

Best Mastercard credit cards in Canada

Secured Neo Mastercard

MBNA Rewards World Elite Mastercard

MBNA True Line Mastercard credit card

Before we dive into the details, get a quick look at our top Mastercard picks across the cash back, travel, low-interest, balance transfer, and secured categories.

| Category | Credit card | Annual fee | Why we love it |

|---|---|---|---|

| Best for cash back | Rogers Red World Elite Mastercard | $0 | * Steady 1.5% cash back * Earn an extra 0.5% if you have a Rogers, Fido, or Shaw service * Includes World Elite Mastercard benefits |

| Best for travel rewards | MBNA Rewards World Elite Mastercard | $120 | * Generous welcome bonus * Includes 12 types of insurance * 10% bonus points every year on your birthday |

| Best for low-interest | MBNA True Line Gold Mastercard | $39 | * Low 10.99% interest rate on purchases * Low 13.99% interest rate on balance transfers * No income requirements |

| Best for balance transfers | MBNA True Line Mastercard | $0 | * 0% promotional balance transfer rate for 12 months * Low 12.99% interest rate on purchases * No income requirements |

| Best secured card | Secured Neo Mastercard | $60 | * Guaranteed approval * Earn cash back on purchases |

Best for cash back: Rogers Red World Elite Mastercard

The Rogers Red World Elite Mastercard is also our pick for the best cash back card in Canada. It offers a high 1.5% cash back on all purchases, with a standout 3% cash back on U.S. dollar purchases. The card has no annual fee, yet it still packs impressive perks, like comprehensive insurance and access to concierge services.

Rogers Red World Elite Mastercard

Annual fee: $0

- 3% cash back on all U.S. dollar purchases

- 1.5% on all other purchases (2% for Rogers, Fido and Shaw customers)

Welcome offer: None at this time.

Card details

| Interest rates | 25.99% on purchases, 27.99% on cash advances, 27.99% on balance transfers |

| Income required | $80,000 per year |

| Credit score | 725 or higher |

Pros

- Simple rewards structure: With a minimum of 1.5% cash back on all your purchases, you don’t have to think about maximizing bonus categories or rewards tiers. The base earn rate is higher than other no-fee cards in Canada.

- FX fees offset on U.S. purchases: Earn 3% cash back on all U.S. currency purchases, both in-person and online, which is enough to offset the 2.5% foreign transaction fee (this is standard for most credit cards in Canada).

- No earnings cap: There are no category spending thresholds at which point you’ll start earning less cash back on your purchases. That’s a standout feature compared to most cards in this category.

- Flexible redemptions: Cash out your cash rewards as soon as you have $10 earned. Many cards issue cash back through statement credits once per year.

Cons

- High income requirements: You’ll need a personal income of at least $80,000 or household income of at least $150,000 to qualify.

- No boosted categories: Other cards offer higher earn rates on select boosted categories, which could help you reap more rewards depending on your spending habits.

Best for travel rewards: MBNA Rewards World Elite Mastercard

The MBNA Rewards World Elite Mastercard offers generous and flexible rewards across a variety of categories, with special perks for travelers. In addition to earning 5 MBNA Rewards points per $1 spent across five categories—restaurant, grocery, digital media, membership, and household utility purchases on the card—cardholders get an annual birthday bonus of 10% of the points earned in the last 12 months. Think of it as a nice gift to you.

MBNA Rewards World Elite Mastercard

Annual fee: $120

- 5 points per $1 on eligible restaurant, grocery, digital media, membership and household utility purchases until $50,000 is spent annually in the applicable category

- 1 point for every $1 on all other eligible purchases

Welcome offer: earn 20,000 bonus points (approximately $165 in cash back value) after you make $2,000 or more in eligible purchases within the first 90 days. (Not available for residents of Quebec.)

Card details

| Interest rates | 21.99% on eligible purchases, 22.99% on balance transfers and 22.99% on cash advances. |

| Income required | $80,000 per year |

| Credit score | 660 or higher |

| Point value | 1 MBNA Rewards point = $0.01 when redeemed for travel |

Pros

- Easy redemptions: You don’t have to worry about complex rewards charts. It’s simple to understand and use.

- High earn rates: One of the highest rates of return in Canada, this Mastercard earns a whopping 5 points per $1 spent across five spending categories.

- Benefits for travelers: You’ll get up to $2 million in travel medical insurance for the first 21 days of your trip, plus flight delay insurance, rental car discounts, and other jet-setting perks.

- Annual birthday bonus: Every year, you get a bonus equal to 10% of the points earned within the last 12 months (up to a maximum of 15,000 points).

Cons

- Travel redemption option: Points can only be redeemed for travel through the MBNA Rewards platform.

- High income requirement: As with other World Elite Mastercards, income requirements are high—$80,000 personal or $150,000 household income per year.

Best for low-interest: MBNA True Line Gold

If you need to pay down debt, the MBNA True Line Gold Mastercard has a lot to offer, like a modest $39 annual fee and one of the lowest interest rates on the market. With this card, more of your money goes toward paying off your balance rather than to fees. Plus, there is no annual income requirement, making this extremely accessible for Canadians in a tight financial spot.

MBNA True Line Gold Mastercard

Annual fee: $39

Low interest rate: 10.99%

Welcome offer: This card does not have a welcome offer at this time.

Card details

| Interest rates | 24.99% on cash advances, 13.99% on balance transfers |

| Income required | None specified |

| Credit score | 660 or higher |

Pros

- Low interest rate: The True Line Gold has the lowest interest rate of any MBNA card. If you regularly carry a balance on your card, the 10.99% interest rate may help you save on interest costs and pay off your outstanding balance faster than a card with a 19%-plus rate.

- Basic insurance: Features one year of extended warranty, 90 days of purchase protection, and rental car theft and damage coverage.

Cons

- No balance transfer offer: Unlike many low-interest cards in Canada, this one doesn’t have a promotional offer. If you need to move your debt to a low-interest card, consider the MBNA True Line Mastercard instead.

Best for balance transfers: MBNA True Line Mastercard

Feast your eyes on the best balance transfer card in Canada. If you’re looking for a way to reduce the interest on existing debt, the MBNA True Line Mastercard offers a 0% balance transfer rate for a full year. Even at the regular balance transfer interest rate of 17.99%, this card saves you on interest charges. There’s no annual fee for you and up to nine additional users, but no rewards, either.

MBNA True Line Mastercard

Annual fee: $0

Balance transfer offer: Receive a 0% interest rate for 12 months on balance transfers completed within 90 days. (Offer not available for residents of Quebec.)

Card details

| Interest rates | 12.99% on purchases, 24.99% on cash advances, 17.99% on balance transfers |

| Income required | None specified |

| Credit score | 660 or higher |

Pros

- Year-long balance transfer offer: The promotional offer lasts longer than any other balance transfer card in Canada.

- Balance transfer flexibility: You have up to 90 days to transfer your balance after opening the account.

- Pay in installments: With the MBNA monthly payment plan, split the bill on purchases over $100 into installments.

Cons

- Balance transfer fee: Even though the balance transfer interest rate is 0% for 12 months, there is a transaction fee of 3% for balance transfers ($30 for every $1,000 transferred).

Best secured card: Secured Neo Mastercard

The Secured Neo Mastercard is the best secured credit card in Canada. Plus, the Neo account dashboard is easy to use to manage your account and to redeem rewards on eligible purchases, making it a smart choice for everyday spending.

Secured Neo Mastercard

Annual fee: $96 ($7.99/month)

Rewards: 1% cashback on gas & groceries, plus up to 15% back at over 10,000 Neo partners across Canada

Welcome offer: None at this time

Card details

| Interest rates | 19.99% to 29.99% on purchases (19.99% to 24.99% for Quebec residents) and 22.99% to 31.99% on cash advances (22.99% to 25.99% for Quebec residents) |

| Income required | None |

| Credit score | None |

Pros

- Cash back rewards: Earn cash back on gas and grocery purchases with Neo retail partners. Most secured cards don’t come with such rewards.

- Guaranteed acceptance: As a secured credit card, you’re guaranteed to be approved as long as you can provide the minimum required security deposit.

- Gift card offer: $50 Indigo, SkipTheDishes or a Virtual Prepaid Mastercard $150. Offer ends July 14, 2026.

Cons

- High interest rates: Depending on your credit history profile, the purchase interest rate can be as high as 29.99% (or 24.99%, if you live in Quebec).

- Monthly fee: Unlike some secured cards that offer no fees, this card charges $4.99 per month (except in Quebec).

How we determine the best cards

To select the best Mastercards, we evaluated all the cards from this network, specifically focusing on how they ranked in our overall credit card rankings by given category. We also looked at things like annual fees, features, and perks and benefits, like insurance coverage and no foreign exchange fees. The addition of links from affiliate partners has no bearing on the results in this ranking. Read more about the MoneySense selection process and about how MoneySense makes money.

Compare all popular Mastercards

Compare all Mastercard credit cards available in Canada using our interactive tool below. You can filter cards based on rewards value, annual fees, income requirements and more.

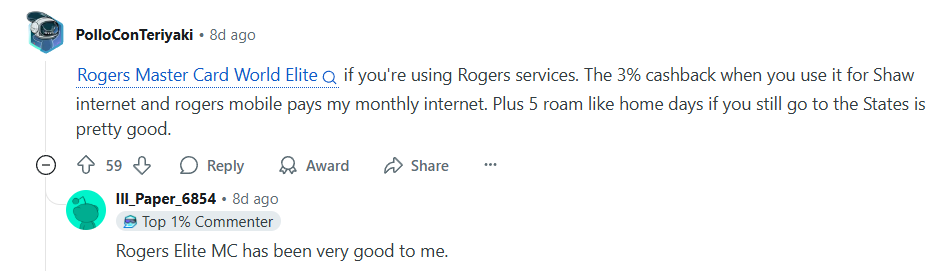

Reddit reviews: What cardholders say

We know what’s best on paper, but we like to see what actual cardholders have to say about the best cards in real life—so we headed to Reddit. Here are real users’ recommendations:

Other users across separate threads seem to agree:

Users also pointed out that they loved being able to use the Rogers Mastercard at Costco (especially since Costco doesn’t accept Amex or Visa).

Types of Mastercards

Not all Mastercards are created equal. There are basically three tiers of Mastercards with different requirements, rewards, and annual fees. You can choose from:

- Standard Mastercards: These are the basic or entry-level Mastercards with the lowest eligibility requirements and annual fees that range from $0 to $89. They usually have limited benefits and low rates of return on rewards, but they’re useful cards if you’re starting out or building credit.

- World Mastercards: These mid-tier cards offer slightly better benefits and rewards, so they usually require a personal income of $50,000 or a household income of $80,000. The cards cost between $39 and $115, but the increased rewards and better insurance can make it worth the annual fee.

- World Elite Mastercards: These premium Mastercards cost between $99 and $199 a year and require high incomes of $80,000 personal or $150,000 household. You’ll enjoy the most perks and World Elite Mastercard benefits that include concierge service, Priceless Cities, Travel Pass airport lounge access, and much more.

Mastercard vs. Visa

As two of the largest credit card networks in Canada, Mastercard and Visa have a lot in common. They’re mainly issued by the same banks and credit unions and both networks are widely accepted around the world.

Both Mastercard and Visa can be added to digital wallets and they feature the same enhanced security along with zero liability protection.

Where they differ comes down to the individual card’s terms and benefits. For instance, a Visa Infinite has similar rewards and benefits to a mid-tier World Mastercard, and Visa Infinite Privilege has comparable perks to a World Elite Mastercard. However, the individual cards issued by banks or credit unions may have slightly different rewards or insurance coverage.

Mastercard has a few things going for it: it’s the only network accepted at Costco, it offers more low- or no-fee credit cards, and some would argue its cash back cards have better reward rates. If you’re more focused on everyday savings than elite perks, you might find better matches with Mastercard than with Visa.

Find the perfect card with CardFinder

In under 60 seconds, get matched with a personalized list of the best credit cards based on your spending personality and approval likelihood. No SIN required.

How to choose the right Mastercard for you

If you’re set on Mastercard as your network of choice, you could start by shopping around for a card or seeing which Mastercards your bank or credit union offers. Don’t forget that some retailers offer co-branded Mastercards, too.

Narrow your options by deciding the type of card and what’s important to you. For instance, decide if you’re looking for a:

- Student card

- Low-fee card

- Cash-back card

- Travel card

- Shopping card

- Balance transfer card

Once you’ve found a card that you’re eligible for with an annual fee that fits your budget (or, better yet, no fee), apply through the card issuer’s website or click on one of the MoneySense links to get started.

FAQs

Mastercard offers three levels of credit cards in Canada: (1) basic cards with no income requirements, (2) mid-tier World Mastercards, which require $50,000 personal or $80,000 household income, and (3) World Elite Mastercards, which require $80,000 personal or $150,000 household income.

Unlike the World Mastercard, the CIBC Costco Mastercard doesn’t charge an annual fee and only requires $15,000 in household annual income. While the CIBC Costco Mastercard is more accessible and offers better earn rates, the World Mastercard includes a wider range of perks.

Visa and Mastercard are incredibly similar networks that offer comparable credit cards. Your best bet is to search for a credit card that matches your spending habits and has what you’re looking for, rather than focusing on a single network.

To get a World Elite Mastercard, you’ll need a great credit score and a minimum $80,000 personal or $150,000 household income per year.